The trio of BSE PTC and ICICI has what it takes to counter IEX , unlike BSE vs NSE monopoly.

Posts tagged Value Pickr

Manjunath.c.a’s (CAMS) PORTFOLIO (26-07-2022)

Thanks for the Suggestion. As of now, Added HCL & TECHM as Tracking Position Only. Will study HCL/TECHM/LTTS/ELXSI further before adding it.

Indian Energy Exchange (IEX) (26-07-2022)

It is good to see that PPAFS has not reduced. What is good to see is DII have increased with increase coming for mirea

Invested and biased

When Not To Buy (26-07-2022)

For me, Valuation is the foremost parameter. If a company fails this parameter, then no matter how great it is fundamentally, I will not look at it. Just cannot accept the avoidable risk of multiple contraction plus low valuations would give margin of safety against unforeseen future circumstances.

I have Two Category of valuations depending on the type of business.

-

For non-moated businesses (average businesses) – BUY when price is at-least 25-30% Discount to Intrinsic Value calculated based on AVERAGE HISTORICAL EARNINGS (Avg ROCE, Avg EBIT margins etc.).

This ensures that we have two tiers of margin of safety.

One is the flat 30% discount Demanded on intrinsic value.

Secondly, By using AVG Earnings power, we can buy when the earnings are on the lower side of the avg, thus giving a chance for reversion to mean (A very powerful and persuasive phenomenon) and also protecting on the downside against further earnings decline. (some basic business analysis is of-course required to figure out where in the cycle earnings are currently and what are the catalysts for mean reversion) -

For Strong / Moated Businesses – Buy at Fair Value, usually 10-12 EBIT/EV Multiple, so that we get all the future growth + Multiple re-rating chance for free.Here numbers are of secondary concern and business analysis the primary. Significant judgement about business fundamentals, industry dynamics is required to determine the strength and sustainability of competitive advantages. Thus, if a company passes the business analysis test, then buying it at fair static intrinsic value would give us all the good things about growth without having to pay for it!

StageInvesting +Elliot Waves (26-07-2022)

Wondrela Holidays

All signs of a should-avoid stock!

Many a times technical -analysis skills can help you to keep away from highly recommended, highly tracked ,high pedigree stocks.

This one falls in that category.

A quick look at the monthly chart can tell you a lot of things ![]()

a) Look at the size of the upper wicks of the candles ! Sellers come running in as soon as it tries to move up.

b) A storng resistance ( red line) , that happened to be a support -level till Dec 19.

c) RSI never went above 60 on monthly charts for the past 5 years- above 60 RSI indicates that there is momentum in buying interest .

c) All upside movement from Covid -lows is overlapping, no clear impulse wave ( as per EW)

On weekly chart – as per stage analysis, lot of up & down movement around key moving averages (10WMA,30 WMA) , Not able to break the trading range for ast one year.

In short – Basic technical-analysis skills can help oone person to stay away from traps.

Disclaimer : Charts are for study purpose only. Opinions are personal, can go wrong. No suggestions ,no recommendations.

Wonderla Holidays (26-07-2022)

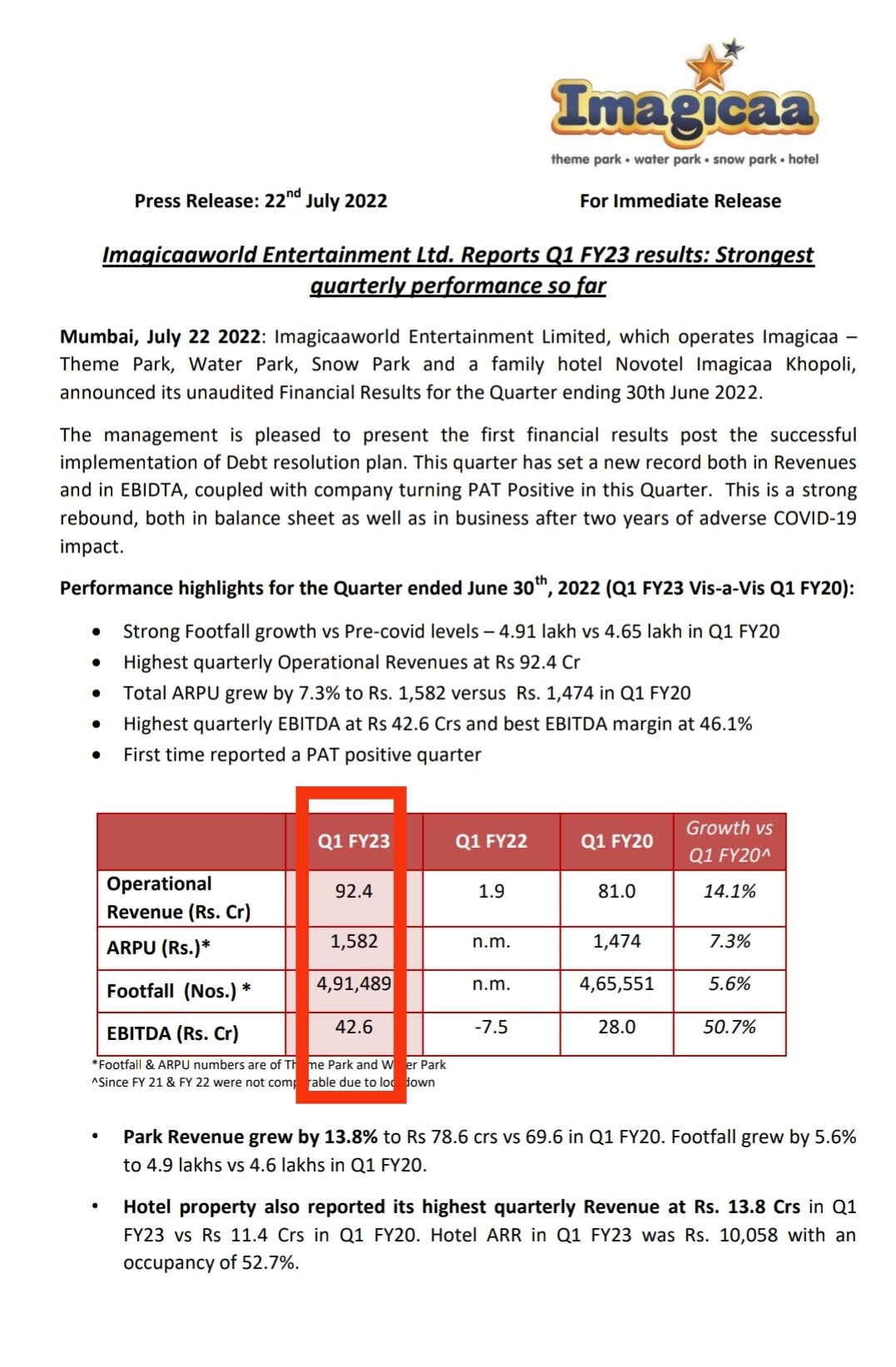

Looking at imagica’s (loss making co since inception) footfalls one can make a good judgement as how the quarter gone by was…also mcap of imagica is 830 cr today in comparison to wonderla which is 1300 cr today with zero debt and three parks in operations. No brainer!

Wonderla Holidays (26-07-2022)

Was going through their earnings call. Thought I would summarise it here, which touches on some of the topics including marketing.

Concerns:

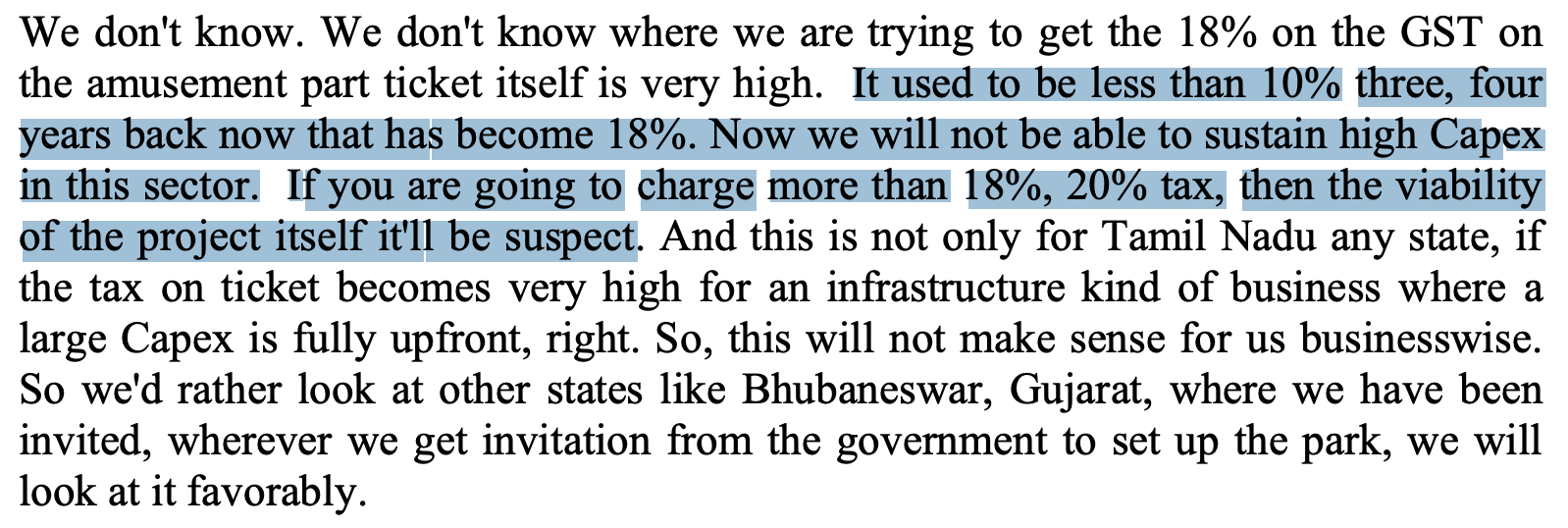

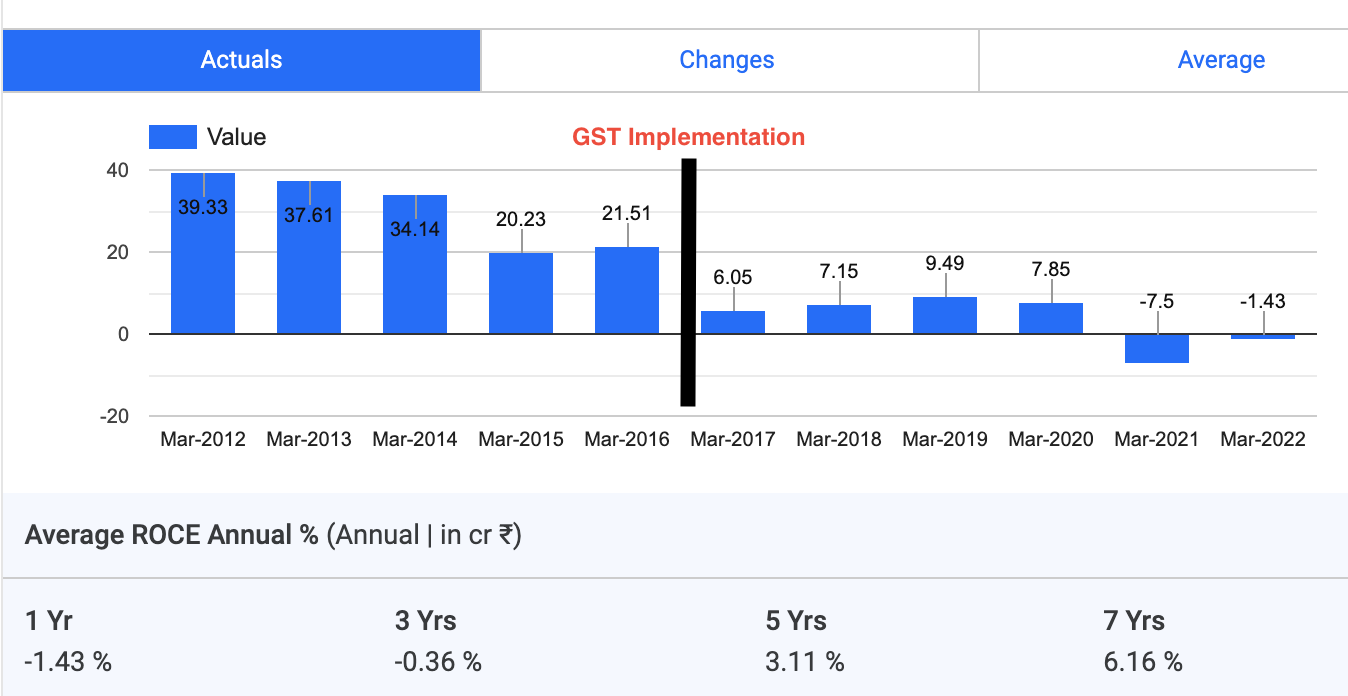

Implementation of GST seems to have material impact, especially in Chennai. This would result in high ticket price that would test customer’s willingness to pay.

I dont know if GST is the prime reason to have resulted in low ROCE.

On the willingness to pay, when they expand the capacity, the price should come down as they need to attract a lower income people. This is a significant constraint on scaling out vertically. If I am right, the current strategy is to scale to multiple locations and target the higher income group that pays more for tickets. Rest is dependent on economy growth.

Tailwinds

It is interesting to note that the company is entering into digital advertising only now! But, at least they are in right path and not beating around the bush on that.

If things augur well, then there can be some good volume realisation through targeted marketing and improving customer relations.

However, there is a limit to success here. Each park can only grow to a certain peak volume. The key is to improve non-peak volumes and improve ARPUs.

But each park can be expanded to handle 3 million, provided the footfall picks up.

There is a good scope for expansion across regions. If ROCE is stabilised, this is a very good long term play.

What I like the most is the capital preservation, provided if management is good and ethical (which they are IMHO).

Views

Overall, I think the next 2-3 years are going to be a good year for them as long as there are no macro economic issues. The management is good and is quite conservative in their strategy, which is important for an capital intensive company.

Disclosure: Have a tracking position. Might scale up over next qtr

StageInvesting +Elliot Waves (26-07-2022)

Thanks for checking.

1st one quick insight- stock-price of every company moves into cycle (we all know that ) . Now during down-cycle , it has two elements ( a) price-correction (b) time-correction ( price moves with -in a range) . Stronger the company, longer the time -correction and lesser the price -correction . The purpose of both of these type of corrections is to frustrate the non-serious investors , the free -riders (in layman’s terms) .

Many a times when price runs ahead of earnings (due to future growth projections), either the price should correct or it rests in a range to catch-up with earnings growth.

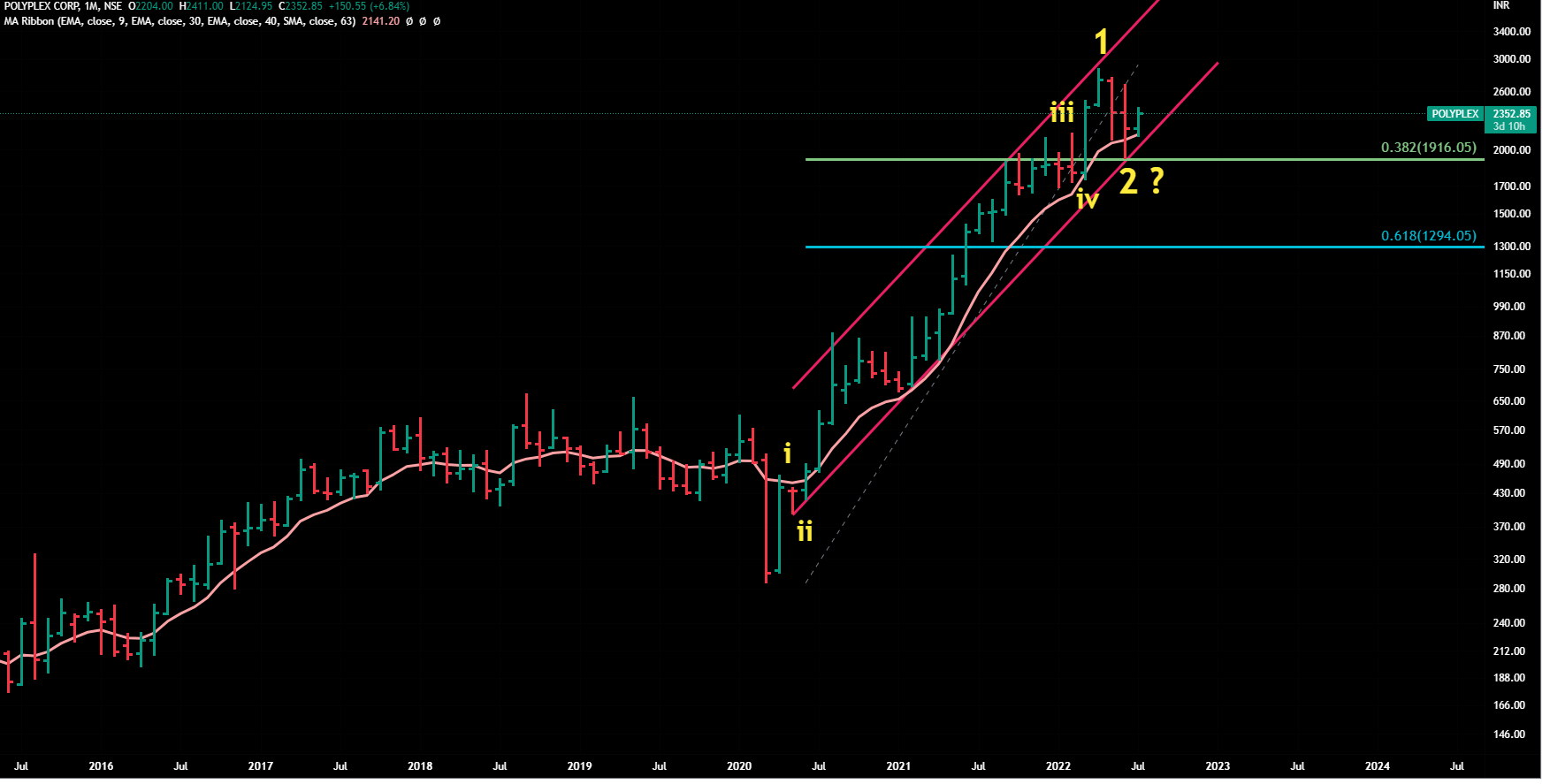

PolyPlex – Quick check.

Please keep in consideration that we don’t comment on day-to-day movement of prices – we tend to look for mid-to-long term trends .

Monthly Chart

It is a beautiful chart – moving in a channel from May 2020 – did not break the channel even in recent correction. Also it is moving above 9 months moving average (pink curve) , came below it in June but did not close below that and also took the channel support at the same time and bounced back.

Other point to note here is that it corrected upto 38 % of FIB level ( of the rise from Covid lows to ATH).This is also a good sign. In these type bear markets, many a times stocks tend to correct upto 50 -78 % levels . If the stock corrected upto 38% level only, that means it is in strong hands ( big money)

Weekly Chart

On weekly, it is taking a support at 40 week moving average (green curve)-never closed below it since the days of COVID lows.

What can happen next ?

Stock became more than 10 X from covid-low levels. To us, it seems to be in time-correction as of now ( it seems price correction won’t be much) , can move in a range between 2000 to 2500 for next few months.

Can it go up ?

Well it depends upon liquidity in the market and overall sentiments .For moving up, it should first trade and close above 61.8% & 78 % level of retracement of current decline ( 2530, 2700 respectively as shown on weekly chart) and then it should cross and close above recent ATH for few weeks.

Can it go down ?

Anything can happen in the market !

If we were at your place, we would track it weekly and monthly. We would draw a channel as well as would use weekly and monthly moving averages as pointed out in the charts.

On every weekend – we would check that it does not close below 40 week moving average for more than 2 weeks, and it does not close belwo the channel.

On every month-end – we would check that it does not close below 9 month moving avergae for more than a month and does not break the channel.

If we were holding this stock from lower level, we would keep it holding it for long term as overall structure looks good. And if we were not holding this stock, we would try to buy when it again comes close to lower end of the channel and track it closely before adding more or exiting.

Disclaimer : Charts are for study purpose only. Opinions are personal- can go very wrong. No suggestions , no recommendations.

When Not To Buy (26-07-2022)

On valuation I’ve seen in my 2 years journey that you make money when the valuation is so cheap that you don’t need to do too much hardwork on valuation. And probability of not making money increases when doing valuation becomes very difficult.

Scenario 1: I bought a NBFC company named CSL Finance Ltd in February 2021 with price being lower than the book value after substracting all the gnpas( which was very low). The promoter was buying from open market. The mgmt managed the NPA to be stable throughout the covid. The adjusted PB ratio was 0.65. It was a no brainer buy at that price and it became a 3 bagger. Didn’t fall at recent sell off at all. Still the company is available at 1.2 PB ratio but now the valuation is little bit hazy. I mean it’s no longer a no brainer buy.

Scenario 2: I bought Prince pipe after it became a multibagger. The PE ratio was 36 but the earning growth was also superb. It was a 25% grower company at 36 PE so I thought even if it grows by 20% I’ll make money because the ROE ROCE was good. After I bought next 2 qtrs results were also good. But then the crude price shot up margins reduced and the stock price is still consolidating and now in the lower range. Though the sector has tail winds. But I’ve lost in terms of opportunity cost. I could have invested now. Because the valuation is much better now. 15% grower at 22 PE with structural tail winds. But will I buy it? No there are much better opportunities which represent no brainer buys.

Scenario 3: Krsnaa diagonistics, a moated player+good management+ Huge runaway for growth. Excellent growth in last 3-4 years. The stock corrected by 50% because everyone thinks increasing competition in Diagonistics sector js going to hurt the existing players. it’s true for dr lal path labs and other like them. but krsnaa completely operates in different field. So here we have a company which can easily double the earnings in next 2-3 years due to huge operating leverage. So it’s a no brainer buy at this valuation.