My trust on myself has started coming back! Though my average is quite high but I am glad that I averaged

Posts tagged Value Pickr

Tree house education and accessories ltd. – Potential candidate for improvement in RoE (08-12-2015)

Avanti Feeds (08-12-2015)

Board Meeting on Dec 18, 2015 08 Dec 2015 17:52

Avanti Feeds Ltd has informed BSE that a meeting of the Board of Directors of the Company will be held on December 18, 2015, inter alia, to consider the following:

Approval of Business Transfer Agreement (BTA), in connection with transfer of Shrimp Processing Business to Avanti Frozen Foods Private Limited (a wholly owned subsidiary of Avanti Feeds Limited), to be effective from November 01, 2015, at a slump sale value of Rs. 128.00 crores.

(the Members of the Company approved the transfer of Shrimp Business of the Company to Avanti Frozen Foods Private Limited by way of slump sale which shall not be lower than the net book value of assets and liabilities by a Special Resolution through Postal Ballot, the results of which were declared on October 26, 2015).To consider subscription of 60,00,000 equity shares of Rs. 10/- each a premium of Rs. 131/- per equity share, aggregating to Rs. 84.60 crores in connection with the Rights Issue made by Avanti Frozen Foods Private Limited.

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=afa2953e-2efe-440d-a215-efeaa25960f7

Renaissance Jewellery (08-12-2015)

Hi Saurabh,

Your and @Nirav8 doubts are very reasonable but since we are in business of separating the wheat from the Chaff, we need to give company a chance.

Debt- Equity ratio of company for last 10 years

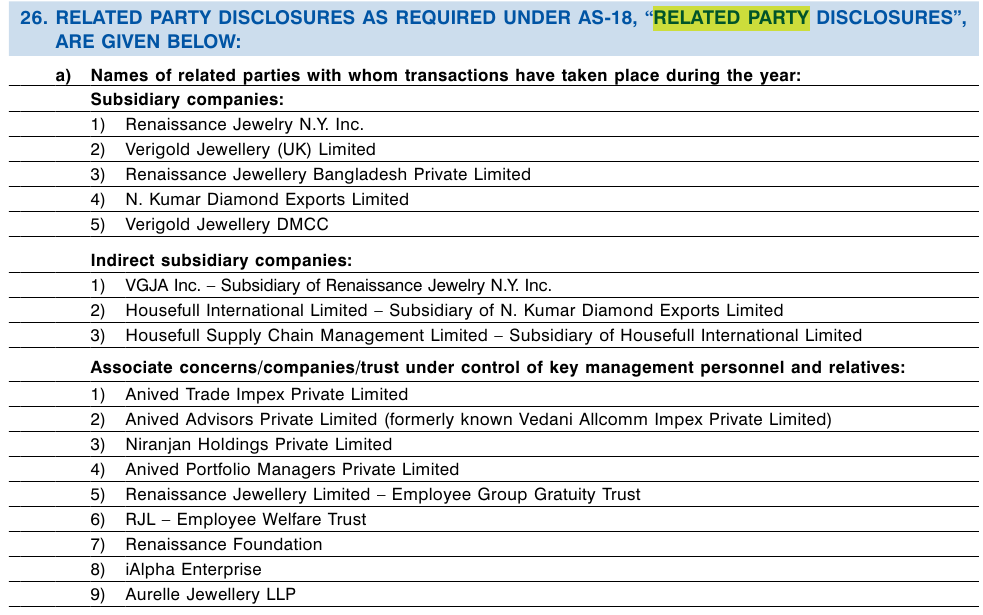

Related-parties according to AR 2014-15 are

The company has also details of related-party transaction in Annual report. Note 26 of note to financial statement. @constantseeker_ Can we use this information to cross-check revenue figures?

Tree house education and accessories ltd. – Potential candidate for improvement in RoE (08-12-2015)

Release of pledged shares:

Capital first has released all 44,600 (10.54% of total share capital) of the pledged shares.

Moneyball – what’s Baseball got to do with Investing? (08-12-2015)

Amazing post - I have been a big believer of charlie munger's horizontal thinking and your post got me excited.

A few points are to mull over are

- if you are a disbeliever and someone else brings in data based evidence, learn to trust it

- one of my biggest learnings is that the less gifted but passionate like billy beane - the extraordinarily gifted seldom make good analysts or coaches because the pieces come together so effortlessly for them

- making the change and wiating for it to yield results is the tougheest part of the process - people want fruits to be borne out as soon as they water the plants. How do you assess progress without seeeing the fruits of it is something no one has figured out completely. But like ian cassel says "if you are doing better than what you were two years back, you are on track" and not necessarily doing better than your perceived competitors. That's the tough part.

good effort !

Forensics and the art of triangulation (08-12-2015)

The report does not seem to be available - can you point us to the link?

Separately, I just read about the Olympus Scandal ( Wikipedia on Olympus Scandal) along with the book by the CEO; who infact became a whistle blower - Exposure - the story behind Olympus.

In a nutshell a fraud was carried for 23 years to hide losses as the Japanese bubble burst. Initial losses were attempted to be recovered by speculative investments; and such investments were doubled downed when losses increased. The Japanese had a nice sounding word for it called the 'tobashi'. However hiding ever increasing losses became more and more difficult as accounting rules changed. The fraud was perpetrated institutionally as the outgoing chiefs passed out the fraud baton to incoming ones.

Ultimately it became too difficult to hide and one incoming CEO, a gaijin (or foreigner in Japanese), a Brit, who was an Olympus lifer climbing the rungs from a salesperson blew it up.

The book talks more about the cultural turmoil, but an investigative report ( Official Investigative Report Summary ) lays out in some broad detail how the fraud was supposed to be hushed up in the books. At its core the idea was to smoothen losses - via amortising goodwill.

But as the amounts got larger, auditors balked, red flags were raised and the organized fraud was exposed and taken to completion by a dogged CEO.

NCL Industries – Resumption of growth? (08-12-2015)

Q2FY16 Nos. analysis by Nirmal Bang-

NCL Industries Ltd reported QoQ decline in operating profit due to seasonal volatility seen in cement prices. Demand across the Southern region continued to remain weak but price discipline is still followed by cement producers in the markets.

1. Revenue during the quarter increased by ~8% QoQ which is led by higher capacity utilization at 65% in Q2FY16 from 60% in Q1FY16. NCL continued to register healthy sales volume growth of ~7% QoQ and ~31% YoY to 2,41,396 Mnt.

2. EBITDA had declined by 18% QoQ to Rs. 32cr due to higher freight cost (Rs. 27crs in Q2FY16 vs Rs. 22crs in Q1FY16) and drop in cement realization at Rs. 6572 in Q2FY16 vs Rs. 6746 in Q1FY16. The decline in realization was due to seasonal declining in its key markets, where cement prices has seen correction of Rs.50 per bag. Cement EBITDA/tonne fell sharply by ~36% QoQ to Rs. 727/tonne from Rs. 1136/tonne in Q1FY16. General Administrative expenses increased by 85% QoQ to Rs. 14crs in Q2FY16 from Rs. 7.6crs in Q1FY16 which includes onetime expenses also increases in some variable expenses.

3. Freight/tonne had increased by ~24% QoQ to Rs. 849/tonne from Rs.735/tonne in Q1FY16 due to company entering new location which have lower realization and high lead distance.

Discl: Invested from much lower levels (10% of portfolio at present). As disclosed in Deccan Cements thread earlier, I had sold 1/3rd of my holdings in NCL at 160+, reason being portfolio top slicing from an allocation pov.

Note: I have just pasted the analysis of numbers selectively from the report. Report can be found here (Nirmal Bang NCL Q2FY16 Result Analysis).

Kind Regards.

Renaissance Jewellery (08-12-2015)

Hi Gaurav,

What you need to get is the debtor list of the company. Then you need to find which of these are related party/sister concerns/companies run by friends/family of promoters. that information is almost impossible to get most of the times. that is one of the reason for opaqueness of the industry and why it is so closed.

Once you have the information u then need to know other details like payment terms, who are end customers of these companies etc to really understand what is the actual sales.

The second risk is you will rely on inventory valuation given by company. Auditors don't audit the value of diamonds used :).

Having said that this is still one of the better companies in the industry. I know this since i had approached them multiple times to avail banking facilities from my erstwhile org :).

PS- they had a loss making retail venture. not sure whats happened of that. but u can check.

Overall, my comment: Too many variables where we dont get information or wont have information. Hence its a miss for me.

Deepak Fertilizers and Petrochemicals (08-12-2015)

I take your point

Was looking at the reason for fall in RCF and Chambal, and the news flashed on CNBC. They even interviewed Zuari Agro management on this  Lets see if the news is posted on their website

Lets see if the news is posted on their website

In any case, I take that as an opportunity to buy more of Deepak. In my opinion, the company is not so adversely affected even if the arrears are delayed. The risk of losing the upside on gas availability is higher. What I am concerned about though is the fall in commodity prices, which might delay an uptick in mining activity (negative for ammonium nitrate).

Torrent Pharma Ltd (08-12-2015)

Stock price movement is a function of the collective wisdom of markets. And its difficult to make out what moves the stock price.

But over a longish period of time say more than 6-12 months time frame, stock prices do tend to follow earnings.

In case of torrent market concerns may be related to the perceived lack of blockbuster molecules post these abilify, detrol and nexium. (I am not too sure what kind of concerns may be there in marketmen's thoughts)

But as I have written somewhere else, I am not too bothered about these temporary gyrations in stock prices especially when I am not on the lookout to raise funds by selling the stocks.

Usually the triggers for stock price rise esp sustained rise is sustained rise in earnings and high dividend payouts.

Both these triggers are still some time away.

Many a times its the positive surprise that moves stock prices. e.g better than expected earnings or order booking or any other kind of surprise that seems to be good news for the company