Hi hitesh sir, could you share your views on laurus labs? This quarter growth returned in revenues and company posted good results. If possible can you analyse the chart? It will be a great help to me. Thanks in advance.

Posts tagged Value Pickr

Schaeffler India Ltd (30-07-2022)

My notes on the co. with some insights from Schaeffler India’s latest concall.

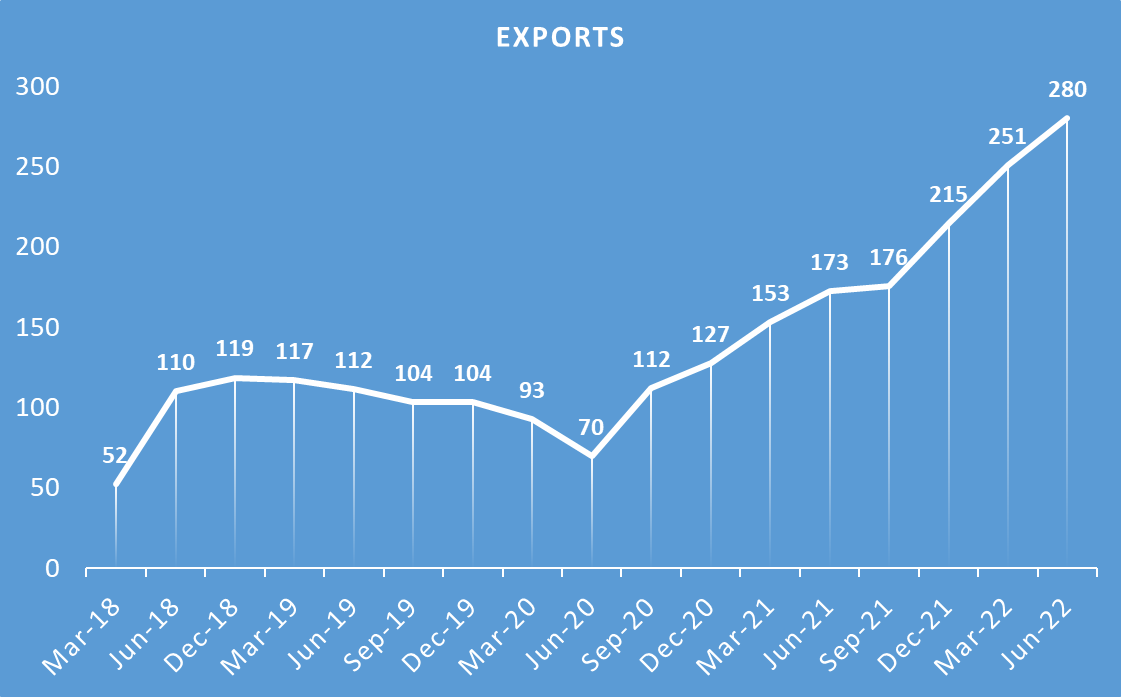

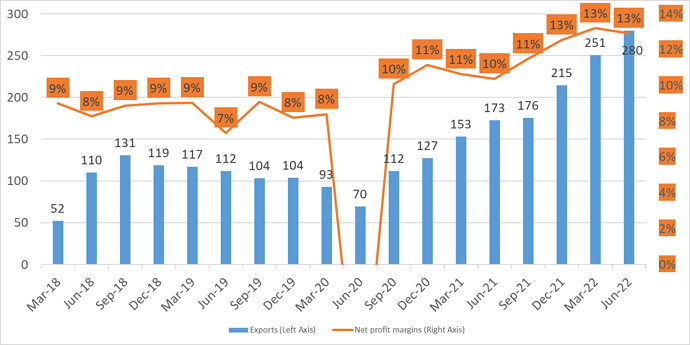

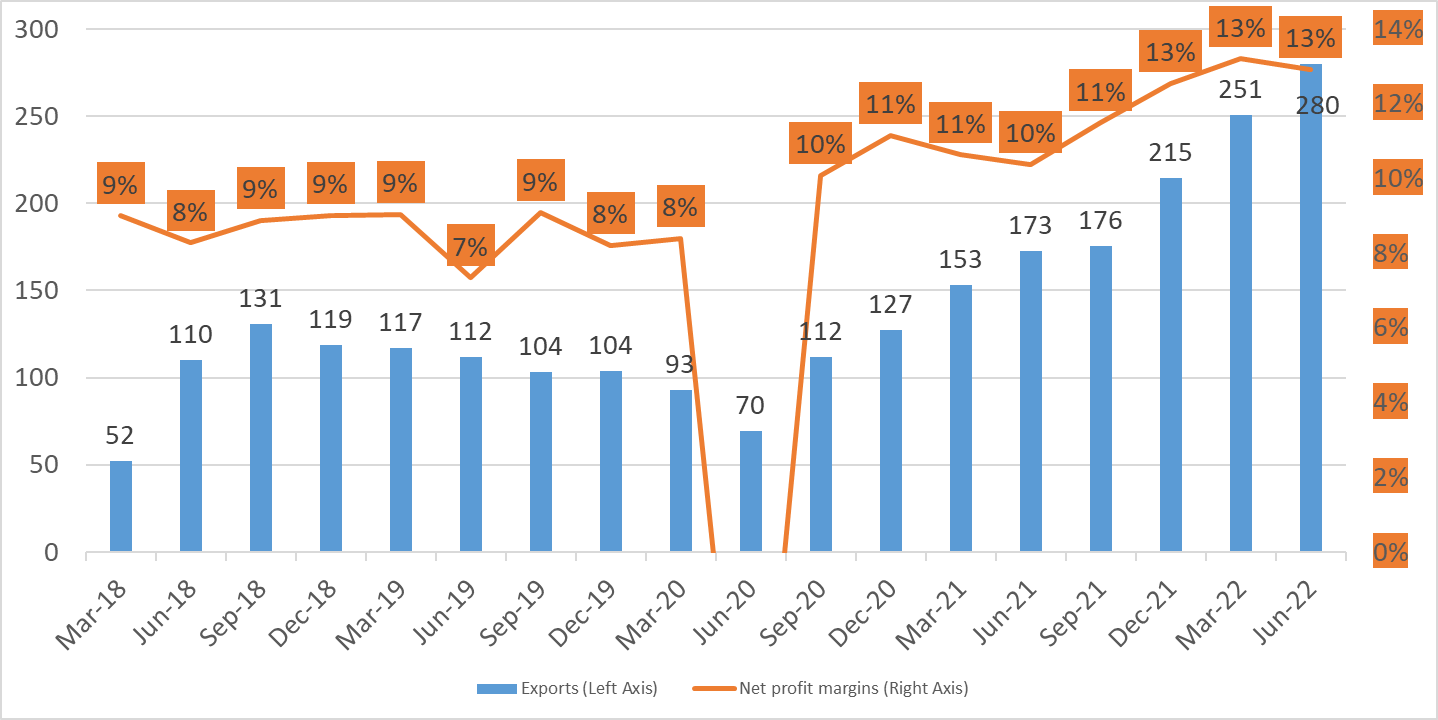

- Exports have been growing well since Sep 2020.

What is significant about the Sep 2020 quarter? Why did exports grow despite covid induced challenges?

-

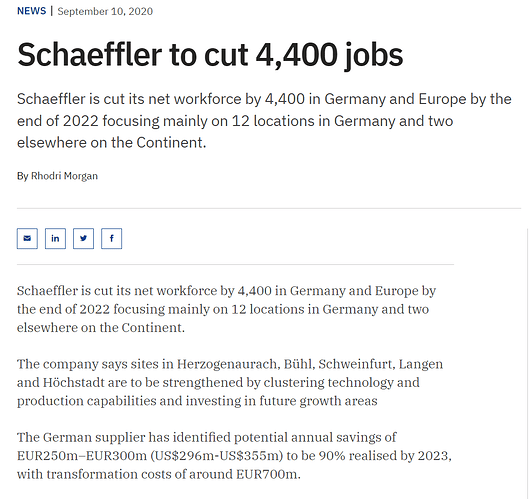

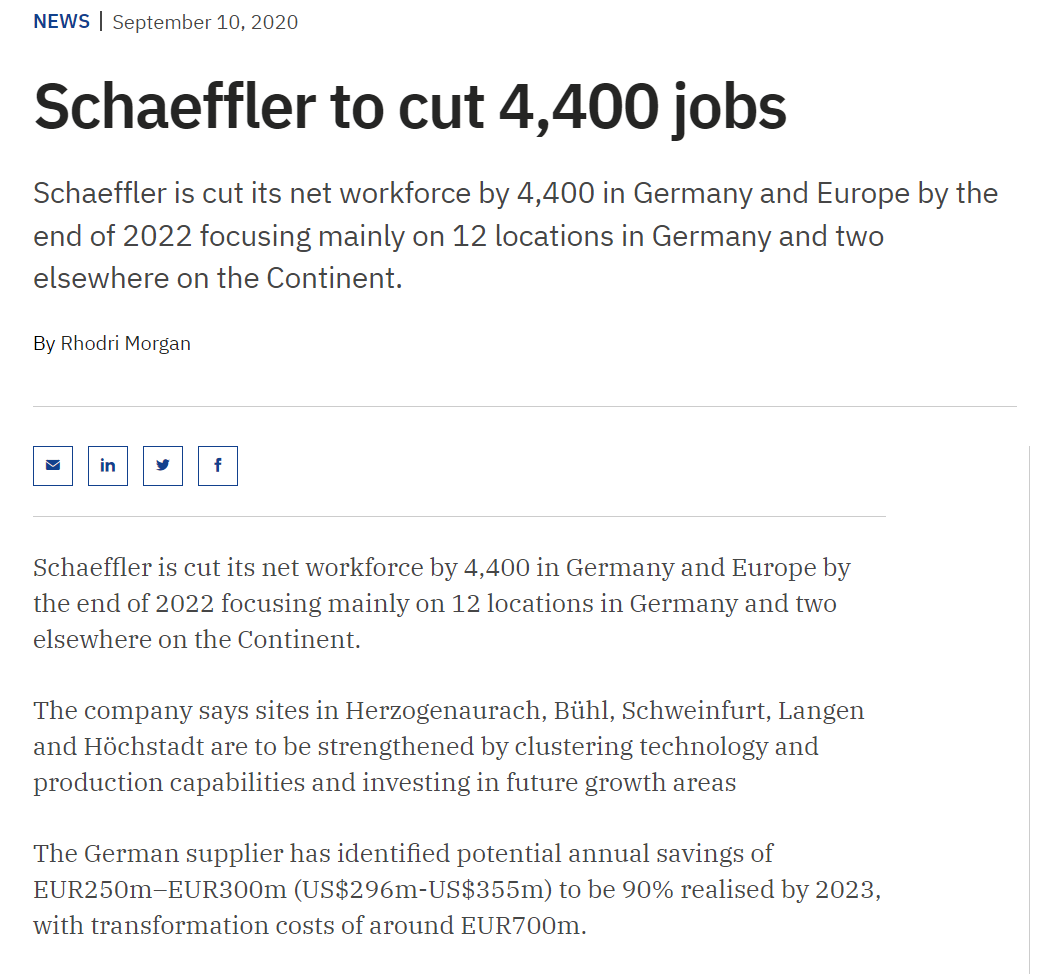

With the benefit of hindsight, in Sep 2020, the German parent, Schaeffler AG, decided to cut jobs and move manufacturing to lower cost locations (such as India).

-

Exports have been growing at a much faster clip than overall sales. Rolling 4 quarter overall sales growth of 28% vs exports growing at 63%.

-

Rising exports have led to a better margin profile.

-

Exports are now to all the continents, including Asia Pacific and North America and South America, where they did not have a significant presence in the past.

-

Their export product portfolio has been expanded as well.

-

A large portion of 150 Crs Capex in the June 2022 quarter was spent to increase export capacity.

-

They have a clear strategy for exports for the next few years depending on what product lines they want to manufacture in India.

-

Geopolitical issues in Europe could benefit Schaeffler India.

-

Scalability – To put things into perspective, Schaeffler India’s total sales (domestic + exports) were a tiny 6% of Schaeffler AG’s worldwide sales and how much of that could come to India is anybody’s guess.

It all depends on how much the parent gives to the Indian co and whether or not Schaeffler India has a cost advantage in manufacturing those products vs Schaeffler AG’s manufacturing locations outside India.

To summarize, growth is likely to come from

- New customers from new geographies

- New products

- Better margins due to an increasing share of exports.

Disc: Invested from lower levels. No transactions in the last 30 days.

Polycab India ~ Connection Zindagi Ka – W&C, FMEG and EPC Player (30-07-2022)

Congratulation for writing your first thread. great initiative. keep it up. After selling Havells, i am also tracking Polycab and KEI.

Investment journey of a late starter (30-07-2022)

IMO, the problem with retail investor lies in the fact they were always into the look out for guess paper, shortcuts, crash course, one night study to pass the exam at the cost of hard grueling approach of completing the entire syllabus by burning mid night oil through out the year. Well, the smartness of these folks do get highlighted for passing the exam in short span of time while doing all year round of fun and masti with mocking intent to those who strives passionately.

Result is all out there in all professional field. At the end of the day people seek professional expertise and excellence from those who committed whole heatedly to the cause of achieving excellence than to those who just acquired information in the guise of knowledge! In one line – there is no shortcut for achieving highest level of expertise, excellence or the mastery of subjects. One has to undergo though the funnel of sheer and frustrating hard work.

Krsnaa Diagnostics – what is the diagnosis? (30-07-2022)

Is anyone able to find any additional news apart from company’s intimation? I’m not able to find any other sources for any additional info.

Hitesh portfolio (30-07-2022)

Thanks a lot Sir for your knowledge and wisdom

Polycab India ~ Connection Zindagi Ka – W&C, FMEG and EPC Player (30-07-2022)

The customers are usually companies doing capex , So to show better capex utilization they procure much more during the end of the financial year. So the march quarter is the strongest usually and june quarter weakest

Hitesh portfolio (30-07-2022)

@lakshmikanth1 Sona BLW IPO came out during the IPO bull run which was prevalent few quarters back. A look at screener tells me that its PE is near 100 and June quarter results have been affected by margin pressure. Now companies quoting at near 100 PE are not allowed any mistakes. They can get away with some fancy explanations for a quarter or two but if even after that period results don’t match expectations, there can be a carnage in stock price. Often this kind of carnage goes from over optimism to over pessimism. If that happens, there can be an opportunity. As of now I feel I have better options to look at.

We have to realise that companies whose IPOs come out during IPO fancy periods often are over priced and over hyped. This is because there is a whole army of financial mercenaries working to sell the IPO at highly inflated prices. And managements/promoters often are working in collusion with these guys to give a rosy picture. Even the media, including social media, print and digital and TV media chips in intentionally or unintentionally to magnify this rosy picture. We have to remember that there are a lot of incentives at stake which you and me as retail investors are not aware of. So better to rely on wisdom of experienced guys like Lynch, who said that the full form of IPO should be understood as “Its probably overpriced. “

Regarding order book being 10 times FY 22 sales, we have all seen such stuff many times in the past. In the infra/real estate frenzy of 2006-2008, the biggest buzzwords were land bank and order book. ( I remember there was a term called book to bill ratio or something similar) A lot of companies in infra space were peddled based on this logic. And look at where those companies are… I guess a lot of them like Punj Lloyd and GVK and Gammon group etc have become penny stocks or have been delisted.

These kind of cycles keep repeating and keeps trapping gullible investors. That’s not to say Sona BLW is similar kind of company, but we have to be very careful when we invest in companies based only on their order book, or expanded capacities and so on and so forth.

Hitesh portfolio (30-07-2022)

As of now I do not see any bullish chart formations in PEL. The technical set up also is not too encouraging, the stock price being well below 200 dema in the midst of a strong rally in overall markets…

@Surender I do not track Novartis. Its leading products are well known but in pharma business, which is highly fragmented in India, well known brand names does not provide too much of an edge. Another company can come up with a copy cat product at much reduced prices and in India where a large part of patient population is non affording, this fact assumes a lot of significance. You can check prices of tegrital and mazetol both of which contain same molecule. Tegrital is the original molecule but because of very big price difference between it and other clones, doctors would prefer to prescribe cheaper alternatives to provide lower cost drugs to patients.

@Rafi_Syed How to analyse a pharma company is something beyond the scope of this thread. You will have to read up annual reports of companies which give out detailed information. Or else go through relevant pharma threads on VP. I recall @ankitgupta gave a presentation on one of our Goa VP conferences on pharma sector. You can try to locate his presentation and go through it.

@ram1984 I don’t track deepak fertiliser.

@Abhishek_Kumar_9 I haven’t looked at DP wire.

Shiny, New Stock-Market Tools (30-07-2022)

Consolidated sectors down to 127.

Broke up Banks & Financials into

- Private Sector Bank

- Public Sector Bank

- Other Banks & Financials.

Metals & Mining is now split into

- Iron, Steel & Ferrous

- Copper,

- Aluminium Copper & Zinc Products

- Aluminium

- Precious Metals

- Coal