Firstly, of course, forget the age. Who thought age equals wisdom, and even experience.

You have raised very important points let me look at them again.

Of course, I have not recommended these stocks. The thread I created with a view to discover more hidden treasures as ancillaries or ancillaries of ancillaries.

In both the cases I have concentrated more on what the companies do.

In fact, we should be happy to look up their competitors. There may be a few.

PS: Really like your analogy of few prospectors made money panning for gold while the suppliers who sold them shovels and picks profited nicely.

Posts tagged Value Pickr

Investment in the ancillaries, or ancillaries of ancillaries-vendors of famous companies (07-09-2024)

Deep Industries (DIL) (07-09-2024)

15 year order. Don’t extrapolate this with market cap.

Investment in the ancillaries, or ancillaries of ancillaries-vendors of famous companies (07-09-2024)

Sir apologies. You’re my senior but I have a rule. Never ever invest in defence companies with P/b >7. I would ask you to relook Avantel investment by this parameter. Regarding Bartronics I cannot understand what has changed. It is listed from 2015 except price movement and minor profit I find no change in company. Please enlighten me more. But I agree with you’re methodology. When people dig for gold there is money in selling them spades.

Godawari Power – Any Trackers? (07-09-2024)

China Slowdown Concerns and Iron Ore Prices:

The ongoing slowdown in China’s economy and the drop in global iron ore prices are valid concerns. However, it’s crucial to note that GPIL is less exposed to these fluctuations than many other players in the market. One of the primary reasons is its fully backward-integrated operations. GPIL sources 100% of its iron ore from captive mines, which means it’s insulated from the volatile pricing that typically affects companies reliant on external sources.

Moreover, while the global slowdown is contributing to the correction in commodity prices, domestic demand for iron ore and steel in India remains strong. India’s steel production continues to grow at around 7% CAGR, and the government’s ongoing infrastructure projects are expected to provide steady demand for iron ore. In fact, GPIL’s premium pellets, which fetch Rs1000-1500 more per tonne due to their high Fe content, cater specifically to this domestic demand, especially from DRI plants in Chhattisgarh. This makes GPIL better positioned to weather the current global headwinds.

Strong Margins and Operational Efficiency:

GPIL has significantly expanded its pellet capacity, which will drive its revenue and profitability over the next few years. By FY27E, pellets will contribute 57% of GPIL’s revenues, up from 39% in FY24. The expanded capacity ensures that GPIL will continue to benefit from economies of scale, further lowering production costs while increasing margins.

Additionally, GPIL’s access to captive iron ore means it doesn’t have to pay premiums on royalty, which enhances its profitability compared to other steel producers who rely on externally sourced ore. The company’s integrated solar power plant also helps to reduce energy costs, providing additional margin stability.

Strategic Expansion and Long-Term Growth:

GPIL’s growth story is not just about the present—it’s about its strategic long-term investments. The company is planning to double its pellet capacity and set up a 2 million tonne steel plant, entirely funded through internal accruals, without incurring any debt. This steel plant will not only double GPIL’s EBITDA but also make the company even more resilient to commodity price fluctuations by fully backward-integrating its iron ore and energy requirements with green power sources like solar.

This positions GPIL as a net cash company, able to fund its growth internally, a rare feat in the capital-intensive steel industry. Even in the face of fluctuating global commodity prices, GPIL’s balance sheet will remain strong, and the company will be able to capture the next phase of growth without taking on additional financial risk.

E2E Networks Ltd – Listed small Cloud computing player (07-09-2024)

read this on Twitter. thoughts?

SG Mart- Can it successfully create a marketplace? (07-09-2024)

What I think is the name of APL Apollo will stand out here, as we have known this group and the management is also looking clean and as they are maintaining such healthy EV/EBITDA growth then I guess the PE will shrink down. Here we should look for Forward PE according to their guidance like FY25 is projected at ₹7,000-8,000 Cr, with expectations to ramp up to ₹13,000-14,000 Cr in FY26 and ₹18,000-20,000 Cr in FY27. This guidance will shrink down their PE and one concern about is their OPM which I think a good management knows how to handle.

My Top 5 Investment Basics Books, & why? (07-09-2024)

The first book I give to people on investment is either Morgan Housel’s Psychology of Money or Richer, Wiser. Happier, then may be Fundamental Analysis for Dummies.

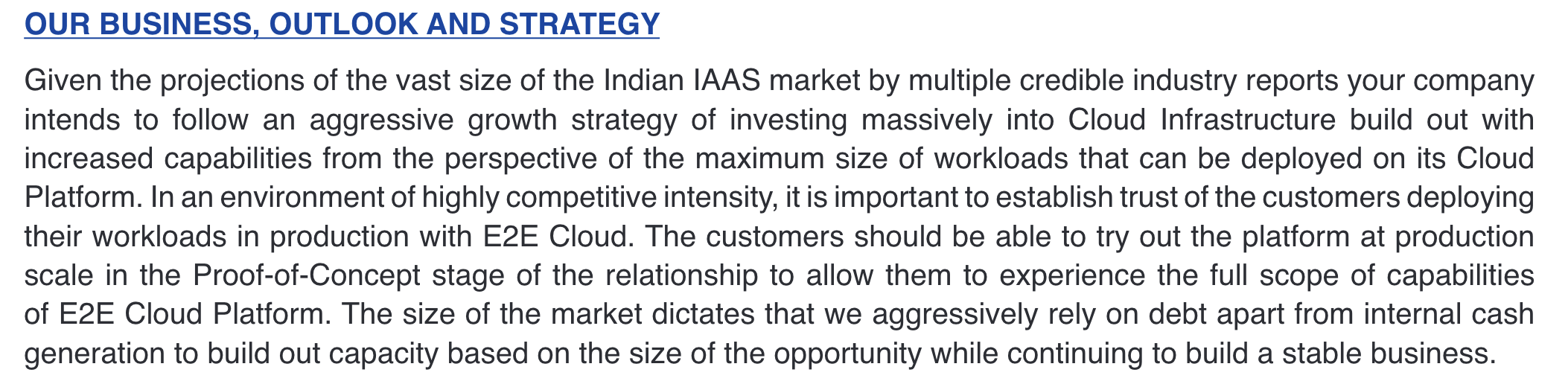

E2E Networks Ltd – Listed small Cloud computing player (07-09-2024)

Going through the AR, found this in the MD&A.

I think a few things are going to happen based on my observation:

- A stock split is highly likely in the short term due to the sheer absolute price of the stock

- More debt could by raised once the cash flow from the 420 cr. Capex starts flowing in and company is assured of its debt payoff

- Interest payment and D/E will rise leading to more debate/discussion on its justification for high valuation

- Further equity dilution with fund raising either via Preferential Allotment/FPO/Rights Issue is on the cards over next 12 months

- Sales will continue to hold with industry CAGR upto 2029 is expected to be ~25%.

Possible timeline this round of Capex:

September 11th – Vote for funding

October Mid – Funds received/ Order Placed

November End – New Hardware Received (based on 4-6 weeks wait time for new hardware as per concal)

December End – Installation complete, brought new H/W online

Jan-March – Revenue generation from new capex

Based on this we can expect no more actual funding happening (discussion/targets may be talked about/set) this year as the cash flow will happen Q4.

Krishca Ltd : A SME offering steel strapping Solution (07-09-2024)

Few takeaways from Annual Report(2023-24) of Krishca.

Strategic Facility Expansion

& Future Growth Initiatives :-

New Hardening and Tempering

Line in Tamil Nadu

The company has launched a new

hardening and tempering line in Tamil

Nadu, marking a significant expansion in

production capacity. This development

allows the company to enter new

markets with its Ultra High Tensile

Strapping, a product in high demand

across various industrial sectors.

Entry into the Welding

Consumables Market

The company is set to enter the welding

consumables market by establishing

a new subsidiary and constructing a

MIG welding wire production plant in

Chennai. This facility will serve both

domestic and international markets,

reinforcing Krishca’s commitment to

diversifying its product portfolio and

expanding its global footprint.

Strategic Investment in

the Middle East

As part of its global expansion strategy,

Company is making significant

investments in the Middle East. The

company is establishing new sales

offices, warehouses, and a state-of-theart manufacturing plant in the region,

providing a strategic gateway to the

lucrative US market.

Focus on India’s Steel

Packaging Market

Recognizing the potential of India’s steel

packaging market, which is valued at

₹ 2000-2500 crore annually, Krishca is

intensifying its focus on this sector. The

company aims to secure a significant

share by forming strategic partnerships

with major packaging contractors who

manage the packaging needs of steel

mills.