Even I am surprised by the comment that its under cyclical category. If we see its Price chart for long term…its a secular growth chart…not the cyclical up and down chart, barring 2018 to 2019 chart part

Posts tagged Value Pickr

52 week highs and all time highs strategy (31-07-2022)

The examples you have posted on chart are good examples of bullish patterns. You can edit the posts you have put up to put in your observations instead of just plain vanilla charts.

52 week highs and all time highs strategy (31-07-2022)

Andor Welding, Wkly chart, forming horizontal consolidating, I have not gone through fundamentals, anyone can thrown some light on the same

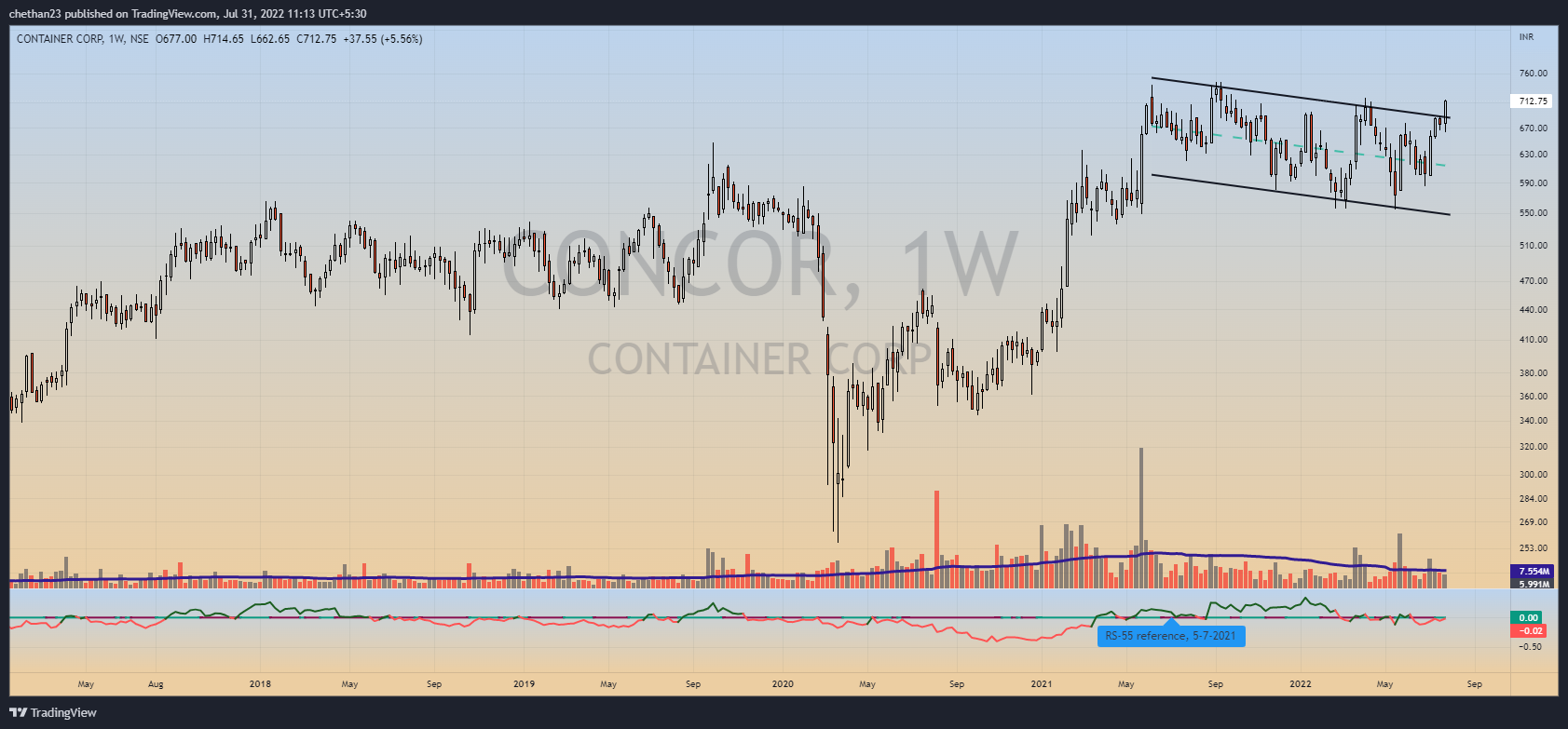

52 week highs and all time highs strategy (31-07-2022)

Container Corp, Wkly, Price has moved out of consolidation

52 week highs and all time highs strategy (31-07-2022)

@hitesh2710 Ji are these right way to look into technical, i am learning

52 week highs and all time highs strategy (31-07-2022)

Vinati Organics, Horizontal consolidation, price did move out, but did closing was not strong.

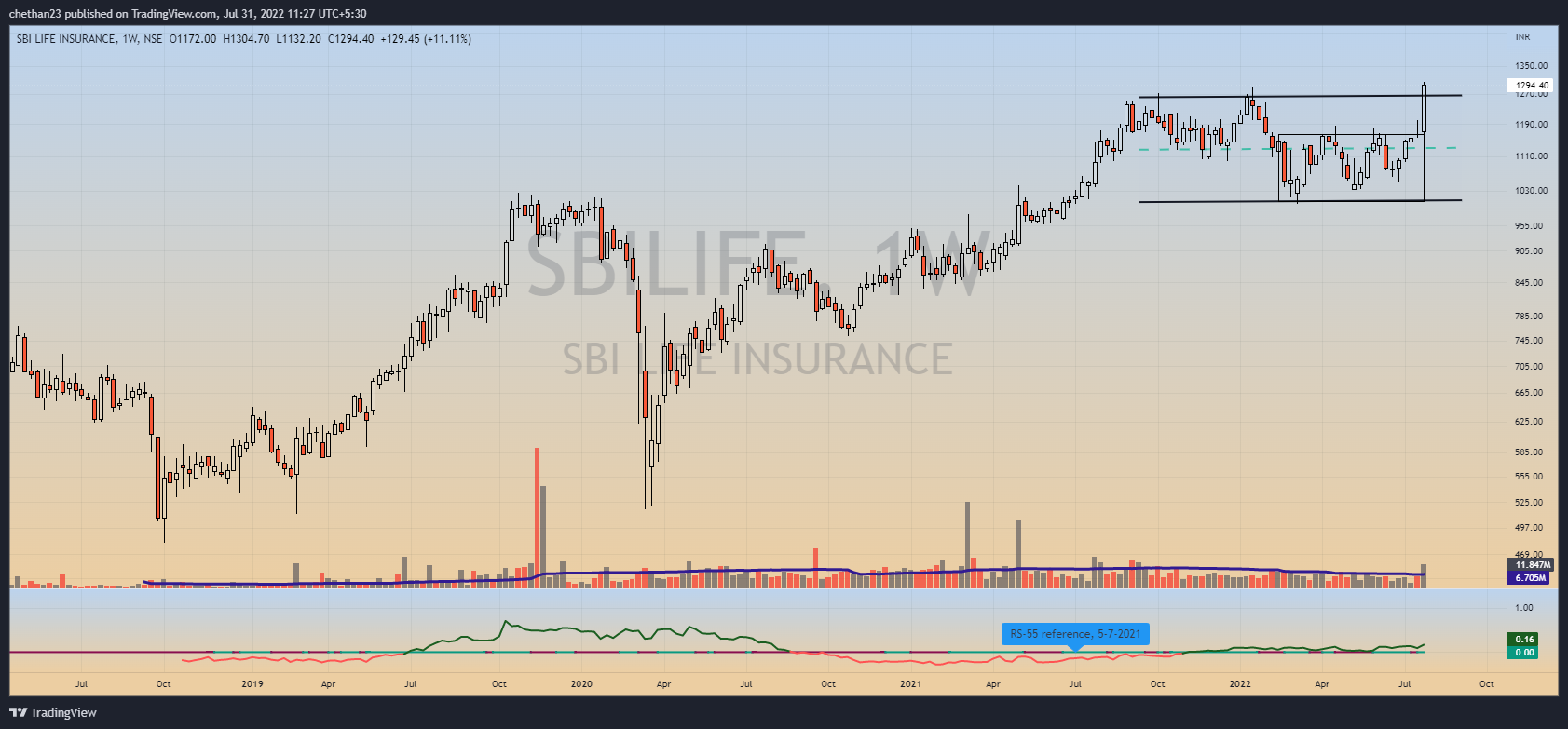

52 week highs and all time highs strategy (31-07-2022)

SBI Insurance, price has come out of horizontal consolidation, also this can be long term bet since many are opted for insurance after COVID

Hitesh portfolio (31-07-2022)

You can scroll back a few posts to see the views on Praj Inds. No use repeating same stuff again.

Regarding textile sector, you can go through concalls and latest annual reports (wherever available) of various textile sector stocks to get an idea about how things stand now. There are well researched threads on VP also regarding textile sector.

IDFC First Bank Limited (31-07-2022)

P/E might not be the best metrics to value banks as they tend to be cyclical. I think Indian market has not experienced this cyclicality in the private bank as some private banks have been able to capture increasing share from public sector banks even during lean years.

It is difficult to see IDFCFB getting valuation of higher than 1.5 P/B when banks with higher scale, profitability and consistent track record are also available at cheaper valuation compared to historical trends.

I believe larger Indian banks should start to narrow valuation premium with global banks over next 3-5 years as Indian market get more integrated with global capital market with growing size.

What will be incentive for someone to own combined HDFC bank at $200 billion valuation when larger and more profitable American banks are available at cheaper valuation.

Indian banks might have higher growth but valuation premium will start coming down with decreasing incremental growth especially in dollar terms.

Divyanshu’s Portfolio (31-07-2022)

Portfolio Update: My allocation to Bandhan bank is a mistake. I got carried away by the narrative that the bank is helping millions of poor people by giving them access to finance. While the narrative may be true, my job as an investor is to generate superior returns while taking acceptable risks. Not only is the bank geographically concentrated in east, it is catering to politically sensitive population. I feel that the risks I am taking here were much higher than my other investments. I will remove my exposure to Bandhan bank and add more to Dmart (I already did that with my personal portfolio, but since I have not announced it here, I will make the change in excel on 1st August)

I also want to reduce my exposure to Infoedge and add more to Nykaa. Reason being I feel Nykaa is more focused, while Infoedge is Naukri + a VC fund, and the VC business can suffer a lot more in case of recession.