The news is dope!

For the profit, is there hope?

- How certain are we that this opium processing will really result in profit?

- Having Govt. as a customer has its problems

- It is good to notice that management is exploring new avenues

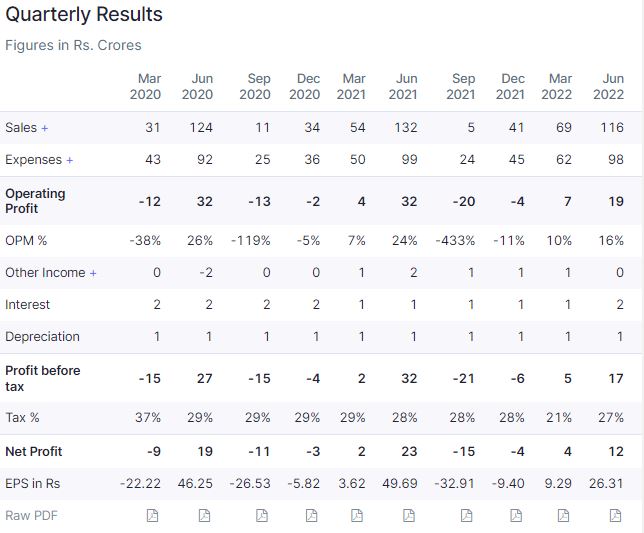

- They certainly overestimated its business guidance for FY22 surfing on the COVID wave…and that shows their unreliability

Disc: Tracking