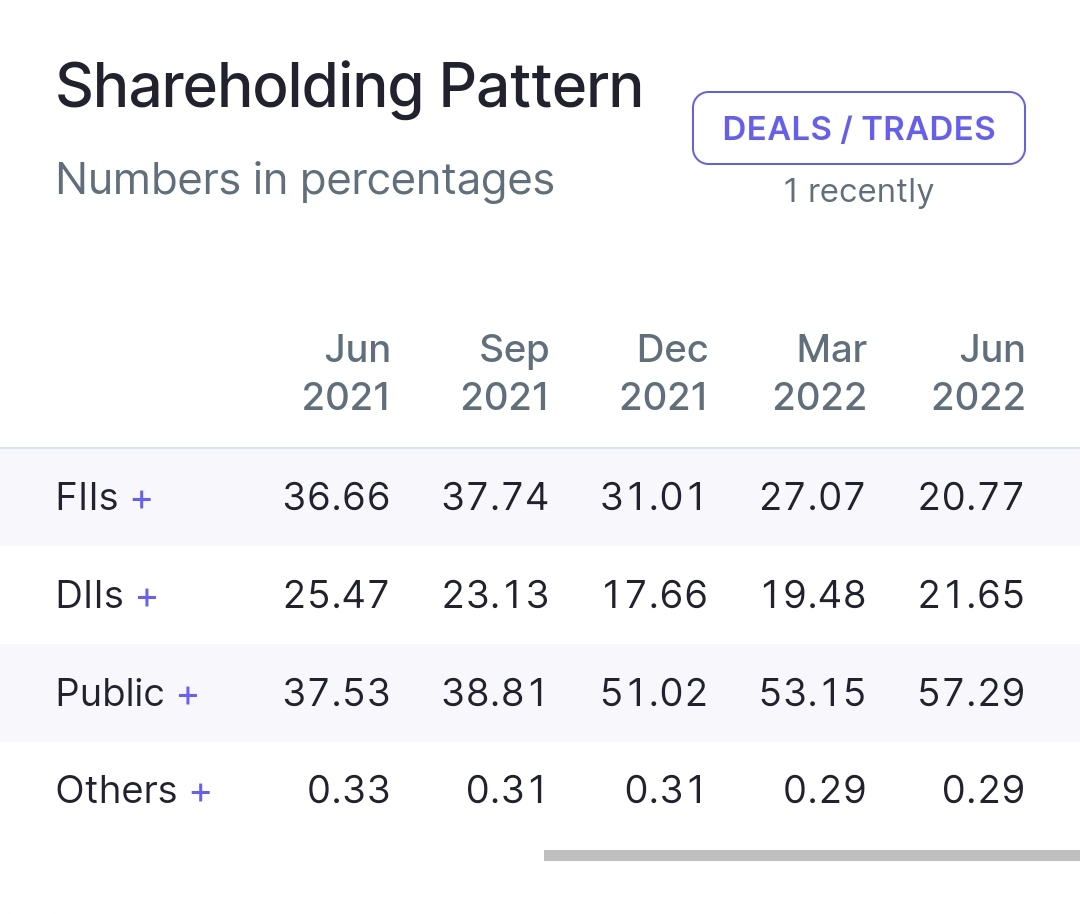

SHP of IEX. There is this pattern. After a good company becomes multibagger and valuations become too rich then institutions start selling. Then with each fall in the name of buy on dip, long term investing etc etc retail share holders buy it. I think the way to buy these businesses is either spot them before the rally starts or buy them when they are cheap enough that one can easily do the valuation. If valuation is very difficult then it’s still overvalued.