NCF implementation could be the next big triggers as second hand market temporarily is finished.

Can be a huge trigger here, positive policy change

Disclaimer:- Invested.

NCF implementation could be the next big triggers as second hand market temporarily is finished.

Can be a huge trigger here, positive policy change

Disclaimer:- Invested.

Hello friends,

It’s been 9 years since I joined this wonderful community of selfless investors. Here’s my first attempt at initiating a thread on a business that I feel is potentially under-priced. The business is an auto-ancillary called Sharda Motor Industries Limited (to be referred as SMIL, henceforth).

But first, some initial caveats and disclosures:

Summary of why this business could be interesting:

—————————————————————————

Detailed Analysis

—————————

About the company

——————————

CMP as on July 28, 2022 – Rs. 736

Market Cap – 2183 crore

SMIL is an established auto ancillary company offering products and services in the following market segments:

It has also entered into the EV space through a JV with Kinetic Green, India. In the initial phase, the JV will focus on assembly of EV battery packs and BMS, primarily for 2W and 3W. It will also explore sub components that go into BMS.

Brief History of the company:

——————————————

1986 – Inception of SMIL

1998 – Foray into Exhaust systems for passenger vehicles with Chennai unit and agreement with Hyundai

2002 – Ventured into Suspension assembly business. Established R&D for exhaust system.

2010 – Established R&D for emission control

2018 – Entered a technical partnership with Bestop Inc. USA for manufacturing of roof systems

2019 – Eberspaecher and SMIL enter into a JV to manufacture CV exhaust systems in India. Eberspaecher brings in global know- how for the local market

2020 – To resolve a family dispute, demerged NDR Auto component limited into a separate listed entity.

2021 – Kinetic Green and SMIL enter into a JV for assembly of Lithium batteries along with BMS for Electric Vehicles – 2W, 3W and Stationary applications

Product Portfolio and market share

—————————————————

Competitive Landscape

————————————

As per management commentary:

[The competitive landscape requires more detailed work and the management claims need to be independently verified.]

Legislation tailwinds

——————————

The below slide from SMIL’s investor presentation captures the legislation tailwinds:

To summarize from the above slide:

Key Risks

——————

Financials

—————

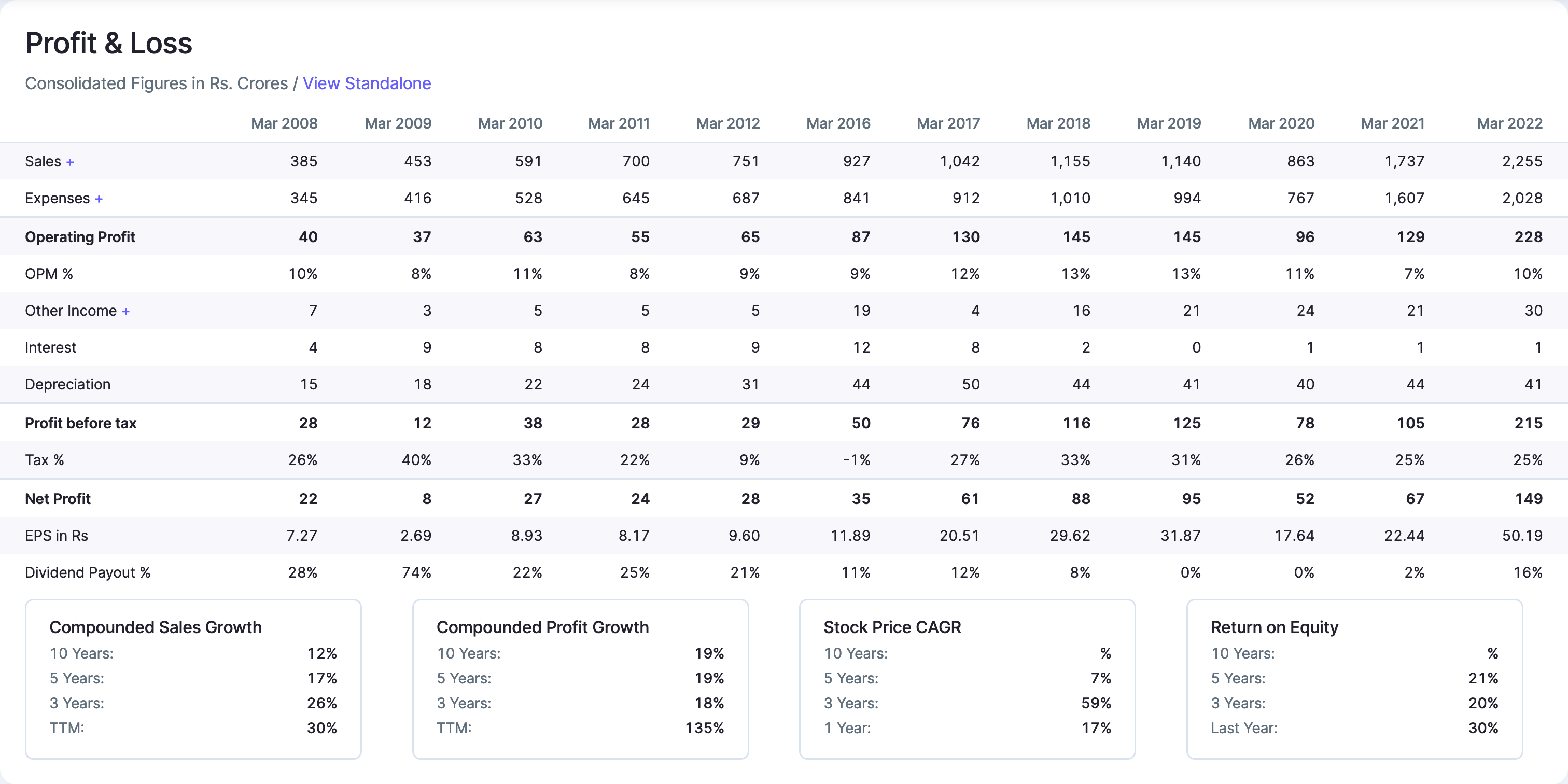

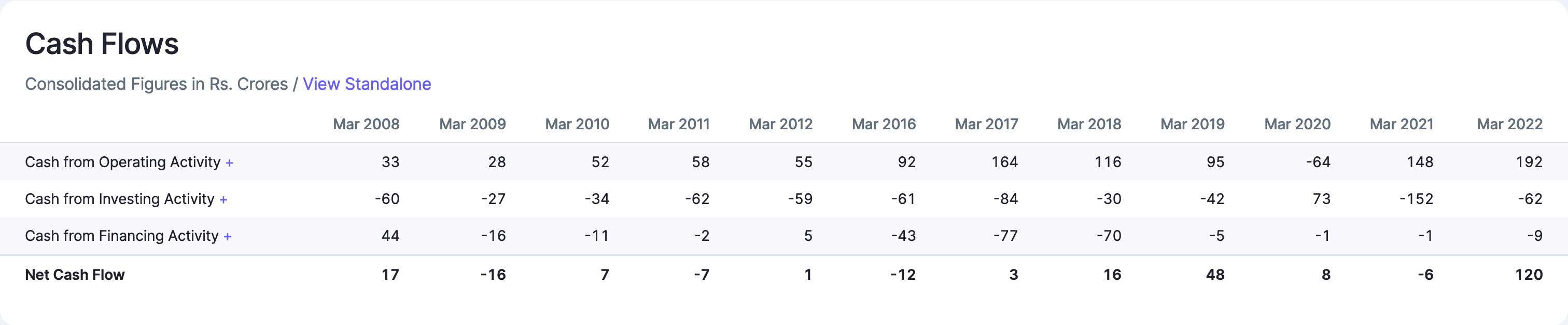

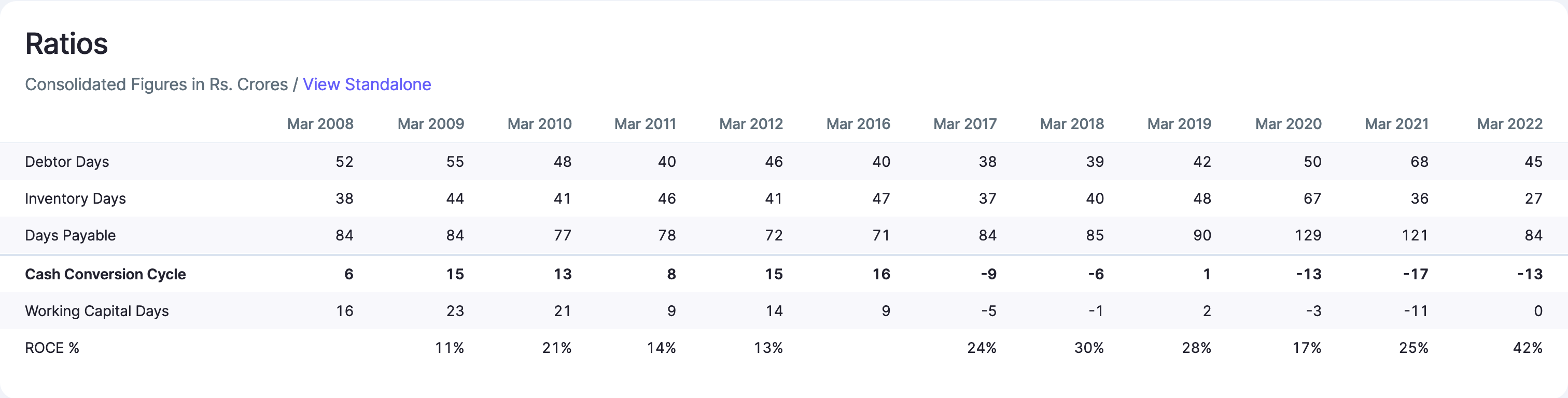

Pasting the screenshot of financials from screener below:

P&L

Cash flows

Ratios

Important things to note

The auto seating business demerged in 2020 as NDR Auto. Therefore, the long term numbers should be seen in that context i.e numbers before 2021 also include the seating business revenues.

In the auto-ancillary space, OEMs tend to have a bargaining power. It is notable that SMIL has a negative working capital cycle as an auto-ancillary. It indicates that they may have some bargaining power with OEMs in terms of receivable days and also with their suppliers in terms of payables.

ROCEs are therefore, high for the business as the capital employed is less due to negative working capital and high asset turns. Management has indicated that only incremental capex is needed to grow the business indicating lower capital intensity in the business. This needs to be investigated more.

CFO/EBITDA is > 84% for the last 2 years

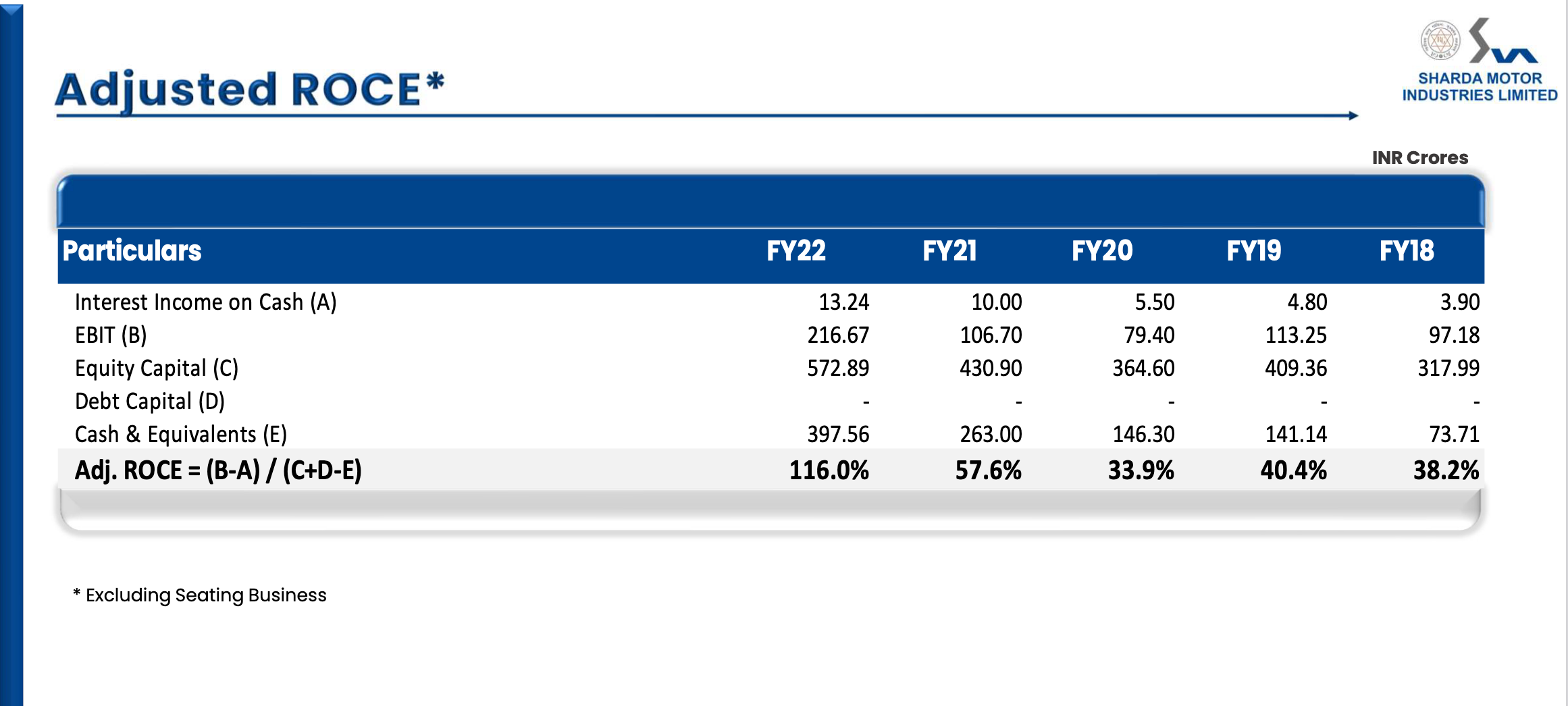

Management has provided a slide on adjusted ROCE excluding the seat business. Here is the screenshot:

As can be seen, the adjusted ROCE for last 2 years has been 57% and 116% respectively.

Valuations

—————-

Since SMIL is a net cash business, EV/EBITDA appears to be suitable valuation metric:

Current market cap – 2183 crore

Net cash as on March 2020 – 454 crore

EV – 1729 crore

TTM EBITDA – 228 crores

EV/TTM EBITDA – 7.5

Average EBITDA of last years – 178.5 crores

EV/Avg EBITDA – 9.7

The valuation range is [7.5 – 9.7] based on what one chooses as denominator.

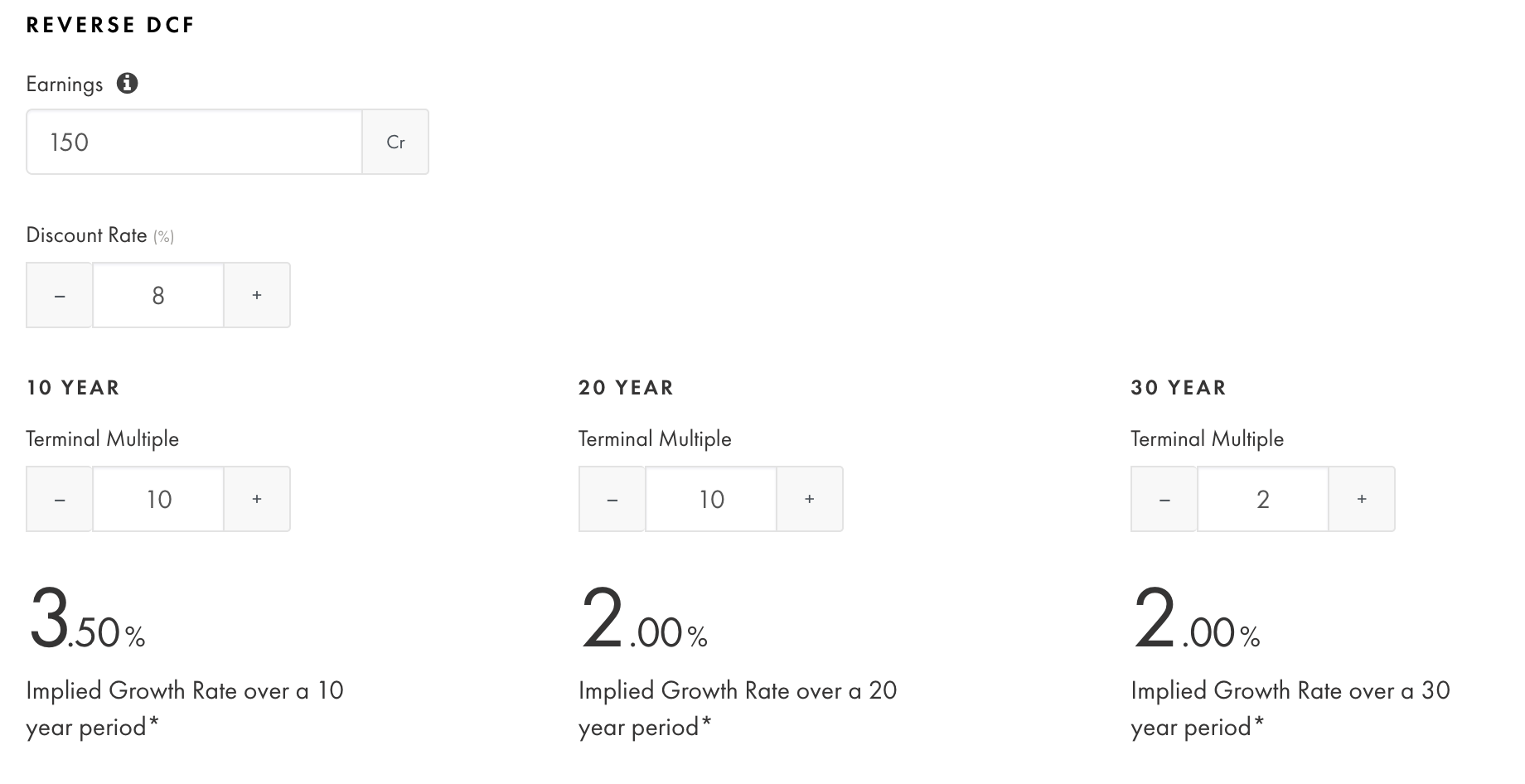

Reverse DCF

Missing pieces in the story

I have heard @Rokrdude in the conf calls and would be happy to hear his thoughts on this business.

Of course, since valuepickr is a collaborative community, I am looking forward to views from everyone.

Sources

Thanks for the clarification @TheWolf

You are missing inventory aspect. All cos increased inventory post supply chain issues because no one wanted a situation of lost sales. If the prices are dropping in Q1, the effect may be seen with a lag.

If I did not misunderstood then all pre-ipo shares will have 1 year lockin period from listing date (w/ few exception) and it does not depend on without or with promoter… This is to save retail so ppl do not come with ipo and offload their stake in short time.

Thanks!

What I believe is the major reason for fall in stock price is not just a weak quarter but change in perception of business , Tanla lost a chunk of revenue from a banking client which is a top 5 contributor of revenue to the competition, Majority of Tanla’s revenue comes from banks there is a fear that the competition might try to poach other large clients from tanla which can lead to severe distress , There is also a fear that there will be increasing competition in platform business .

However I believe the stock has already corrected alot , the company has good cash reserves and once the three deals on wisely start to materialize the dependence on enterprise business will be further reduced , This poaching came as a surprise for the company I believe they will now be prepared for other such events and even they lose a little margin in enterprise business it can be well compensated by platforms in the long term

Please let me know your opinion on this

Disc – Invested

break out above 200DMA with volume… on results…

margin jump

company : “Novartis India “

Novartis India reported huge jump in net profit and margin due to cut in employee costs (layoffs) and improvement in sales… as they have stuck a sales and distribution deal for some of their their branded portfolio of drugs with Dr Reddy labs “calicium sandoz” “diclofenac”…

source:Portfolio under Novartis-Dr Reddy’s agreement comprises over 30% of NIL’s turnover

extract form annual report.

“The Company has entered into an exclusive

sales and distribution arrangement for few

of its Established Medicines brands with

Dr. Reddy’s. This arrangement aims to

further broaden access of these medicines

beyond the current geographies to benefit

many more patients, more efficiently,

by significantly extending the reach of

healthcare professionals through an expanded

field force.”

@hitesh2710

Sir, my question…Can we see this as some kind of earnings based pivot to the upside in this neglected company with an improvement in ROCE, NPM profile along with sales due to the partnership with dr Reddy … ? can this leading to a new 52 week high ? thanks…

As it stands today, the stock is overvalued & is more volatile. Better to wait for the correction and buy?

@GrowingAlpha no need to apologise mate. As somebody who has a large portfolio position in Tanla and has suffered the brunt of this brutal fall, I very much appreciate sincere bear thesis presented in a calm and factual manner. I don’t agree with your interpretation of the Forbes article and will detail that out tomorrow, but appreciate the evidence based cautions. I hope to write a detailed post tomorrow about the developments of the past few weeks and my thoughts on them.

Sincerely believe its very important to hold the anti thesis pointers closer to one’s chest than pro thesis pointers especially in scrips where position size is large.

Will delete this post soon.