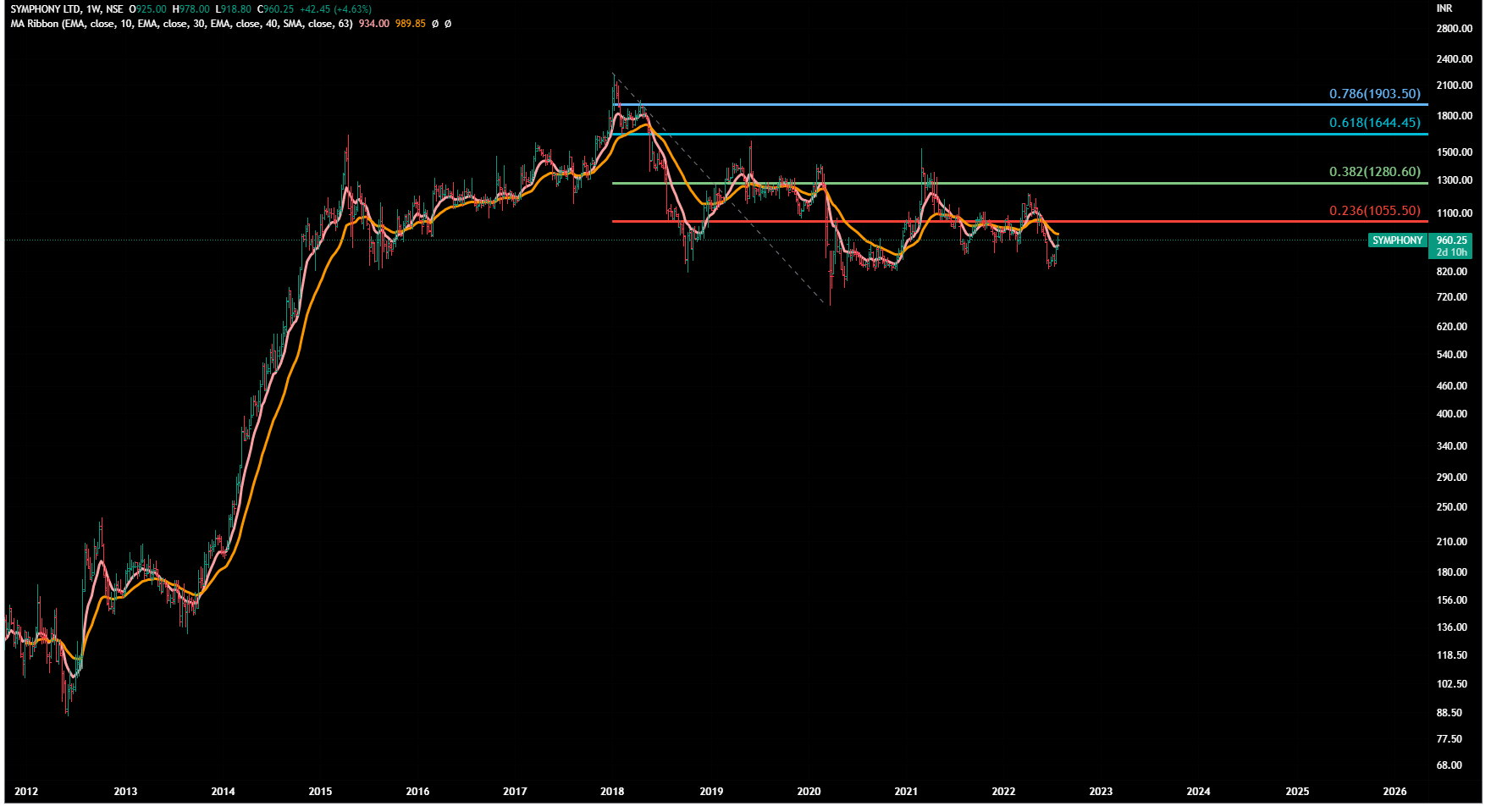

Symphony

Another stock that falls in my should-avoid list.

Weekly Chart :

a) Could not cross 61.8 % of its decline since Jan 2018 (even in 2years bull run)

b) Lot of ups and downs around key moving averages (10 WMA, 30 WMA)

c) No clear impulse (as per EW)

On monthly charts –

a) Trading below 40 months moving average

b) Could never cross 61.8 % of its latest declines (3 times) in last 2 years

c) RSI never crossed 60 in last 3 and half years.

d) Just taking support at a key level -any break from here can be brutal

Disclaimer : Charts are for study purpose. Opinions are personal. No suggestions, no recommendations.