does the current CMP justifies the total sales ??

cmp=₹ 172

sales ony rs 51.87 cr

Posts tagged Value Pickr

E2E Networks Ltd – Listed small Cloud computing player (29-07-2022)

Cigniti Technologies – Global Leader in Software Testing (29-07-2022)

A decent quarterly performance considering other IT sector performance. Will wait for their commentary and remain invested considering its niche space and growth prospects and current valuations.

Yes bank (29-07-2022)

Although would have loved to see dilution at 16 but management knows the best. Getting 8900 cr in current times will definitely boost long term performance and a decent yearly appreciation is assured from these levels.

Eris Lifesciences – 100% of sales from India Pharma Market (29-07-2022)

Can you share the link of Eris’ FY22 annual report? I haven’t been able to find the same.

E2E Networks Ltd – Listed small Cloud computing player (29-07-2022)

I have been tracking this company for more than 12 months now…two main problems

- Annual reports do not give any worthwhile input

- Float is very low which results in wild swings in both directions.

If some big player buys out the business (like Tata bought Tejas), this can get re-rated big time…But that is just hope (and hope is not a strategy).

I have token investment for tracking purpose. It is a capex heavy industry, and depreciation will also play a big role here…Let us hope management starts sharing more information going forward to help build enough conviction.

Yes bank (29-07-2022)

CMP is Rs. 15. Private placement @ 13.78. again many retail investors shortchanged!!

these PE investors are hedge funds who take large risks expecting higher returns – and they follow a portfolio approach.

for retail investors yes bank is a not a good investment – risk return wise.

also dont know what these funds are going to be used for as asset book has declined and so has every operating number!!

Anyway all the best to retail investors/ depositors/ etc…

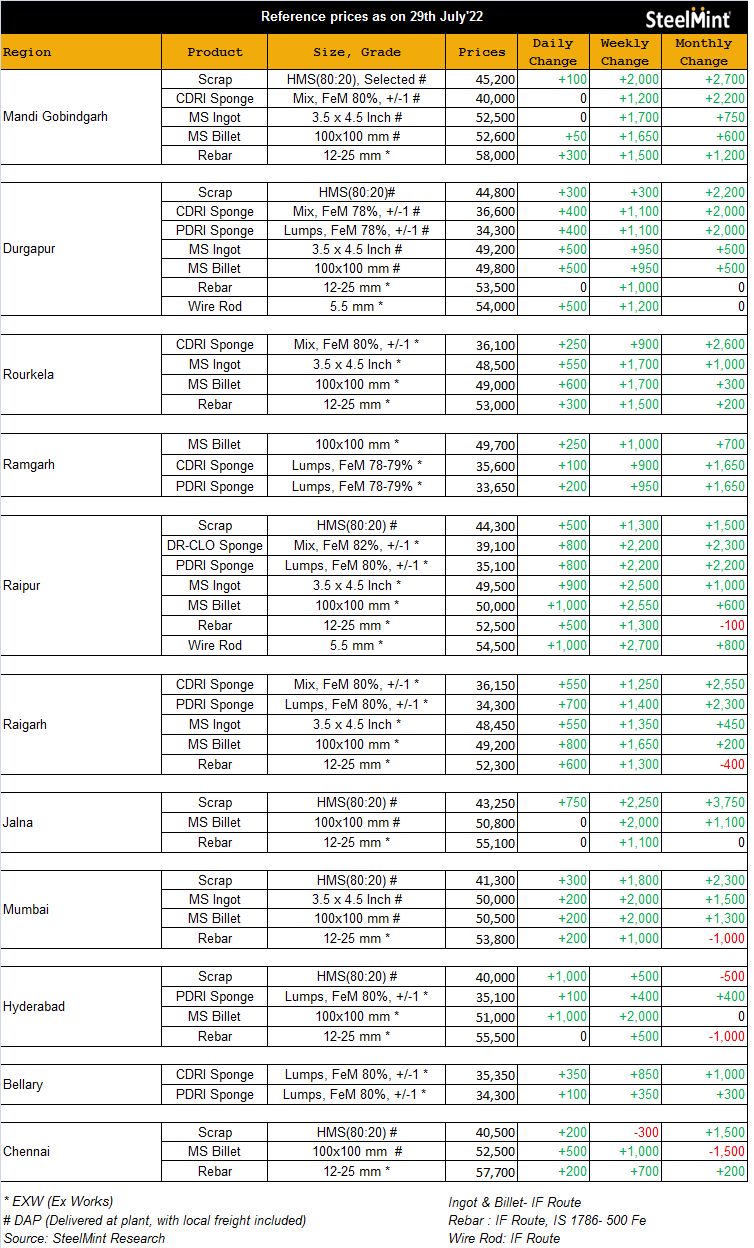

Godawari Power – Any Trackers? (29-07-2022)

Key takeaway from Presentation-

The pellet realization (3% down QoQ) and sales volume (19% down QoQ) both DOWN QoQ.

But, net sales is UP 16% QoQ, and EBITDA is also UP 16% QoQ.

Implies, majority of sales and profits is right now NOT coming from Pellets.

Prices of other products are pretty stable and strong.

No sharp fall in earnings expected unlike other steel companies.

Company should have 1000 crore cash balance by mid-term results.

From the investor presentation, one can make out the quality of management and their thought process of managing the company.

I find management quality and thought process far better than most other companies.

Big surge in prices today too-

Eris Lifesciences – 100% of sales from India Pharma Market (29-07-2022)

Company hosted an investor call with Bank of America and Abakkus PMS on 18 Jul 22.

Disc : invested, biased

Bull therapy 101-thread for technical analysis with the fundamentals (29-07-2022)

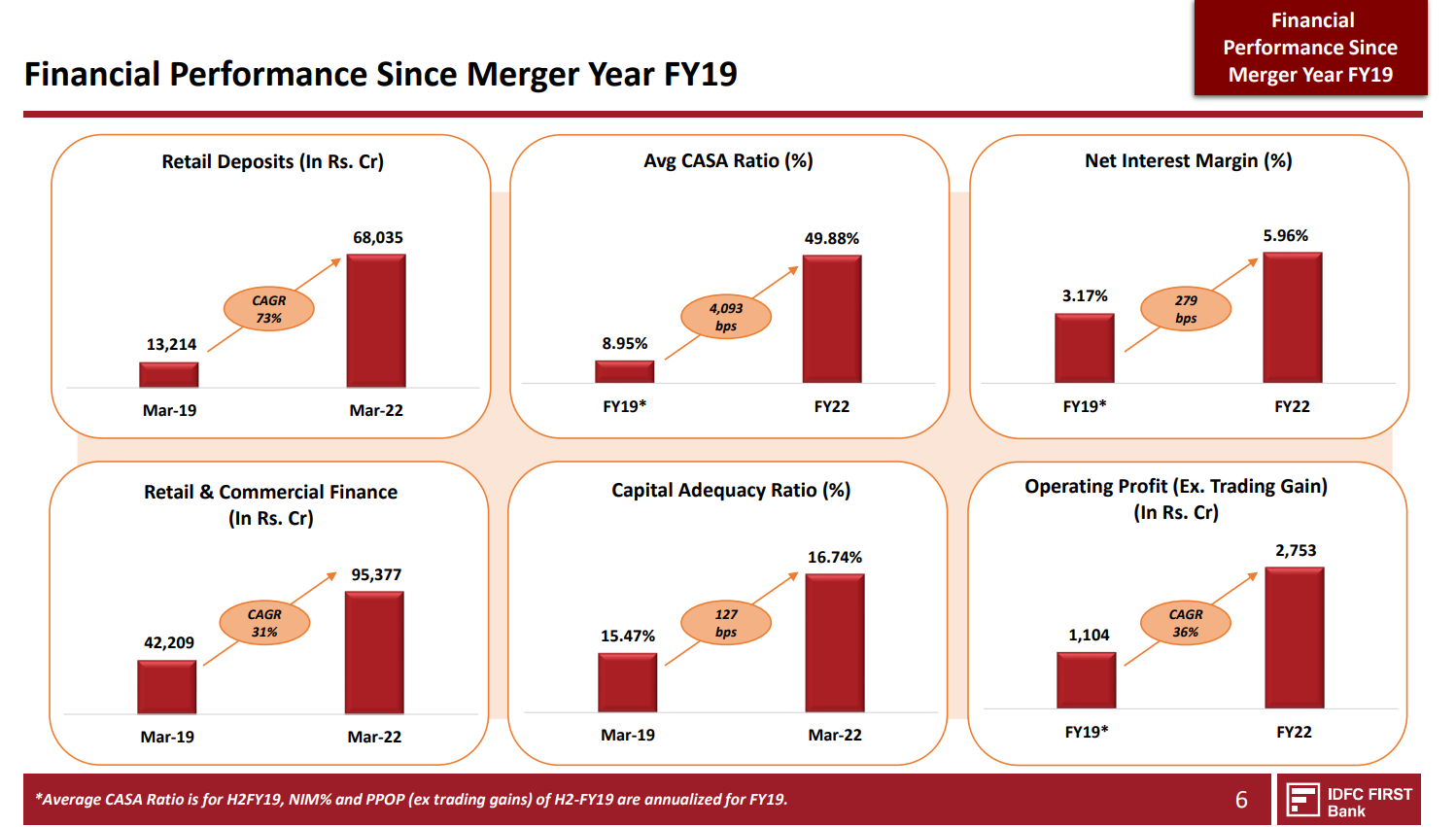

IDFC First Bank, Monthly – Has been in a downward channel for 18 months and has taken channel support at 30. July has closed convincingly above June open which is quite bullish as well. August will very likely be another green candle. If it has enough in the tank for a breakout post that, it can re-test Jan ’21 highs in 6 months. This scrip has extreme retail participation and has tested patience of everyone who has touched it in the last 5 years or so. Why should this time be different?

To understand, we need to go back to Jan ’18 when the merger of erstwhile IDFC Bank and Capital First was announced. The promoter who everyone should know by now, courtesy social media coverage for the stock, promised a lot of things. The promoter being very savvy in self-promotion probably added to the hope. Maybe market expected things to turnaround overnight but what transpired is one misfortune after another – as profligacy in infra, power, telecom loans from the past came home to roost, along with Covid.

In the intervening 4 years though, the texture of the business has changed considerably

That’s some seriously impressive retail deposit growth (73% CAGR), the CASA ratio is now 50% which is on par with the leaders in the pvt banking space, ICICI and HDFC Bank. This has helped the bank replace wholesale deposits with relatively cheaper retail deposits. NIMs have grown from 3% to 6% and retail loan book is now substantial.

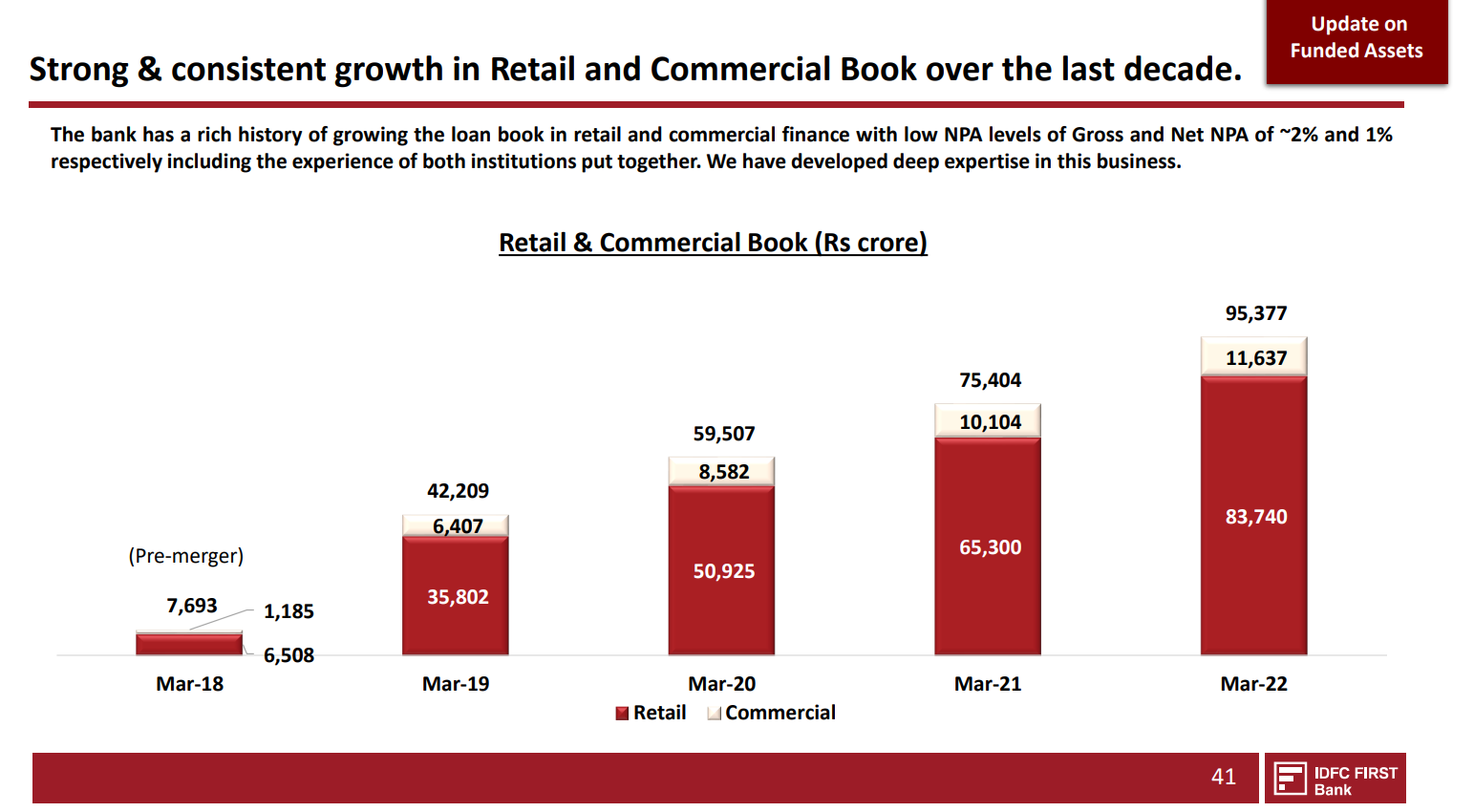

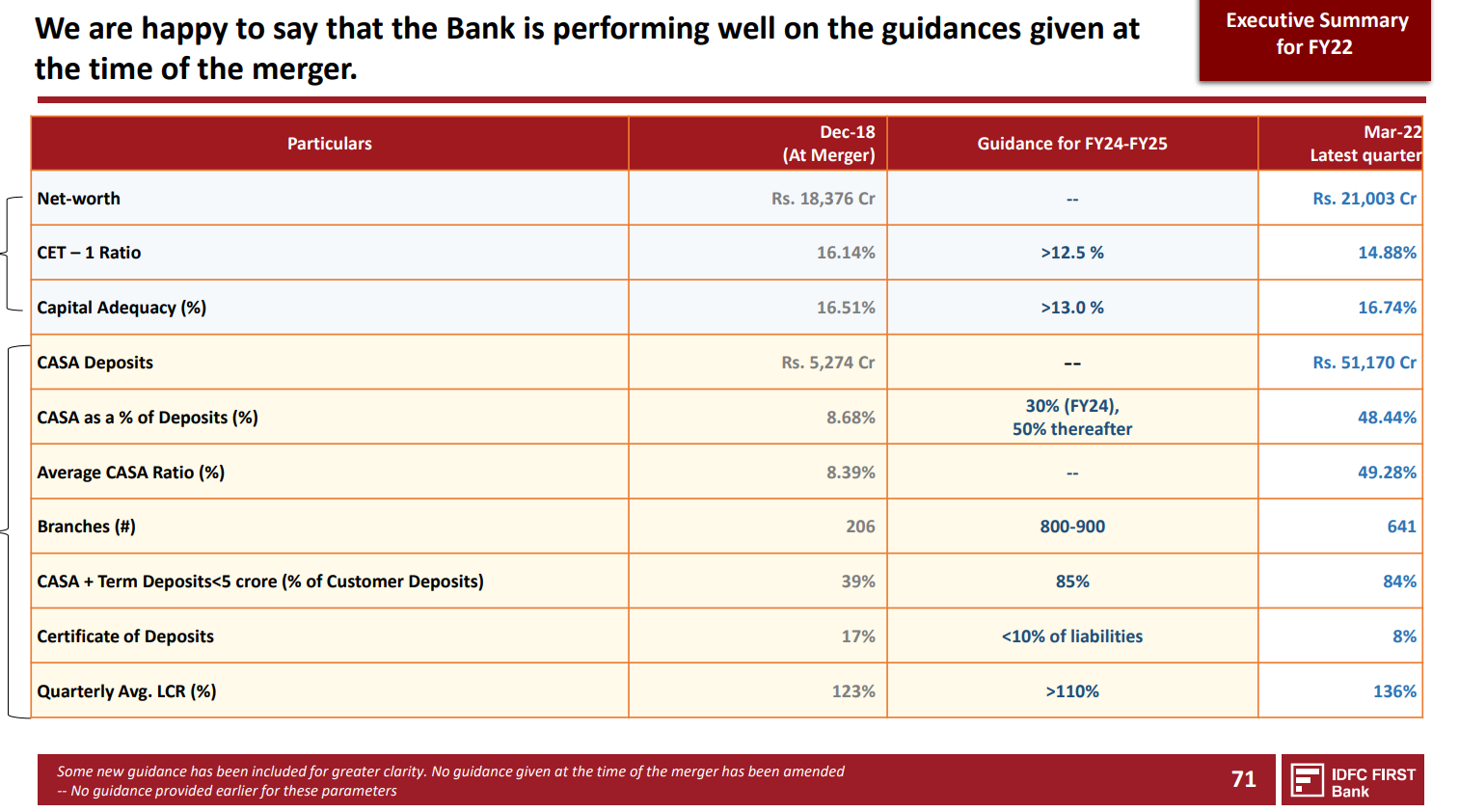

The bank has grown retail loan book considerably and has reduced infra financing (26k Cr to 7k Cr) and risky wholesale loans. Most of these are what the promoter appears to have promised in FY19 and th execution seems to have kept pace with that.

But the price has gone nowhere because all this matters for squat if you book value per share doesn’t grow and that has been the problem for IDFC First Bank. The net-worth of the bank was 18k Cr before the merger and is now at a meagre 21k Cr now. On top of this, to provide for all the troubles, the bank has had to dilute – the equity base has grown from 4800 Cr to 6300 Cr. So effectively, the BVPS has deteriorated from Rs.38 to Rs.33 during the period which explains the abysmal stock performance.

The business has spent its efforts in building a retail franchise which is not easy. It has roped in Mr. Bachchan, spent considerable sums in ads and promotions, grown from 206 branches to 641 branches and built a better CASA franchise and also better retail loan book. So the P/B I would be willing to give for Rs.33 BVPS in FY22 would be higher than the multiple I would have given in FY19 when the BVPS was Rs.38.

There’s a lot of scope for improvement in the business as well, as cost-to-income improves. There should probably be lesser negative surprises going forward, going by the provisioning done already in the past (courtesy equity dilution). The RoE should improve in the next 2-3 years which can make this trade at 2x P/B. The BVPS should grow as well with reduced provisions. So there are multiple things that can go right from here than wrong and there’s probably sufficient margin of safety at 1x P/B around Rs.33.

Risks:

- Large equity base coupled with unprofitable growth

- Loan book quality is an unknown unknown

- Further equity dilutions

Disc: Built positions between Rs.30 and Rs.35 which I thought was fair value. I am a novice and don’t really understand banking well and usually avoid it, so please don’t consider this advice.