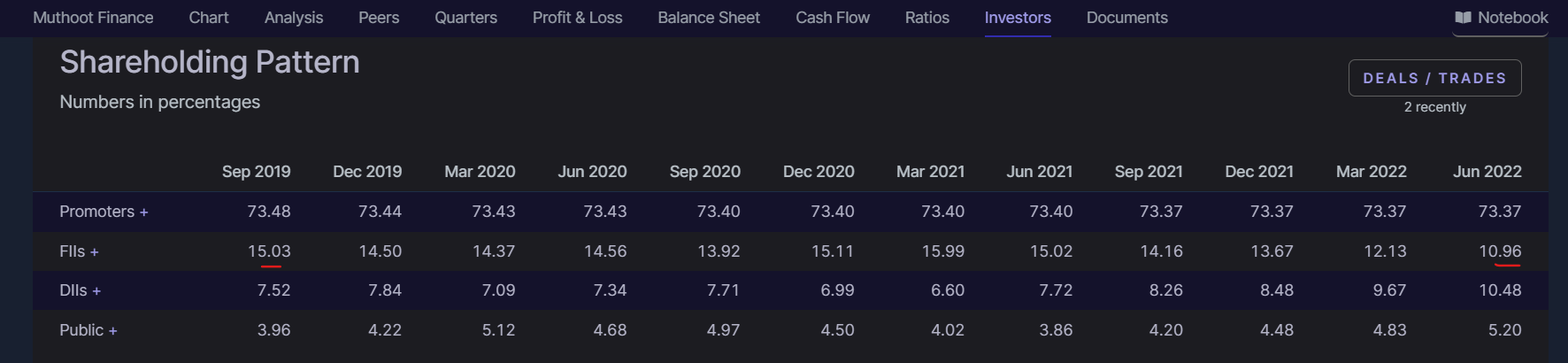

FIIs have offloaded 5% of their stake…

FIIs have offloaded 5% of their stake…

did anyone attend the agm. If yes will be great if can share the notes

I think it will be SNC, under “Talent Pipeline as a Service (TPaaS)”, where they kind of build pool of job ready employees by training them.

Cross-posting my notes from Tatva Chintan Q1 concall in case some folks following this company are keen.

Concall: Tatva Chintan Pharma Chem Earnings Call for Q1FY23 – YouTube

Investor PPT: https://www.bseindia.com/xml-data/corpfiling/AttachLive/5605c8a3-6517-4977-b734-c11ac57ad8bd.pdf

My notes on Q1 FY23 concall:

SDA

Guidance for FY23

PTC

Guidance for FY23

Electrolyte Salts

Guidance for FY23

PASC

Guidance for FY23

Flame Retardants

Guidance for FY23

General

Guidance for FY23

Estimates for FY23 based on above commentary turn out to be not too bad actually. With non-SDA segments, growing 60%, if they manage to get ~200Cr from SDA (10% degrowth), you are looking at ~20% topline growth and ~30% bottomline since SDA is high margin. Now that Dahej tax holiday has ended, bottomline will come down a bit and needs higher SDA share to alleviate that. With Q2 to be marginally better for SDA, overall numbers might look subdued until Q3 when additional capacity, renewed demand and new product revenues kick in. I see this as temporary pain for 2 quarters which will hopefully bring TCPCL down from stratospheric into reasonable valuation range.

Disc: Not invested. In my watchlist to invest when valuations are reasonable.

New Engagements ( TCV of new engagements won during the Quarter : $ 155 million)

KPIT expands its team and global infra-structure footprint

The vehicle manufacturers are aiming to earn revenues over the life of the vehicle for sustainable growth. This change will be enabled by CASE and centralized architecture programs, essentially Software Driven Vehicles. KPIT is uniquely positioned as a software integrator, helping global OEMs accelerate this journey. We have started the year on a positive note with an all-round performance, with growth in-line with our plan and healthy margin expansion, despite cross-currency headwinds. We remain optimistic on the overall growth environment

This message is for those who think that technical -analysis is for lesser souls.

Ujjivan Finance chart was telling in advance that something is happening and was giving signals for upmove.

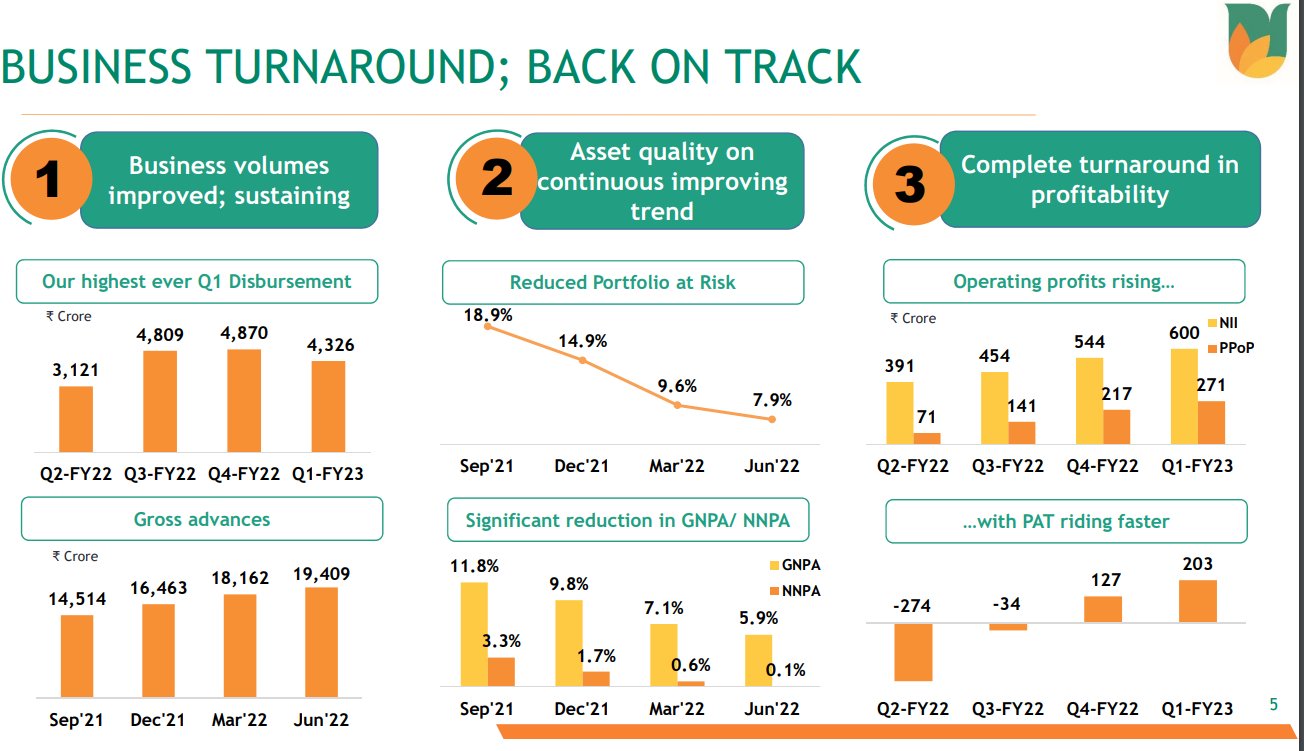

Look at the results declared today.

PPOP at 271cr vs 161cr,

Q4 at 217cr PBT 271cr vs -312cr

Q4 at 173cr GNPA n NNPA sharply lower QoQ n YoY

In short – any work that is done passionately (and if one tries to go into depth ) has value.

do you genuinely think that the price might run as lower as inr 40/-?

It has been 12months since this post – we don’t see much change in Techno Electric. In fact it seems to sink with the buy back from open market at INR 325/- or lesser. Every now and then, we hear them saying on their concall that their capex has been completed and the results will start showing up, but we don’t see much earnings in subsequent results.

Ujjivan Finance – Follow-up

Covered 8 days back at 156, CMP 174.

Today H & S got active – target for H & S is 220 .Key resistance is at 185.

Disclaimer: Charts are for study purpose and to track the probabilities… They may or may not work.