From q1 con call

An old interview with MD

New order from ONGC. Order value 1,402 Cr (single order is > 50% of current market cap of the company !!)

In addition, company has mastery in acquiring asset at vary cheap valuation through insolvency resolution process under the Insolvency and Bankruptcy Code and converting them in efficient asset generating good revenue and profit with minimum investment on it.

Disc – Invested earlier. 8000 @ 201 INR

Yes I am from surat. I am interested.

One Query has come. so some further explanation :

These ranks are based on Sharpe returns. Sharpe returns are price returns divided by volatility.

I use average Sharpe returns of (3months+6months+9months+12 months) . I use a paid readymade screening website momoscreener This is for information, not for promoting it. here are many such ranking websites available which gives you readymade ranking of your selected universe as well as your customised screening criteria.

@Balki Sir can you please explain what is going in Expleo solutions stock,why revenue not growing sir and what is your current view on this stock and what about this stock future prospects sir?

Dilip Buildon: Q1 FY25 concall highlights

Order book:

Debt:

Asset transfer:

DBL 2.0:

Guidance:

Hi all, After long time…update on strategy and portfolio…After reading Wesley book and many other material , I finalised my startegy to follow Rank-based momentum.

I selected 2 seperate uinverses :-

so my portfolio currently looks like this :

Microcap stocks :

SmallCap Stcoks

11) Glenmark Pharma

12) Godfrey Phillips

13) Inox Wind

14) PCBL

15) Eris Lifesciences

16) Granules

17) Suven Pharma

18) Natco Pharma

19) Himadri Specialty

20) Deepak Fertlizers

Currently 23% of my overall portfolio is in this strategy. If I get comfortable and more convinced, I will be shifting slowly my remaining 77% ( which is currently in mutual funds) to this startegy. If I take this decision in future, then I will be selecting the universe of Nifty 200 and Midcap 150 as well.

Returns : from 1st August 2024 till 1st Sept 2024 = 6.25%

27% PAT margin translates to 36% PBT margin assuming a 25% effective tax rate

Q4FY24 which had higher proportion of Indri sales in the overall distillery segment had a 31% EBIT margin. Even if you allocate all of interest & other cost to distillery segment, the PBT % would have come up as 29% for the distillery segment.

Now this 29% is composed of low margin country liquor and ethanol sales and high-margin Indri sales. It’s anyone’s guess as to what margin Indri would have given that country liquor would be mid-teens at best.

This is because in FY22, EBIT for distillery segment was 20% and at that point of time, Indri + Kamet + blended malt whiskeys had a combined sales of 18k cases in the full year. For reference, Q1FY25, Indri alone has done 25k cases.

Fair to say that the standalone Indri numbers would be substantially higher given the distillery segment is a mix of low margin country liquor, ethanol sales etc vs high margin Indri

Another way to look at this is 70%+ gross margins. Take another 25% for SG&A and all other kinds of opex. That gives you 45% EBITDA. Interest & Depreciation – take another 10% worst case. 35% PBT and you have 27% PAT after assuming 25% tax rate.

In my practical view though, gross margins would also inch up as special editions of Indri gain traction. They sell at nearly 2x price point, which means gross margins may be substantially higher for them.

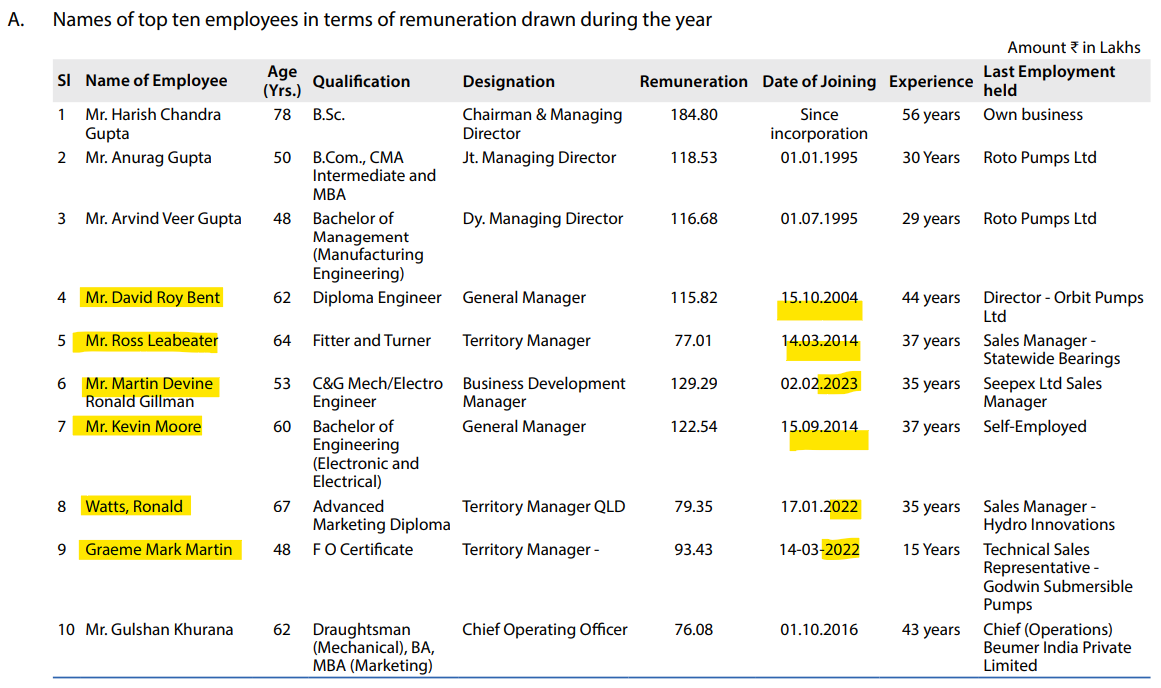

FY24 AR Observations:

49th Annual General Meeting of the Company scheduled to be held on Saturday, September 28, 2024 at 04:30 P.M. through Video Conferencing (VC) or Other Audio-Visual Means (OAVM)

Re-appointment of Mr. Harish Chandra Gupta as Chairman & Managing Director of the Company: Aged about 78 years is the co-founder of the Company | Remuneration upto ₹ 32,00,000/- per month | Past Remuneration: Remuneration upto ₹ 17,82,000/- per month

Re-appointment of Mr. Anurag Gupta as Jt. Managing Director of the Company: Aged about 49 years is one of the promoter of the Company | Remuneration upto ₹ 21,00,000/- per month | Past Remuneration: Remuneration upto ₹ 11,43,000/- per month

Re-appointment of Mr. Arvind Veer Gupta as Dy. Managing Director of the Company: Aged about 48 years is one of the promoter of the Company | Remuneration upto ₹ 12,00,000/- per month | Past Remuneration: Remuneration upto ₹ 11,25,000/- per month

Sub-division of Equity Shares of the Company and alteration of Capital Clause of Memorandum of Association (MOA) of the Company:

Nature of Industry: The Company is engaged in the business of manufacturing and sales of progressive cavity pumps, twin screw pumps, spare parts of pump and retrofit spares and provision of maintenance & repair services and commissioning & installation services in Domestic and Overseas Market.

The Company had embarked on a new project of Downhole Pumps and Mud Motors. A state-of-the-art Manufacturing facility has been setup and commercial production of Downhole Pumps has been commenced. As a part of this project existing Unit at Phase II Extension Noida to have an in-house facility for hard chrome plating and other critical activities for the said Downhole pumps and mud motors and existing products as well. Development of Mud Motors is in advance stage and is expected to commence.

Company’s new wholly owned subsidiary Company established to carry on business of solar pumping systems has also commenced commercial production.

Increased focus on existing operations coupled with commencement of new operations, would improve performance of the Company.

Expected increase in productivity and profits in measurable terms: Subject to the unforeseen circumstances, in 2023-24, the Company expects to increase its productivity which would amount to more than 25% in sales turnover and profits. Thereafter, an annual growth of 20% in sales and corresponding increase in annual profits is expected.

Our Mission: To achieve 100 million USD revenue by 2028. | FY23 Mission: Our Mission is to be among the first five global Positive Displacement Pump manufacturer by the year 2030.

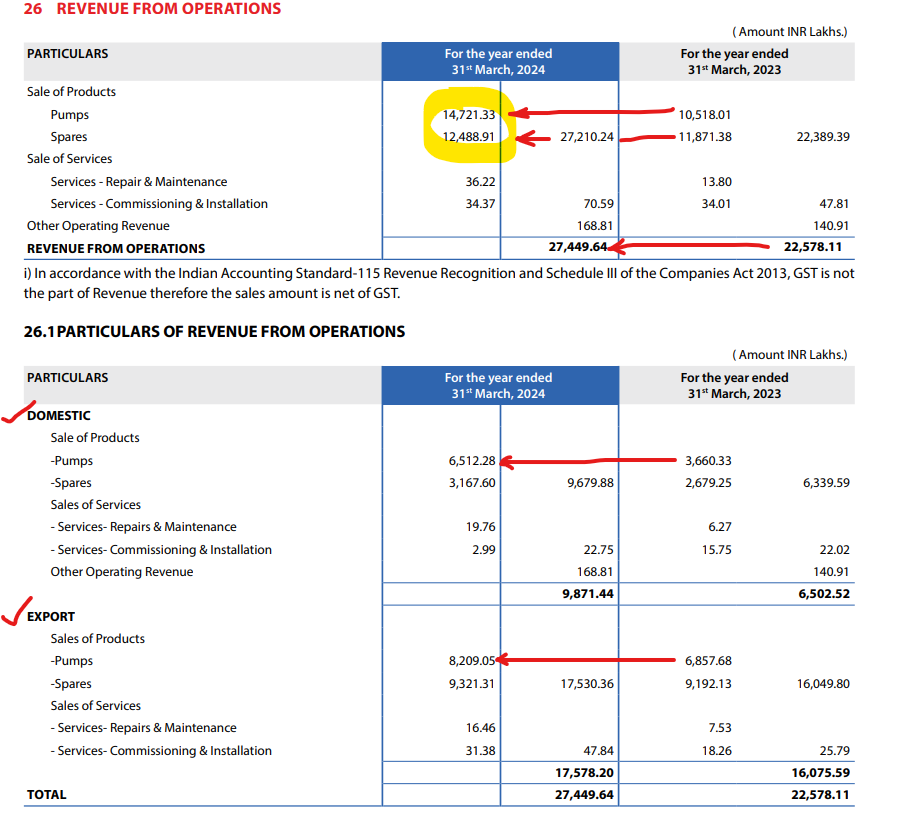

Domestic sales were ₹ 9,870.36 lakhs as compared to ₹ 6,502.52 lakhs having an increase of 51.79%. Export sales were ₹ 13,110.13 lakhs as compared to ₹ 12,563.08 lakhs, having an increase of 4.35% over last year. Export sales includes ₹ 7,209.13 lakhs, sales from Marketing Outlets in United Kingdom and Australia. Revenue from exports constitutes 54.99% of the total revenue from operations.

Medium term growth would be led by new businesses of downhole pumps and solar pumping systems, which would substantially contribute to business growth. Downhole pumps are used for artificial lift and mud motors are used in directional drilling.

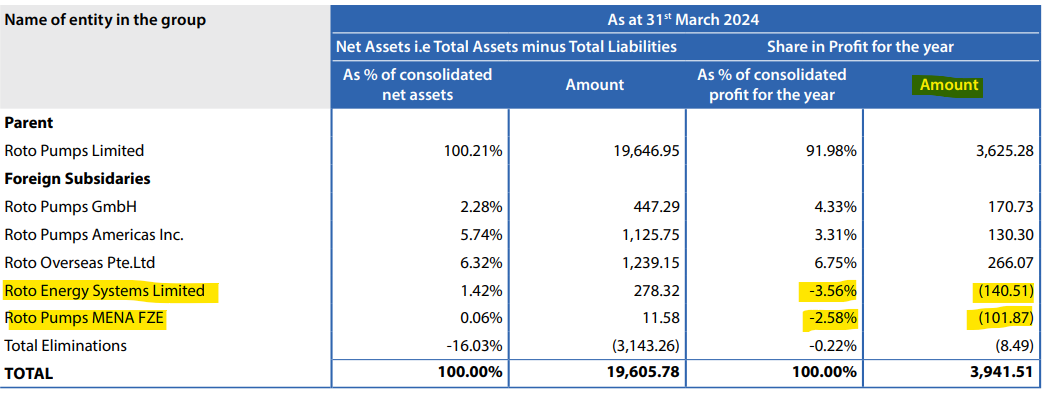

Roto Energy Systems Ltd. – a wholly owned subsidiary was incorporated to carry on business of solar pumping systems. The Subsidiary is taking steps towards commencement of its business operations. During the year under review, the subsidiary has achieved sales turnover of ₹ 3.00 lakhs and incurred a loss of ₹ 140.66 lakhs.

Roto Pumps Mena FZE – a wholly owned subsidiary (WOS) in UAE was setup to cater the MENA region. a company engaged in the business of sales and marketing of Company’s products in the MENA region. During the year, the subsidiary has achieved a sales turnover of AED 743,546 and incurred a loss of AED 449,017.

Horses for the courses:

Revenue Breakup:

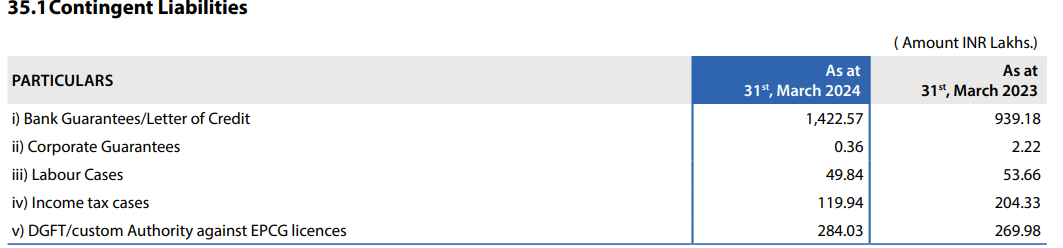

Contingent Liab:

Market Risk: The Company operates internationally and a major portion of the business is transacted in several currencies. Consequently the company is exposed to foreign exchange risk through its sales and services in the US and elsewhere, and purchases from the overseas suppliers in various foreign currencies. The Company holds derivative financial instruments such as foreign exchange forward contract to mitigate the risk of changes in exchange rates on foreign currency exposure.

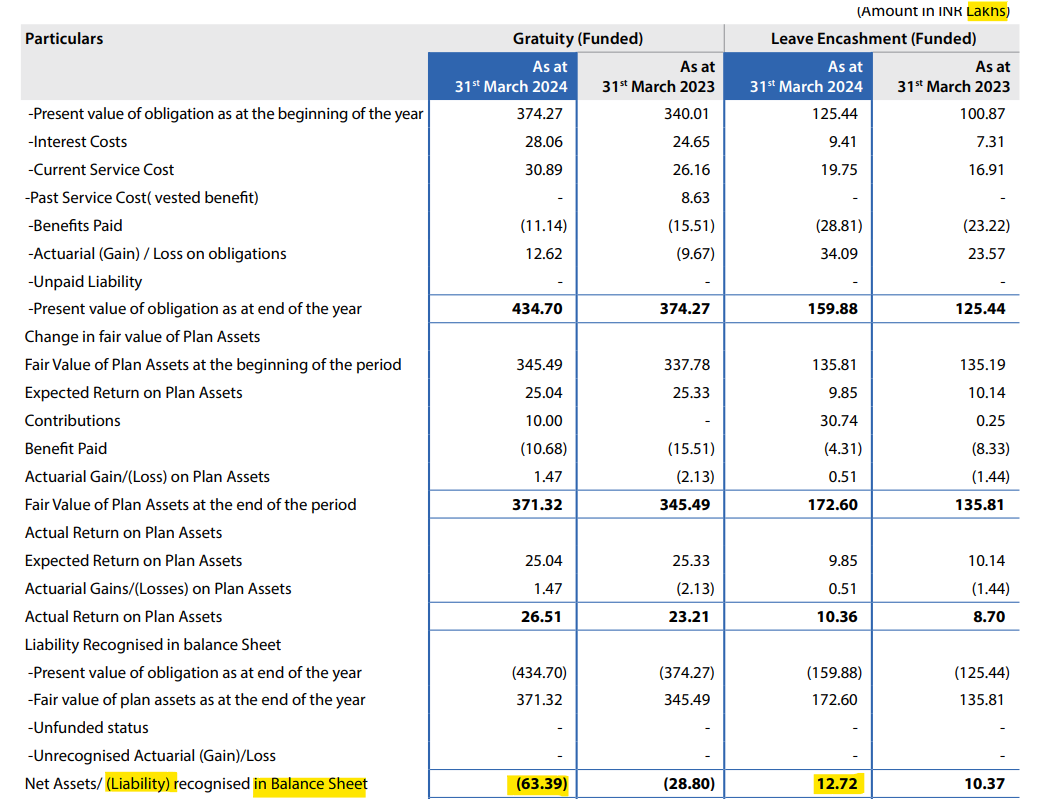

Defined Benefit Plan Liabilities:

Goose (WOS) that are yet to lay eggs (loss making as of now):

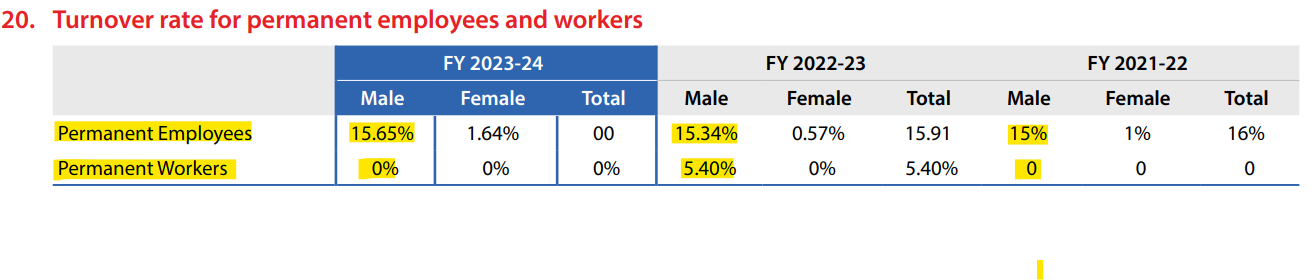

Attrition:

Disc: Not Invested