Hi Kalpesh – Thanks for sharing the bond portfolio with the group. One more information if you can share, what is the interest payment frequancy you opt generally for the above bonds and is there any risk which one should keep in mind while opting the given frequancy.

Posts tagged Value Pickr

Avantel (04-09-2024)

Even I was surprised and was about to post the same. One of the 3 companies shortlisted is a big achievement and yet no announcement formally on the exchange.

The Cycle of Financial Manias (04-09-2024)

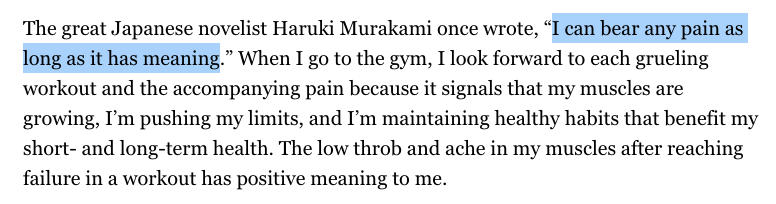

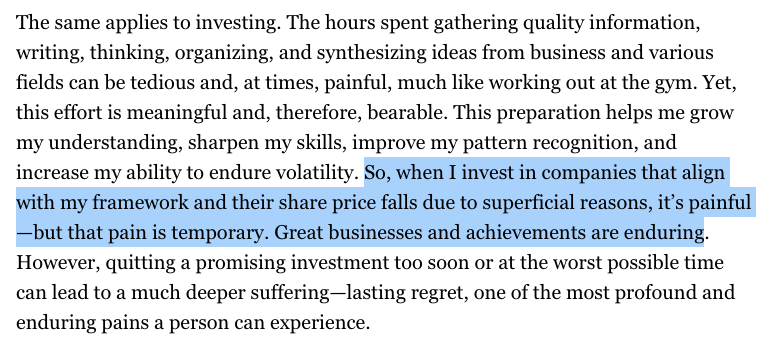

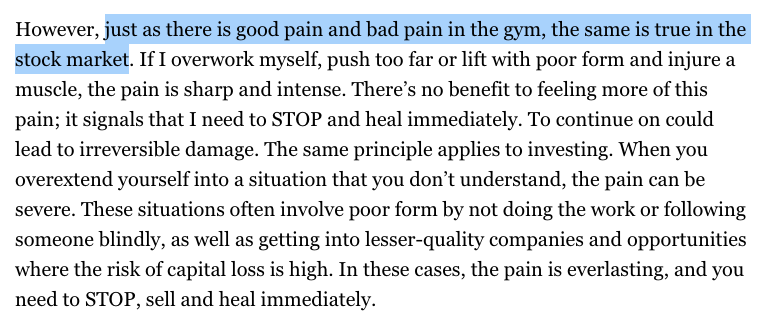

Throughout history, financial markets have been repeatedly gripped by manias—periods of intense and irrational enthusiasm where asset prices soar to unsustainable heights. During these times, everyone seems to believe that the market is a goldmine, with endless opportunities for anyone to grab a piece of the wealth. Stories of overnight fortunes and the lure of easy money spread like wildfire, captivating the imaginations of investors and non-investors alike.

1. The Illusion of Easy Money

- Greed Takes Over : As tales of easy profits circulate, greed becomes the dominant emotion, overshadowing caution and rational thinking. People begin to believe that wealth can be easily acquired, and this belief fuels a collective frenzy.

- Herd Mentality : As more people rush into the market, the herd mentality takes hold, driving prices to sky-high levels. The fear of missing out (FOMO) on potential gains leads individuals to follow the crowd, often without conducting their own due diligence.

- Rational Judgment is Abandoned : The disciplined approach to investing is abandoned in favour of speculation. Investors overlook fundamentals and risk, convinced that prices will continue to rise indefinitely.

2. The Market Flood

- New Issues and Dubious Companies : Established companies, sensing the public’s eagerness to invest, flood the market with new issues, many of which are designed to capitalize on the mania rather than create real value. At the same time, dubious and unproven companies (multi-myriad, mid-small-micro cap companies join the party) enter the fray, luring gullible investors with promises of high returns.

- Continued Frenzy : The market frenzy intensifies as more and more money pours in. The history of past market collapses and the evaporation of millions of investors’ hard-earned money is completely and thoroughly discounted. People convince themselves that this time is different, that the market will continue to rise without end.

3. Ignoring Historical Lessons

- The Cycle of Boom and Bust : Despite the clear lessons from history, people continue to fall into the same traps, repeating the cycle of boom and bust that has brought ruin to countless investors. The essence of a mania lies in the collective belief that “this time is different.”

- Disregard for Fundamentals : Investors, driven by the fear of missing out and the allure of rapidly rising prices, convince themselves that the usual rules of economics no longer apply. Fundamental values are disregarded, and the crowd rushes headlong into the market, each person emboldened by the actions of others.

- Self-Reinforcing Speculation : As prices escalate, the sense of invincibility grows stronger, drowning out the voices of caution. The mania feeds on itself, creating a self-reinforcing cycle of speculation that can only end in collapse.

4. Human Nature and Cyclical Amnesia

- The Temptation of Easy Money : Why do people continue to engage in such behavior, knowing full well the disastrous outcomes of past manias? The answer lies in the flaws of human nature. The prospect of easy money is often too tempting to resist, even for seasoned investors.

- Fading Memories of Past Losses : Over time, the pain of past losses fades, leading to a kind of cyclical amnesia. New generations of investors, who may not have experienced previous crashes, are particularly vulnerable to the siren call of a booming market.

- False Confidence : Even those who have lived through past bubbles may find themselves drawn back in, believing they can outsmart the market or time their exit perfectly. This recurring pattern highlights a profound truth about human behavior in markets: people often fail to learn from history.

5. The Tragic Irony

- Short-Term Gains vs. Long-Term Wisdom : As Warren Buffett famously said, “What we learn from history is that people don’t learn from history.” Despite the clear and repeated evidence that manias end in disaster, the same psychological forces continue to drive people into speculative frenzies. The lessons of the past are ignored, as the desire for short-term gains overrides long-term wisdom.

- Rationality vs. Emotion : In the end, manias are a reflection of the inherent tension between rationality and emotion in investing. The thrill of being part of a rapidly rising market, combined with the pressure to conform to the crowd, leads people to make decisions that, in hindsight, seem foolish.

- The Cycle Repeats : Yet, as time passes and the scars of previous crashes heal, the cycle begins anew. This is the tragic irony of financial manias: they are as predictable as they are destructive, yet they continue to occur, driven by the unchanging nature of human psychology.

Conclusion

Financial manias are a recurring phenomenon, deeply rooted in human psychology and the allure of quick riches. While the specifics may vary from one mania to the next, the underlying pattern remains the same: a spark of opportunity ignites a frenzy of speculation, which eventually spirals out of control and collapses. The challenge for investors is to recognize the signs of a mania, resist the urge to follow the crowd, and remain grounded in the fundamentals that ultimately govern market behavior. The lessons of history are clear, but only those who heed them can hope to avoid the pitfalls of the next financial mania.

Glenmark Life Sciences (04-09-2024)

Glenmark Life Sciences –

Q1 FY 25 results and concall highlights –

Revenues – 588 vs 578 cr, up 2 pc

Gross margins @ 51 vs 57 pc

EBITDA – 165 vs 195 cr, down 15 pc ( margins @ 28 vs 33 pc )

PAT – 111 vs 135 cr, down 18 pc

Cash on books @ 426 cr

Breakdown of revenues ( by customers ) –

Non GPL business – 392 cr ( 67 pc of sales )

GPL business – 196 cr ( 33 pc of sales )

Breakdown of revenues ( by business segments ) –

Generic APIs – 535 cr ( 93 pc of sales )

CDMO – 42 cr ( 7 pc of sales ) – signed a multiyear agreement with an innovator for supply of API. Expect commercialisation wef Q4

Breakdown of revenues ( by target markets ) –

Regulated markets – 84 pc

Emerging markets – 16 pc

Breakdown of revenues ( by therapeutic segments ) –

Cardio – 41 pc

CNS – 16 pc

Anti-Diabetic – 4 pc

Pain management – 6 pc

Others – 33 pc

Contribution from chronic therapies @ 67 pc

Have added 05 APIs to the development grid – 03 are high potency – Onco APIs and 02 are synthetic small molecules

Manufacturing facilities –

Ankleshwar Gujarat – 742 KL ( additional 208 KL capacity will come on stream wef Q2 FY 25 @ Ankleshwar )

Dahej Gujarat – 381 KL ( additional 18 KL capacity will come on stream wef Q2 FY 25 @ Dahej )

Mohol Maharashtra – 49 KL

Kurkumbh Maharashtra – 25 KL

Greenfield expansion @ Solapur – phase -1 of construction has started to set up a 200 KL facility. Phase 2 @ Solapur shall add another 400 KL of capacity. In addition, 400 KL of backward integration capacity is also planned at the same site

Future growth drivers – Onco High Potency APIs, CDMO ramp up, expansion into complex APIs and Iron compounds, pursuing 2nd source opportunities for top generic players, geographical expansion

Future drivers of operational efficiencies – Debottlenecking, backward integration, adoption of flow chemistry in manufacturing

Company’s business with GPL did suffer in Q4. In Q1, there has been a smart recovery and this business is up 18 pc QoQ

Q1 was company’s first Qtr after a long time without the PLI benefits. Hence the contraction in Gross Margins. Slightly unfavourable product mix also contributed to GM compression

Company expects their CDMO business to pick up significantly in Q2

Company had received a closure notice from Gujarat Pollution control board ( in Mid July ) for its Ankleshwar site – citing pollution outside their plant / site. The issue was finally resolved on 14 Aug. Company should be able to catch up for the production loss as 1.5 months are still available in this Qtr

Company doesn’t expect their GMs to go below 51 pc in future

According to the management, upcoming demand environment is much, much better. The brownfield expansion that’s coming on stream should take care of this additional demand over next 1-2 yrs. After that, the Greenfield capacity at Solapur shall kick in

The Bio-Secure act in US is a definitive tailwind for the company’s CMO business – they did acknowledge the the same in the concall

Capex requirements for FY 25 @ around 350 cr. Capex outlay for FY 26 shall also be significant. Hence the dividends payouts, going fwd should be smaller vs past. Also – don’t intend to take on any debt for the planned capex for next 2-3 yrs

Company’s CDMO business currently has 3 commercial projects. Should add another 2 products by end of FY 25. These 2 projects should add 100 cr / yr to the topline. That should take the total CDMO business to around 250 cr / yr. Aim to take it to 500-600 cr / yr in next 4-5 yrs

Post the change of promoters and Nirma group taking over, company has become more aggressive wrt Capex

Disc: initiated a tracking position, biased, not SEBI registered, not a buy/sell recommendation

Ranvir’s Portfolio (04-09-2024)

Glenmark Life Sciences –

Q1 FY 25 results and concall highlights –

Revenues – 588 vs 578 cr, up 2 pc

Gross margins @ 51 vs 57 pc

EBITDA – 165 vs 195 cr, down 15 pc ( margins @ 28 vs 33 pc )

PAT – 111 vs 135 cr, down 18 pc

Cash on books @ 426 cr

Breakdown of revenues ( by customers ) –

Non GPL business – 392 cr ( 67 pc of sales )

GPL business – 196 cr ( 33 pc of sales )

Breakdown of revenues ( by business segments ) –

Generic APIs – 535 cr ( 93 pc of sales )

CDMO – 42 cr ( 7 pc of sales ) – signed a multiyear agreement with an innovator for supply of API. Expect commercialisation wef Q4

Breakdown of revenues ( by target markets ) –

Regulated markets – 84 pc

Emerging markets – 16 pc

Breakdown of revenues ( by therapeutic segments ) –

Cardio – 41 pc

CNS – 16 pc

Anti-Diabetic – 4 pc

Pain management – 6 pc

Others – 33 pc

Contribution from chronic therapies @ 67 pc

Have added 05 APIs to the development grid – 03 are high potency – Onco APIs and 02 are synthetic small molecules

Manufacturing facilities –

Ankleshwar Gujarat – 742 KL ( additional 208 KL capacity will come on stream wef Q2 FY 25 @ Ankleshwar )

Dahej Gujarat – 381 KL ( additional 18 KL capacity will come on stream wef Q2 FY 25 @ Dahej )

Mohol Maharashtra – 49 KL

Kurkumbh Maharashtra – 25 KL

Greenfield expansion @ Solapur – phase -1 of construction has started to set up a 200 KL facility. Phase 2 @ Solapur shall add another 400 KL of capacity. In addition, 400 KL of backward integration capacity is also planned at the same site

Future growth drivers – Onco High Potency APIs, CDMO ramp up, expansion into complex APIs and Iron compounds, pursuing 2nd source opportunities for top generic players, geographical expansion

Future drivers of operational efficiencies – Debottlenecking, backward integration, adoption of flow chemistry in manufacturing

Company’s business with GPL did suffer in Q4. In Q1, there has been a smart recovery and this business is up 18 pc QoQ

Q1 was company’s first Qtr after a long time without the PLI benefits. Hence the contraction in Gross Margins. Slightly unfavourable product mix also contributed to GM compression

Company expects their CDMO business to pick up significantly in Q2

Company had received a closure notice from Gujarat Pollution control board ( in Mid July ) for its Ankleshwar site – citing pollution outside their plant / site. The issue was finally resolved on 14 Aug. Company should be able to catch up for the production loss as 1.5 months are still available in this Qtr

Company doesn’t expect their GMs to go below 51 pc in future

According to the management, upcoming demand environment is much, much better. The brownfield expansion that’s coming on stream should take care of this additional demand over next 1-2 yrs. After that, the Greenfield capacity at Solapur shall kick in

The Bio-Secure act in US is a definitive tailwind for the company’s CMO business – they did acknowledge the the same in the concall

Capex requirements for FY 25 @ around 350 cr. Capex outlay for FY 26 shall also be significant. Hence the dividends payouts, going fwd should be smaller vs past. Also – don’t intend to take on any debt for the planned capex for next 2-3 yrs

Company’s CDMO business currently has 3 commercial projects. Should add another 2 products by end of FY 25. These 2 projects should add 100 cr / yr to the topline. That should take the total CDMO business to around 250 cr / yr. Aim to take it to 500-600 cr / yr in next 4-5 yrs

Post the change of promoters and Nirma group taking over, company has become more aggressive wrt Capex

Disc: initiated a tracking position, biased, not SEBI registered, not a buy/sell recommendation

Oriental Carbon and Chemicals Ltd (04-09-2024)

Had mailed them and received this reply.

Screener Specter – Companion for screener.in (04-09-2024)

New Features in v1.3 and Future Plans!

I’m excited to share an update about the latest version of Screener Specter, a Chrome extension I developed to enhance our experience on Screener.in. After receiving some fantastic feedback, I’ve made several updates to make the extension even more useful for our investing journey!

What’s New in the Latest Update:

- Improved Insights and Forensic Data: The extension now includes a “Shareholder Frenzy” factor that monitors changes in the number of shareholders over time to gauge investor interest, market sentiment, and potential volatility.

- Better Performance: Under-the-hood optimizations ensure smoother performance and faster loading times.

Plus, I’ve added a Google Feedback Form right in the extension! Your input can truly shape its future, so please take a moment to share your thoughts and ideas.

Looking Ahead: Future Updates and AI-Powered Features

In future updates, I’m planning to add several new features to make Screener Specter even more customizable and insightful:

- Customizable Forensic Settings: One of the exciting additions will be an optional settings menu that lets you personalize various forensic insights. For example, instead of using fixed constants for sales growth checks (like 15%, 10%, or 5%), you’ll be able to set your own parameters. This will also apply to compounded growth checks for consistency, allowing you to tailor the extension to suit your investment style perfectly!

- AI-Driven Insights and Projections: I’m working on integrating AI to provide more advanced data analysis, trend prediction, and tailored stock recommendations.

- New Indicators and Visualizations: Based on user feedback, I plan to add more indicators and advanced filtering options, enhancing the depth of analysis available.

Atma Nirbhar Bharat – Stock opportunities (04-09-2024)

Indian Navy set to receive 12-Warships over the next 12 months against old orders.

These are against old orders which are under different stages of construction at Mazgaon Dock & Garden reach ship builders, which means that these shipping companies would book under revenues during next 12.months.

https://idrw.org/indian-navy-set-to-receive-12-warships-over-the-next-12-months/