Thankyou for the information. I was suspecting that their debt could have been the reason, but this info clears things up.

To other readers who may be curios with regards to the date of conviction, it is actually December 2010.

Posts tagged Value Pickr

UFlex Ltd – Short term opportunity? (18-12-2015)

Gulshan Polyols(GPL) – Business by FMCG and Valuation by Commodity (18-12-2015)

@kkvinvestor

Looks like company has recently expanded its Calcium Carbonate or PCC

- On site PCC & WGCC plants in Bangladesh commenced commercial operations.

- On-site project with Orient Paper Mill, MP has started & production is expected by 31-Dec-15

(source – q2fy16 press release)

therefore it will reasonable to conclude that we may see PCC growth in this or next quarter.

Hindistan Media Ventures Limted (HMVL): A mispriced bet in newspaper business (18-12-2015)

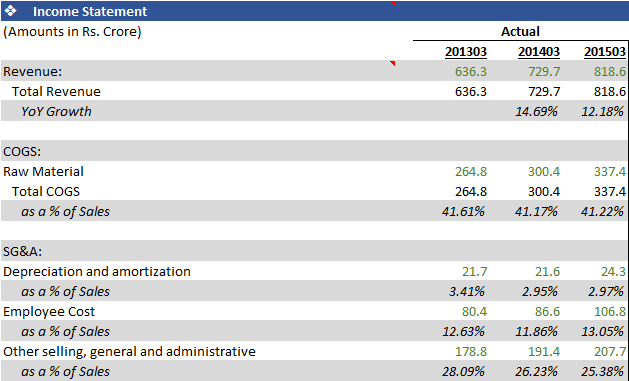

After doing some more research I would like to add the expansion in margins has been account of both pricing power (which flows to the bottom line) and their fixed cots being spread over a larger volume. The second factor illustrates the operating leverage that the business enjoys.

As you can see from the table below, raw material cost as a % of sales has declined marginally. But SG&A (advertising, repairs, rent, etc.) and depreciation have declined as well. Infact they have declined more significantly.

I would also like to add that DB does actually have a presence in Uttarkhand. They still don’t have a presence in UP however, which I still find very puzzling.

Companies affected by Chennai Flood (18-12-2015)

In my first post I have mentioned that I couldn’t find any data or reports with regards to the actual data.

When I googled for news… I came up with this

Introduction & Portfolio (18-12-2015)

Unitech & Lanco are risky bets. Expecting turn around in Q3, Q4. Also Unitech is 2nd biggest realtor available at 20% of book value. Its only 1700 crore. Imagine you can buy out a formidable real estate company for less than 2000 crores…..I see this as a discount. however last 30 days no great movement, rather lost some money in both.

I didnot plan for diversification Cap wise or Industry wise. I am picking stocks basis MOS & IV.

I am tracking companies, where QoQ losses are reducing- so that at some point they cross over to profit. May be stock will pick up from that inflection point. Let me know if this method is wise or has any + correlation with price movements

UFlex Ltd – Short term opportunity? (18-12-2015)

Hi Anand,

The reason for Uflex’s low proce is due to past conviction of its CMD…Ashok Chaturvedi..see extract beow

Chaturvedi and Neera Yadav, the former chief secretary of Uttar Pradesh were on Tuesday sentenced to four year in prison by a CBI court in a 1994-95 Noida land scam case. Following the judgment, the company’s shares crashed 20% on the Bombay Stock Exchange. In a communication to BSE, Uflex stressed that the judgment had no financial implication for the company. Chaturvedi, it said, had been found guilty in his ”individual capacity” in a case relating to allotment of land for the company’s employees. Uflex added that the land was not used by the company and that Chaturvedi was taking ”appropriate legal steps” in the matter.

Known to be a charmer in Delhi’s power circles, Chaturvedi is no stranger to controversy. In 2001, he was arrested by the CBI under the Prevention of Corruption Act for allegedly bribing a top excise department official. Former cabinet secretary Prabhat Kumar was forced to resign as Jharkhand Governor after reports that Chaturvedi had paid for his private parties appeared in the media.

Companies affected by Chennai Flood (18-12-2015)

Can you tell me the source of your data and do you have exact numbers around this?

Introduction & Portfolio (18-12-2015)

Anupam, portfolio good good, would be nice to know your buying price with current return to gauge the performance

Thanks

Companies affected by Chennai Flood (18-12-2015)

Sorry if I wasn’t clear.

A lot of vehicles have been destroyed or impaired by the floods, also lots of home applicances like refrigerator, grinder, motor pumps etc were also either impaired or washed away by the floods.

Money will have to be spent by the consumers in replacing them or repairing them as they are essential commodities.

This will result in additional sales for companies supplying those appliances/auto parts.

Lycos internet – way to digitalization (18-12-2015)

The following kind of response doesn’t give any confidence on the promoters (taken from their last conf call transcript). This made me not to look at this script ever again !!

Individual Investor: …………… My first question is regarding the increased number of pledging of shares as per the latest quarterly results.

Suresh Reddy: This is not related to the company, this is what….these are things that are done outside by shareholding promoters of the company and it has nothing to do with the company.

What kind of response is this ?