Does it make sense to buy right entitlements since seller of rights have a huge profit to make when buying cost is only 10 rupees?

Also what price upper ceiling should we take into consideration when going for buying of rights entitlements ?

Does it make sense to buy right entitlements since seller of rights have a huge profit to make when buying cost is only 10 rupees?

Also what price upper ceiling should we take into consideration when going for buying of rights entitlements ?

(post deleted by author)

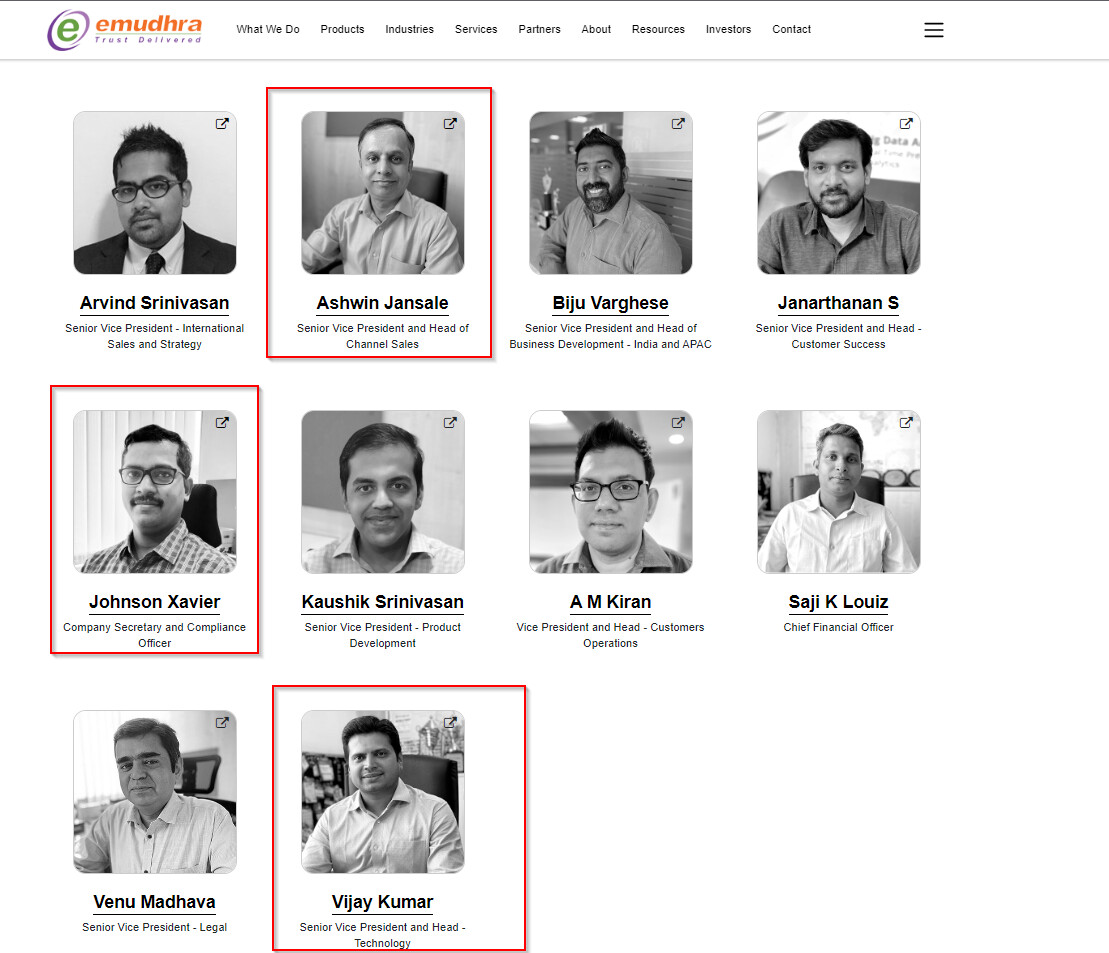

Interesting bit of things happened post Q1 numbers. Price Movement was rather steep and it looks like some of the very important KMPs have sold almost all of their holdings in this rally. This certainly does not gives me any comfort now as a shareholder.

exchange Filings of the open market sell :

One of them is the CTO of the company. One is CS and other one is SVP-head of Sales.

Views Invited.

Does anyone know what the 2.5 CR+ of other income this quarter and last represents . In prior periods, other income had never been meaningful

I think this type of searches are common. Somedays ago Hero Motocorp was also subjected to some raid (not search). Nothing happened. Anyway Krsnaa stock price already reacted to the news with 3% fall with minor volume.

Attended the concall partially. They reiterated many of these points – US pricing pressure slowing, other regulated markets and emerging markets growing, Endo launches picking up etc. Spoke about moving back to their erstwhile strategy of focusing on complex / difficult to make generics as opposed to “me too” products which they had resorted to post covid to balance the over-reliance on their acute portfolio.

They will bring the gross debt down to 1000cr by this year. Arun Kumar has guided for 20% EBITDA margins by six quarters, which is where they used to be pre-covid. Essentially the business seems to have made a clean bottom and should be on the way up from here, barring any unforeseen events.

Stelis is scaling steadily but no news on Sputnik money yet. I think we as investors should write it off.

Total paid 15 rs dividend for this year. And they sound more optimistic if one goes thru AR . They were waiting for Vietnam plant to stabilise and putting up new plant is good sign. Main IS 3.3 cr capital, 293 rs book value , 50 rs EPS and honest management.

DISC, INVESTED

and historically 2nd half is better than 1st half.

1500 KgPD Recycling plant along with the upgradation of POY lines has been commissioned on 29/07/2022

Thank you for asking great questions over conf – call …