This is because as gold prices increases, obviously the amount of loan they can disburse also increases.

Posts tagged Value Pickr

Himachal Futuristic communication (24-07-2022)

I think this is negative for HFCL as it imports core of optical fiber.

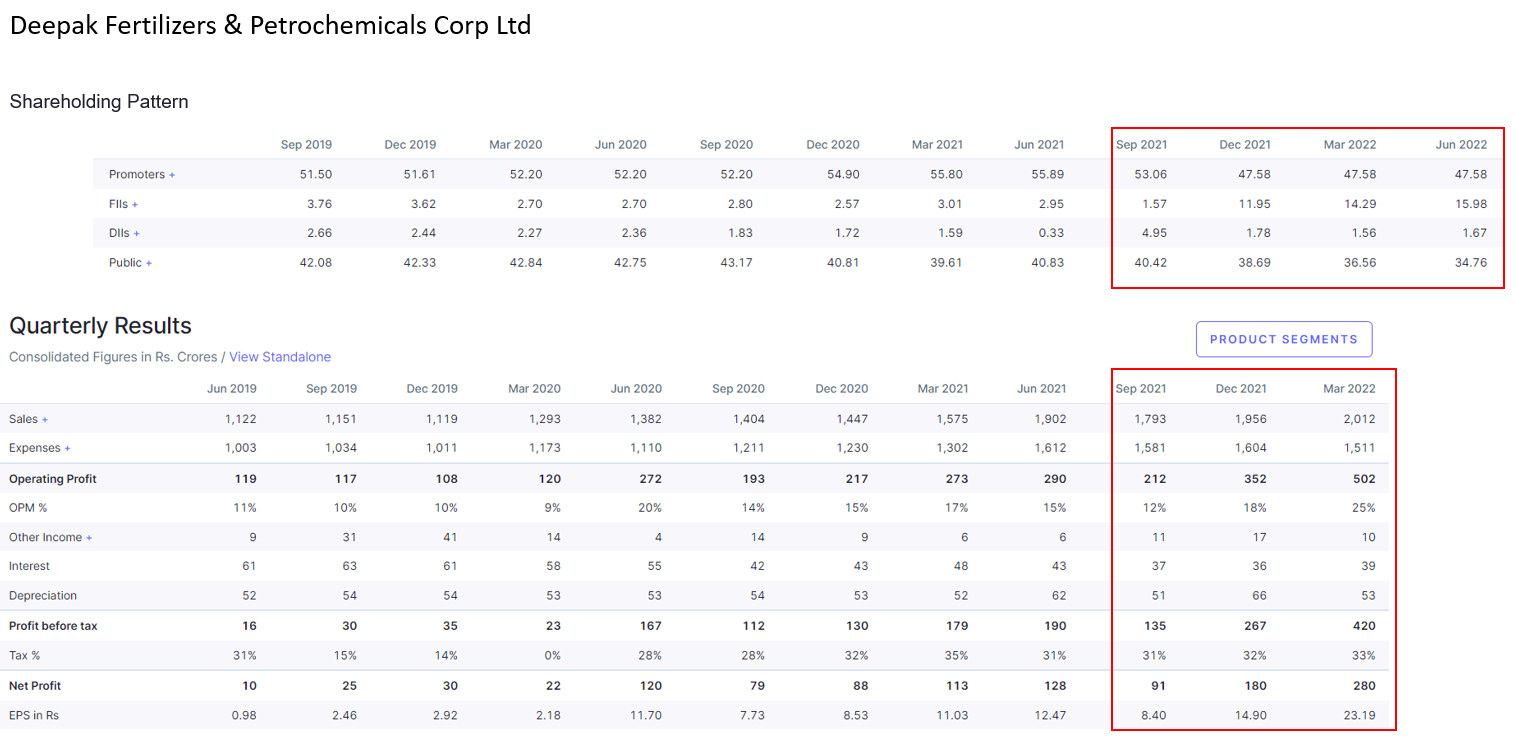

Deepak Fertilizers and Petrochemicals (24-07-2022)

Deepak Fertilizers seen a significant uptick in FII holdings in last one year or so, which is against the general trend. Apart from this Net profit also significantly improved in recent quarters.

Stock recently broke out of 5 years high (~450) and currently trading near ATH.

Data: Screener.in

Disc: I am invested.

IZMO- bet on new technologies in Auto retail & defence (24-07-2022)

Directors of Hughes Precision Manufacturing Private Limited are Sanjay Soni, Jay Prakash Susheel Kumar Saraff, Ved Prakash Soni and Susheel Kumar Govindram Saraff.

Promoters of Izmo, Sanjay Soni & family.

Smart Contract Platforms Thread — Web3 Wars (24-07-2022)

And just like that Crypto markets have started rallying again as Crude Oil prices have moderated and Ethereum’s transition to Proof of Stake is getting closer.

At the Ethereum Community Conference in France Thursday, Vitalik shared his vision for future developments well beyond the network’s move to proof of stake. After the merge, which is very close “the only thing left to do is do a merge on Ropsten [test network],” Ethereum will then undergo further upgrades which he calls the “surge,” “verge,” “purge,” and “splurge,”

https://www.youtube.com/embed/kGjFTzRTH3Q

The surge refers to the addition of Ethereum sharding, which will help scale the base layer.

The verge will implement “Verkle trees” (a type of mathematical proof) and “stateless clients.” These technical upgrades will allow users to become network validators without having to store extensive amounts of data on their machines.

The purge: trying to actually cut down the amount of space you have to have on your hard drive, trying to simplify the Ethereum protocol over time and not requiring nodes to store history.

The splurge will include all the other fun stuff.

Deepak Fertilisers and Petrochemicals Stock Story (24-07-2022)

Deepak Fertilisers and Petrochemicals

BACKGROUND

Deepak Fertilisers And Petrochemicals Corporation Limited (DFPCL) is one of the largest manufacturers of chemicals in India. It manufactures Technical Ammonium Nitrate (mining chemicals), Industrial Chemicals and Crop Nutrition. The products of the company have uses in Explosives, Mining, Infrastructure and Healthcare. The company was set up in 1979.

MAIN PRODUCTS/SEGMENTS

MAIN MARKETS/CUSTOMERS

CURRENT MARKET/INDUSTRY TRENDS

BULLISH VIEWPOINTS

• X

• Y

• Z

• A

• B

• C

BEARISH VIEWPOINTS

• X

• Y

• Z

• A

• B

• C

INTERESTING VIEWPOINTS

• X

• Y

• Z

• A

• B

• C

BARRIERS TO ENTRY

• X

• Y

• Z

• A

• B

• C

BUSINESS MODEL

VALUATION MODEL

CORPORATE GOVERNANCE SCAN

RED FLAGS/FORENSIC SCAN

DISCLOSURE(s)

Muthoot Finance (24-07-2022)

I ran a regression of Muthoot Finance’s Revenues to the Gold Prices (per g). I took the quarterly revenues and gold prices from June 2011 to March 2022. The R-Squared is 88.15% which means gold prices do affect Muthoot Finance’s Revenues. I came up with a conclusion that every rupee increase in Gold Price (per gram) will result in Rs. 7.05 increase in Muthoot Finance’s Revenues. Look at the numbers and relationship chart below:

Hinduja Global Solutions (24-07-2022)

What do you think is the fair value of this stock?Most of the cash may be utilized to make acquisitions and hence to assess their value should be difficult.