i got your point.

after posting the thread....i came to know the right way.

Anyway thanks for the guideline.

I will close the thread

i got your point.

after posting the thread....i came to know the right way.

Anyway thanks for the guideline.

I will close the thread

@mahesh112 with due respect to you, this is not the VP way of initiating a new thread, please look at the recent threads of Vidhi Dye stuff or Deccan cements, Cafe Coffee Day etc. where the members have opened a new thread in a comprehensive way. I suggest you also do similar kind of work before you seek other's opinion. Lot of senior members are there who would be willing to help if you have done your part correctly. Thanks.

Hi,

I'm new to market.

I bought man infra@39.40.

Any view please

I recently was doing some scuttlebutt and speaking to some industry insiders in the plywood sector. The view is that real estate is in very bad shape in West & North of India and moderate / stagnant demand in East & South. It is definitely impacting the offtake of products. Housing for all and smart cities have not yet picked up demand on the ground.

No, I won't date here as I cannot two time my existing partner CCL Products

Anyway, seriously, at 1 billion USD valuation and a PAT of 80 crore as per your above post, it is straight away getting 70 PE? While strictly not comparable, CCL Products is available at 15-17 times FY17E EPS of 14-15 and 24 times FY16E 10-11 EPS.

However, India is a predominantly a Tea drinking country as so far we did not have this coffee culture, westernisation thing not yet penetrated broadly. I myself in my 20s felt aspirational drinking coffee in a Barista or Coffee day so with Indian demographics in support the coffee culture is going to explode and market opportunity could be huge.

After reading the above post, I personally would stay away from this IPO as the capital allocation strategy is not encouraging and so is the company's stake in unrelated fields. Also, the business is real estate intensive. For coffee culture, you need to be present in HIGH cost locations with appealing interiors etc.

I too am from Hyderabad. Would like to get in touch , to share and discuss ideas. Let me know if you have some time. My mail id is skotte@gmail.com

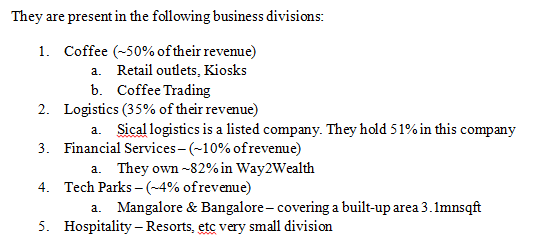

Café Coffee Day well known for its CCD outlets operates outlets since 1996. They are present in about 209 cities in India. They have a market share of about 46% and are the largest in terms of total number of chains. Café Coffee Day (CCD) has come out with an IPO for an amount of Rs 1150 crores with fresh issue of 35060976 shares valuing the company at ~ Rs 6756 crores approximately. Post issue Promoter Holding will stand at ~52.55%

Apart from this CCD owns about 16.6% stake in Mindtree. Their consolidated debt stands at 2762 crores.

Logistics Business:

Sical Logistics Limited is a listed company and most of the financial information for this company is available in public forum. This company is available at a market cap of ~900 crores.

Techparks Business(Similar to NESCO):

They have 2 tech parks in Bangalore and Mangalore with a built-up area of 3.1mn square feet. This division does a top-line of around ~95-100 crores on a yearly basis. This is around 4% of their top-line.

Coffee Division:

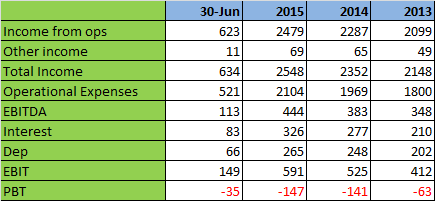

Coffee division #s:

The above table has the break-up of Coffee segmental revenues reported for this company. Of this 80% of the revenues are from retail outlets and these outlets operate at an EBITDA margin of ~20%. The other 20% of the revenues come from trading business which has an EBITDA margin of about ~2%.

So their retail coffee business is doing approximately 1000 crores/FY. Their retail coffee business is operating at an EBITDA of ~20% going by their EBITDA.

Consolidated Revenue from all divisions:

The company is planning to raise around Rs 1150 crores and the objective of this issue is to accomplish the following major heads:

1. Repay loan amount of about ~630 crores.

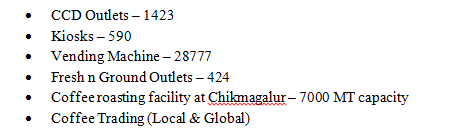

2. Set-up 215 new CCD outlets at a cost of 37lakhs/outlet – ~79 crores

3. Set-up 8000 new vending machines at a cost of 1.2lakhs/machine - ~97 crores

4. Set-up 105 new kiosks at a cost of 7.4lakhs/kiosk - ~7.77crores

5. Refurbishment of existing outlets – 60 crores

6. Setting up an additional 7000 MT coffee roasting plant capacity – 41 crores

Conservatively assigning Holding price discount for their investments in Sical Logistics & Mindtree:

1. Sical’s market cap is 900 crores. They have a 50% stake. So at 1/6th (holding price discount), Sical investment can be valued at 80-90 crores.

2. Mindtree’s market cap is 10,500 crores. They have a 16.6% stake. So at 1/6th (holding price discount), Mindtree investment can be valued at 338 crores.

3. They have cash/cash equivalents of about 197 crores.

4. Techpark & Financial services contributes to 4% & 10% respectively to their top-line. (150crores valuation on the optimistic side?)

At the issue price of 328/share the company is asking for a valuation of 6756 crores. Factoring in the above valuation for their other businesses, you roughly get the coffee business(retail + trading) at a market cap of 5815 crores. Add debt of about 2100 crores. The company’s enterprise value stands at 7900 crores.

Coffee retail business doing a top-line of about Rs 1000 crores, operating at 20% EBITDA has a market share of about 46%. Even if they manage to do 8-10% PAT margin (on the optimistic side), you get PAT of 80 crores(very optimistic #). Jubilant is valued at 100 PE. Most of the front end retail companies are valued at north of 70-80PE.

From here valuation of CCD is an individual’s call.

The big negatives here for me are:

1. Poor capital allocation – Their cash cow is their retail coffee business, they are pumping in money in to low RoE Techpark, Financial & Logistics business. They borrow to do this. Most of their borrowings stand at around 13-15%. So they borrow at this rate and invest in these low RoE business

2. No specific Niche – As an investor I am interested only in their 40% retail business. This IPO is looking to raise cash for their holding company

3. Their culture of funding growth(??) through Debt.

Thanks,

Ravi S

Thanks for your detailed notes. Totally answers my question.

@manoj I did not care (pun intended) to buy into CARE because,

There is this conflict of interest with rating agencies all the time. It is behaviourally difficult to downgrade a company's bond etc. when that company is paying you and when that company is a source of your revenues. I read few books related to 2009 financial crisis and was fascinated by how these rating agencies work. Fascinated here in a sarcastic way.

It's difficult to rate a company because it is difficult to know practically ALL the details of a company and one fine day some issue sees the light of the day and the rating company which rated it so far will be thrashed.

It is for this reason I did not invest in rating agencies and the reason showed up itself in Amtek for example. This is not the first one and the last one, you will see many such instances in corporate India as our economy leaps in the coming years.

In way, these are like aviation companies. Once in a while a plane crashes which could be due to manufacturer fault or the airlines but more than manufacturer's stock the airlines stock is hammered. See what happened to Malaysian airlines. Bad example, eh?

HOWEVER, I think the BOND market itself is so HUGE that opportunities to grow in this field are AMPLE, just that a black swan event could pull you down by 2-3 years in terms of stock price. So, why buy when there are other opportunities.

I won't invest 2-3% in a stock, it should be around 10% at least and I'm not comfortable investing 10% YET.

Stock hitting 52 week low due to 'so and so' reason which is beyond companies hands should never be a REASON to buy it.

This is my thinking and I could be entirely wrong.

if company is doing exceedingly well then what is the logic behind decrease in promoter stake and for which reason larsen & toubro exit from startgeic stake holding pl give some light on it