Hi sorry, I am not following Lawsikho very closely… Can you please tell me why the increase in Skill Arbitrage contribution to the revenue such a good thing? Is it a higher margin vertical or has bigger TAM? What is it?

Thanks!

Hi sorry, I am not following Lawsikho very closely… Can you please tell me why the increase in Skill Arbitrage contribution to the revenue such a good thing? Is it a higher margin vertical or has bigger TAM? What is it?

Thanks!

Hi @kdjolly,

Where are you getting your information from for sakar?

I’m unable to find any company presentations or concall transcripts after Oct 2022.

Thanks in advance!

Hi @kdjolly,

Where are you getting your information from for sakar?

I’m unable to find any company presentations or concall transcripts after Oct 2022.

Thanks in advance!

There are reports of Expleo solutions being sold by the current promoters, scouting for buyers. ,it seems… After a subdued quarter, Revenues & Profits set to improve over the next few quarters.

There are reports of Expleo solutions being sold by the current promoters, scouting for buyers. ,it seems… After a subdued quarter, Revenues & Profits set to improve over the next few quarters.

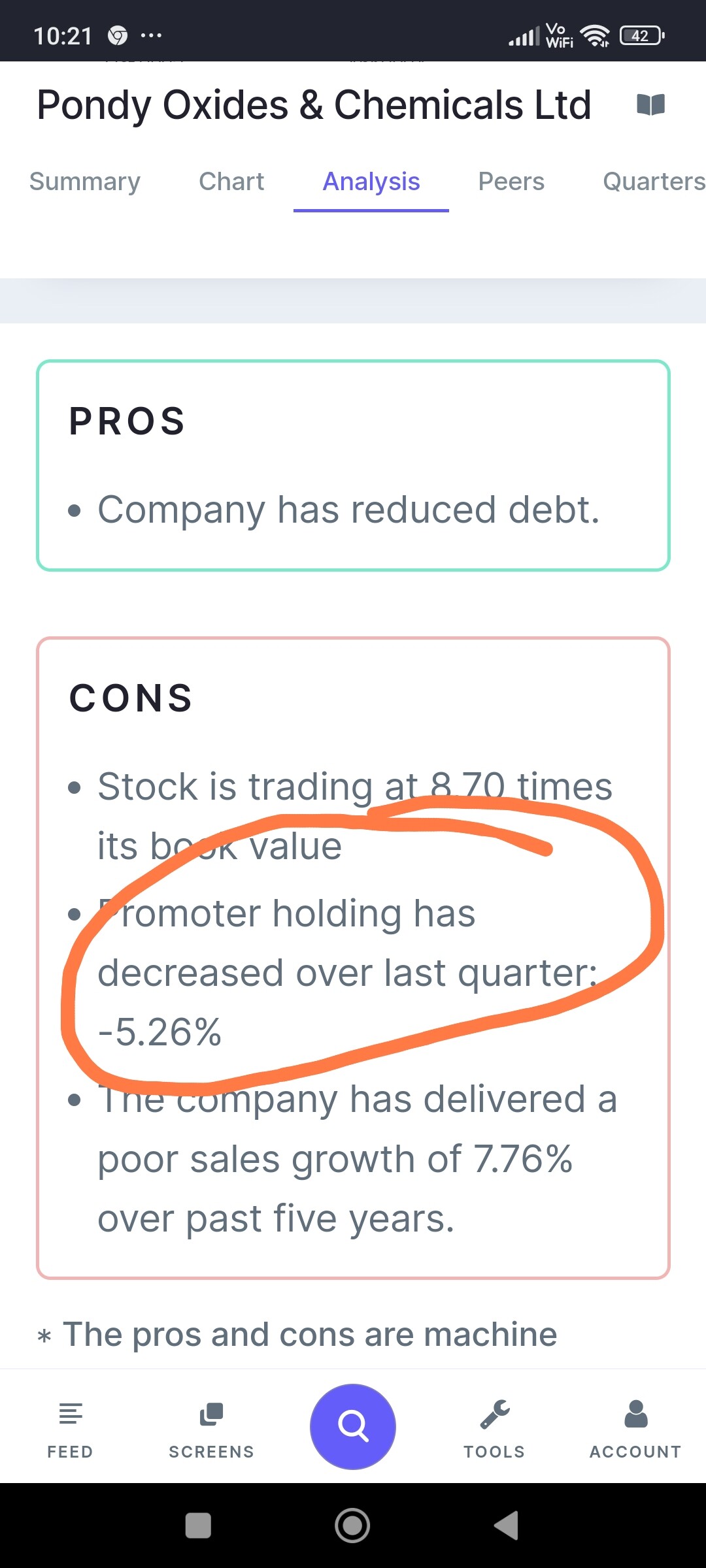

ICICI DIRECT Mobile app

ICICI DIRECT Mobile app

I have also thought in similar lines as you. Defence cashflow comes late after a war but defence ancillaries cashflow is even further late. Just there are some conditions. Need cheap defence ancillaries. So select those below p/b of 7. Example MIDHANI. I have invested in it but would now prefer reducing exposure and diversifying. Now there is a tailwind in aerospace sector also. So defence ancillaries + aerospace. By that logic we get AXICADES, CYIENT, Apollo Microsystems and Dynamatic technologies. I also have fresh position in Automative axles but it does very little defence and no aerospace. All stocks below 7 p/b.

I had done a similar analysis for paint ancillaries as there was a new paint war going to start. Also Asian paints management has gotten arrogant. I identified 3 companies. Atul chemicals, Mangalam organic and 20 micron. If which since 20 micron is small corporation I avoided it and I brought lot of Atul and less Mangalam. A very very big mistake. Both 20 micron and Mangalam are 100% up but Atul is only 30% up. I don’t recommend these paint ancillaries stocks right now to anyone. But this strategy of selling spades to gold diggers or weapons during a war always works. I lack experience or I would have done it will electric car ancillaries. Maybe even now money can be made in electric battery chemicals. I have a lot of experience for next bull run. Only God knows when will that come. Next year is definitely a bear market so please invest with care. Also Sir checked you’re profile you have invested all corpus in Equity!! Sir please for Lord Shiva’s sake liquidate corpus and buy gold, silver ETF with 25% of it. Especially do this after next year April end. ![]()

Warning : I am not Sebi registered Investment advisor. No buy sell recommendation. It’s only out of care for senior people.

I have also thought in similar lines as you. Defence cashflow comes late after a war but defence ancillaries cashflow is even further late. Just there are some conditions. Need cheap defence ancillaries. So select those below p/b of 7. Example MIDHANI. I have invested in it but would now prefer reducing exposure and diversifying. Now there is a tailwind in aerospace sector also. So defence ancillaries + aerospace. By that logic we get AXICADES, CYIENT, Apollo Microsystems and Dynamatic technologies. I also have fresh position in Automative axles but it does very little defence and no aerospace. All stocks below 7 p/b.

I had done a similar analysis for paint ancillaries as there was a new paint war going to start. Also Asian paints management has gotten arrogant. I identified 3 companies. Atul chemicals, Mangalam organic and 20 micron. If which since 20 micron is small corporation I avoided it and I brought lot of Atul and less Mangalam. A very very big mistake. Both 20 micron and Mangalam are 100% up but Atul is only 30% up. I don’t recommend these paint ancillaries stocks right now to anyone. But this strategy of selling spades to gold diggers or weapons during a war always works. I lack experience or I would have done it will electric car ancillaries. Maybe even now money can be made in electric battery chemicals. I have a lot of experience for next bull run. Only God knows when will that come. Next year is definitely a bear market so please invest with care. Also Sir checked you’re profile you have invested all corpus in Equity!! Sir please for Lord Shiva’s sake liquidate corpus and buy gold, silver ETF with 25% of it. Especially do this after next year April end. ![]()

Warning : I am not Sebi registered Investment advisor. No buy sell recommendation. It’s only out of care for senior people.