Are Roller Coasters Actually Safe? – YouTube importance of safety in the amusement park industry

Posts tagged Value Pickr

Manjunath.c.a’s (CAMS) PORTFOLIO (25-07-2022)

I think before replacing HCL with TATA Elxsi, why you chose HCL in the first place. ER&D is also available in HCL alongwith traditional Service business…So its a more diversified business in my view.

Yes bank (25-07-2022)

Hi Lotus,

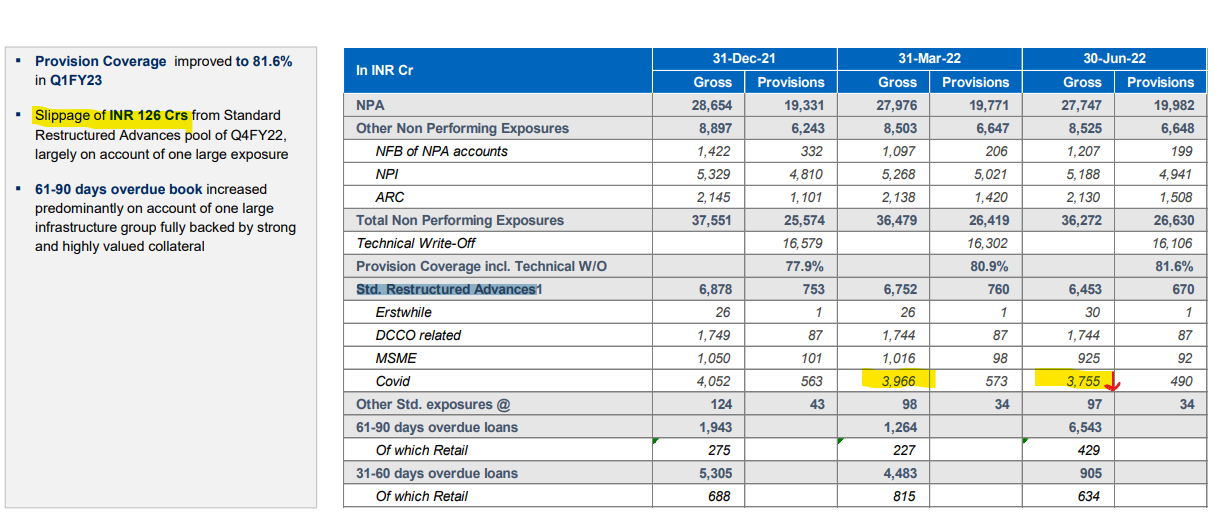

The amount is 126cr from COVID Std. Restructured Advances. I don’t know the name but the amount is clear.

Secondly their 61-90 days overdue bucket has gone up substantially. Bank says it is largely because of 1 infrastructure group backed by high value asset and they are very confident that this wont become NPA.

The results are not good but we have to understand to what extent they are not good. What are the reasons for QoQ underperformance . Are they temporary or permanent . We have to see how other banks have performed QoQ. Just seeing few numbers QoQ and concluding that they are extremely bad is not a correct approach according to me.

I am going through 4 to 5 more banks result. Going through yes bank in detail. I have already see 2 to 3 very important points. Will be posting all details in a few days with the guidance of this year. I would also me mentioning weather 0.75% ROA is achievable this year or not.

@myfirstmillions in con call they were mentioning 800cr of NPA from carnival cinema. I posted the article as well. This NPA was already provisioned last year.

Yes bank (25-07-2022)

It was mentioned in the con-call, i think 138Cr impact. It was NPA in last financial year itself.

Indian Energy Exchange (IEX) (25-07-2022)

Does anyone know where we are in regards to these decisions.

- Market Coupling – Has this happened? If no, then whats the plan/inclination of govt regarding this.

- MBED – Phase 1 was supposed to be live in Apr 22 right? This was a politically and technically difficult move, hence has this been implemented? What the plan regarding this by the govt.

Sigachi Industries Limited (25-07-2022)

Good results. Q1 profit jumps 42.5% YoY to Rs 12.82 crore on strong revenue. The company reported 42.5% year-on-year growth in consolidated profit at Rs 12.82 crore for the quarter ended June 2022, driven by revenue and other income. Revenue grew by 42.5% to Rs 78.31 crore during the same period.

Mahanagar Gas Ltd – a natural monopoly (25-07-2022)

A customer review of MGL

Disclosure: Not invested.

Investing Basics – Feel free to ask the most basic questions (25-07-2022)

i recently came accross this VIP (value averaging investment plan) vs SIP article, however could not find any funds offering this type of investment product. I have contacted my HDFC Securities relation manager, no feedback recieved so far…

if any seasoned investor here is using this method instead of SIP please let me know how to go about this?

Hitesh portfolio (25-07-2022)

Hitesh Bhai,

You have on most of the occasions said that once the sector fancy is over, its better to look at stocks in a different sector which does show interest, than look at same sector.

If we take recent past, specialty chemicals had a great run. stocks which were 1-2 times sales went upto 10 times. Then the pharma sector. Now if we see again, some picks of chemicals sector viz., Gujarat Fluorochem, SRF, Navin Flourine seem to be coming back to fancy on back of good to solid results. How cautious you are in betting these kind of outliers which belong to sector which had its good time.