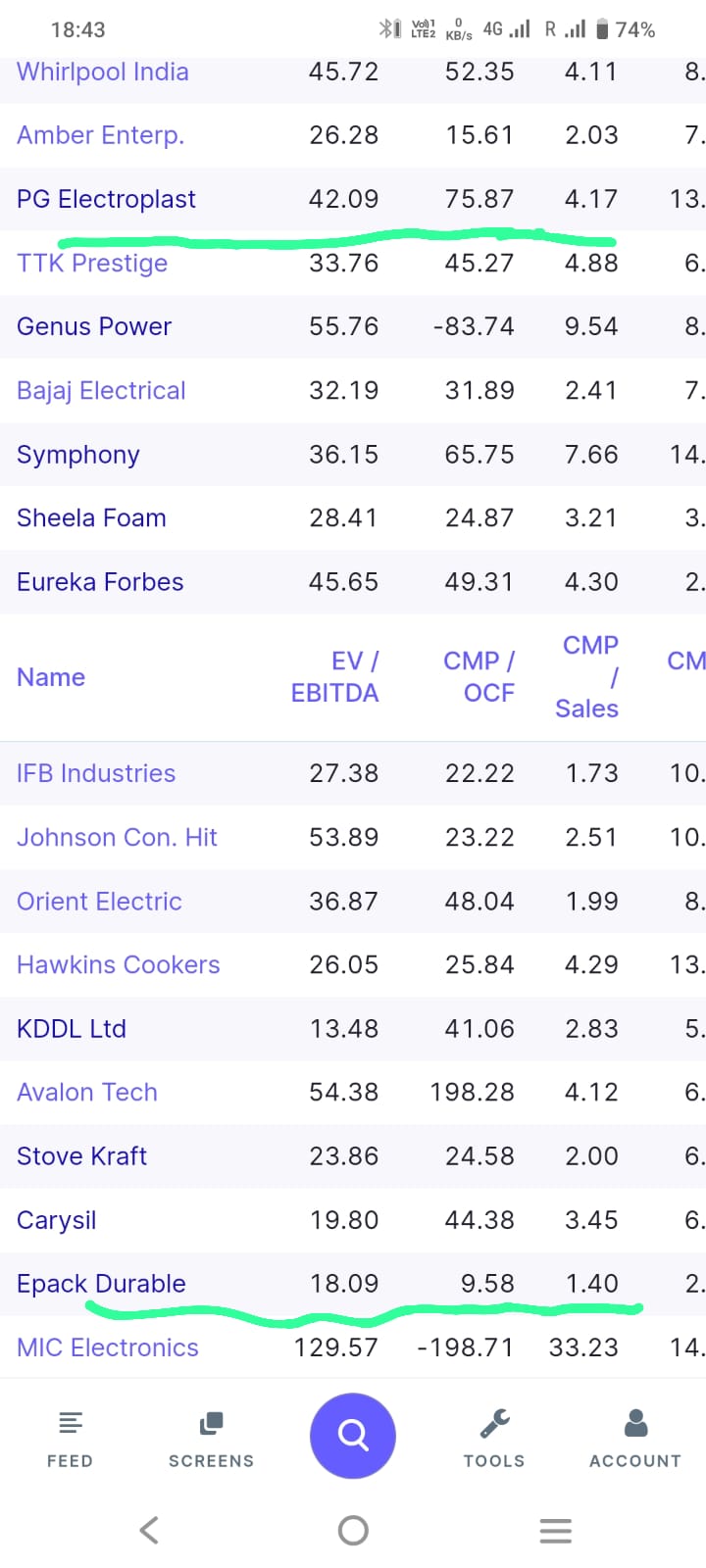

simple screener like

Sales growth >15 AND

Profit growth > 15 AND

Return on equity > 20 AND

Market Capitalization > 1000 AND

Debt to equity < .50

but this will give mostly stable companies for others we need to change parameters and track many companies, sometimes we get companies from competitors and analysis of some other businesses.