Yes, Abhijit. You should put appropriate and meaningful disclosure to comply with forum guidelines.

Posts tagged Value Pickr

Vidhi Dyestuff Management Meet (06-10-2015)

Hi Dhwanil

Glad it was useful!

Another interesting observation from the AR is that despite the major break down due to fire of a critical equipment (which affected 30% of the production), they were able to grow at a steady pace.

I feel discontinuing the trading biz is a very wise move and must result in superior ROCEs.

Also as I'm new here, Is it compulsory to put Discl. at the end?

Vidhi Dyestuff Management Meet (06-10-2015)

Hi Abhijit,

Thanks for the management meet updates. It is very useful. Especially, the answer to Sensient buying out VDSL was very interesting!!

If the management's vision plays out, it looks like a very interesting bet. However, there is one big "If". We, as an investor, must assess the odds of management's vision turning into reality. I did some number crunching and few inferences base on the same

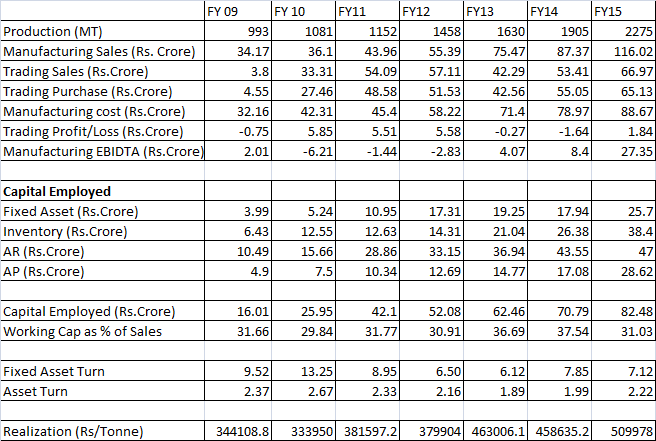

- Company is currently making a loss in its trading activities thus reduction in trading revenue as % of sales will improve margins. However, it is important to note that in the past, company made EBIDTA losses for manufactured product also.

- For the manufactured product, company's margin have increased consistently over last 3 years from 7% to 10% and this year it has increased to 23%. Thus, it is possible to improve margins from here on if the manufacturing/trading ratio changes in future.

- Company's working capital cycle has remained stable despite growing at 25% CAGR which indicates that company is managing it's capital well.

- Realizations have improved at 7-8% CAGR over last 6 years from 3.44 lakhs/ton to 5.09 lakhs/ton . However, a part of realization improvement has come from rupee depreciation. Thus, in constant currency terms, the realization may have only increased marginally.

- Company has grown consistently over last 6 years(25% CAGR) with managing its balance sheet well thus there is a fair chance that in future, company will be able to grow without impacting the balance sheet quality.

- Sansient, makes around 20-22% EBIDTA margins in spite of operating in high cost countries, thus 20% EBIDTA margin seems achievable for Vidhi.

- It is an asset light business, and fixed asset turns are very high (due to high value product) thus any improvement in margin combined with asset light business, can fetch very decent ROCE. In fact, ROCE can increase beyond 25%, if company is able to achieve 20% EBIDTA margins.

After looking at competitors like ROHA and Sensient, I too come to same conclusion that it is a industry dominated by few large players and business is growing for companies like Roha and Vidhi as companies like Sensient are forced to look at natural colors due to their existing clients demanding the same. At the same time, I also got an impression that there exist a slow but sure shift from synthetic color to natural colors (even though, as management rightly pointed out, there is no evidence of synthetic color being harmful). Thus, it will be prudent to start developing products for natural colors market.

On whole, it remains interesting idea worth tracking to me

Disclosure: Hold small position @ Average price of 48.

Hitesh portfolio (06-10-2015)

Hi Hitesh,

With pharma doing so well in recent years, do you foresee a bubble forming? or are we already in a bubble? All pharma cos valuations are stretched. How far can it go?

REPCO home finance – another Gruh in the making? (06-10-2015)

@bbarhate : I can answer why Repco is not taking up leverage question.

In fact Repco is increasing leverage but slowly. It doesn't happen that Repco disburses 2-3,000 cr of loans in a year just because it can. Management has said in past that they are comfortable with growing at 25% in current environment. If economy picks up they'll like to grow at 35% but would not compromise on quality of loans or cost of operations.

All said and done, Repco will not leverage as much as Gruh. Credit rating agencies look at leverage when they give you a rating. A discussion with one of my friend working in a rating agency revealed that many times when NBFC approaches rating agency, the analysts ask them to get to a certain level of leverage by raising equity if the higher rating is to be given.

Arrow Coated Products ( ACP) BSE CODE – 516064 – Anybody tracking (06-10-2015)

Article in today's Economic times on Arrow coated products

Avanti Feeds (06-10-2015)

Thanks Mukesh, That I am aware of of, But haven't seen any research report yet, not even on research byte

Dynemic Products (06-10-2015)

Please check the complete thread. U will find the reasons. And also, the explanations for them.

Vidhi Dyestuff Management Meet (06-10-2015)

Vidhi Dyestuff Management Meet Notes

Vidhi Dyestuffs Manufacturing Ltd. (VDML) is the third largest manufacturer of synthetic food colours globally with a capacity of 4200 MTPA. It is among the very few USFDA approved manufacturers of food grade colours in India. Over the last 20 years, the company has established strong relationships with global majors like Mars, Pedigree and Sanofi among others. The company has been able to grow its revenues substantially by 21% CAGR over the last five years, while the industry has witnessed a growth of 4-5%. Going forward, the company’s investments in capacity addition and reduction in its low margin trading business would help it achieve its targeted margins of 20% plus over the next 4-5 years. Following is Transcript of our Meet with the Management.

What are the entry barriers in our business? How strong is the customer stickiness for a seemingly commodity product?

Ans: Switching suppliers is a big hassle for clients as colour component is very small (colour comprises of ~0.5% of the cost of the final product). We have spent 20 years carefully establishing relationship with clients and distributors across 80 countries.Is our business a commodity business? Are there any risks to our business?

Ans: ‘You may keep a halt on buying Ferrari during recession, but what about strawberry cream biscuits and flavoured chocolates?’ More than 95% of our manufacturing revenues are from exports thus exposing us to currency risks but apart from that none.Who are our direct competitors?

Ans: Due to a small overall market size of synthetic food colours, there are only four major players worldwide. Sensient Technologies (20,000 MTPA), Roha Dyechem (9000 MTPA), we are the third largest manufacturers with 4,200 MTPA, Emreld USA (2,200 MTPA). No competition from china as market size is too low for them (40k MTPA, growing at 5%).Where is Sensient focusing given it is losing its market share in synthetic food colours? Sensient's website suggests increased focus on natural food colours, how strong is the shift in trend? What is the natural vs synthetic dilemma all about?

Ans: First it is a myth that Synthetic colours are harmful. Natural flavours have less variety in terms of colour and only premium products are using it. There is no apparent trend shift towards natural colours and it is just a propaganda. We are selling our product 25% cheaper than the world leader Sensient and thus gradually taking their market share.What is our expansion plan and how are we planning to fund the upcoming expansion?

Ans: We are aiming at capacity of around 8,400 MTPA by 2020, capturing around 20% of market share. We are just waiting for environmental clearance to start with the incremental capacity addition. Mix of internal accruals and debt will be used for the same, around 60:40 ratio.Why the decision to stop trading and cause a de growth in the coming year as the new capacity will take time to ramp up?

Ans: Trading is a high capital and a low return business and thus we will discontinue it from the next month onwards. Trading is ruining our balance sheet and we rather use that WC for manufacturing. We are running at almost full capacity and want to focus on high margin manufacturing business.Is there any pricing differential in our product and Roha Dyechem? Will get any benefit in terms of lower raw material price with recent fall in crude oil price?

Ans: There is none and we don’t touch their customers and nor they touch ours. Yes some of the benefit we will pass to the customer but some we will keep for us.Can Sensient buy us out in coming years? Will we be open for it?

Ans: Yes, if they have an ‘offer which we can’t refuse’ !

!Are we looking to enter in the Naturals arena? Do we have any presence in that segment? Apart from that do we have any other opportunity to expand?

Ans: Yes, we are developing one colour at a time in natural segment. So far we have developed couple of natural colours and we are the sole manufacturers for one of the colour. Apart from Natural we have the Pigment market of 15k Crore to explore in future. So market opportunity is there.Where do we see ourselves in 2020? What is the vision?

Ans: Over Rs. 500 Cr. in top line with 20% OPMs, Capacity of around 8,400 MTPA.What dividend policy have we decided?

Ans: As discussed in the last AGM, we will continue to distribute 20% of the Earnings.

For any queries email me: chokshiabhijit@gmail.com

Abhijit Chokshi

+91 9920245796

Any view on gold? (06-10-2015)

hello everyone,good afternoon to all. anybody have any idea about today's moves of gold in market? if anyone have some view on it please suggest me. I am really very confused about gold moves.