posted pic below on the holding of a few funds, lets keep checking as this months they are expected to pick a lot more and new funds ,ike HSBC and Canara are also picking it

Posts tagged Value Pickr

Lycos internet – way to digitalization (18-12-2015)

I am seeing a few things that un-settle me when it comes to their books and management:

-

There is a new entry under the head intangibles under development in 2014. The head had relatively small amount allotted to it in 2014 … around 19 cr. In 2015 this entry has been deleted and a new entry created under same head. This time this entry is for 164 cr. Any idea what this head is and why was it created in 2014? In absence of clarity on this new entries like these should be considered a red flag. It probably relates to point 3 I am mentioning regarding employee costs being capitalized.

-

CFO changed in FY 2015 . Auditor remuneration going up from 14L to 20L and as per the concall they mentioned that they are going to change the auditor. Isn’t this just too many changes too soon? Is there a reason mentioned in previous con calls?

-

They are capitalizing employee costs and consultant expenses related to research. These should not be capitalized. They talk about listing in U.S., but as per their accounting standard and my limited knowledge .. they are not allowed to capitalize these expenses. In such a scenario their earnings are over-stated. This I guess to relates to point 1 I mentioned.

-

Mr. Suresh Kumar Reddy receives zero remuneration. This is a bit odd considering this company doesn’t even pay dividend.

-

To some extent their business model does explain their high accounts receivable, but there should be a comparative business elsewhere (if not in India), any idea on how I can compare their levels of receivable to a similar company in another country.

Thanks

MPS Ltd (18-12-2015)

Some key observations from my side :

Performance of Acquired Companies :

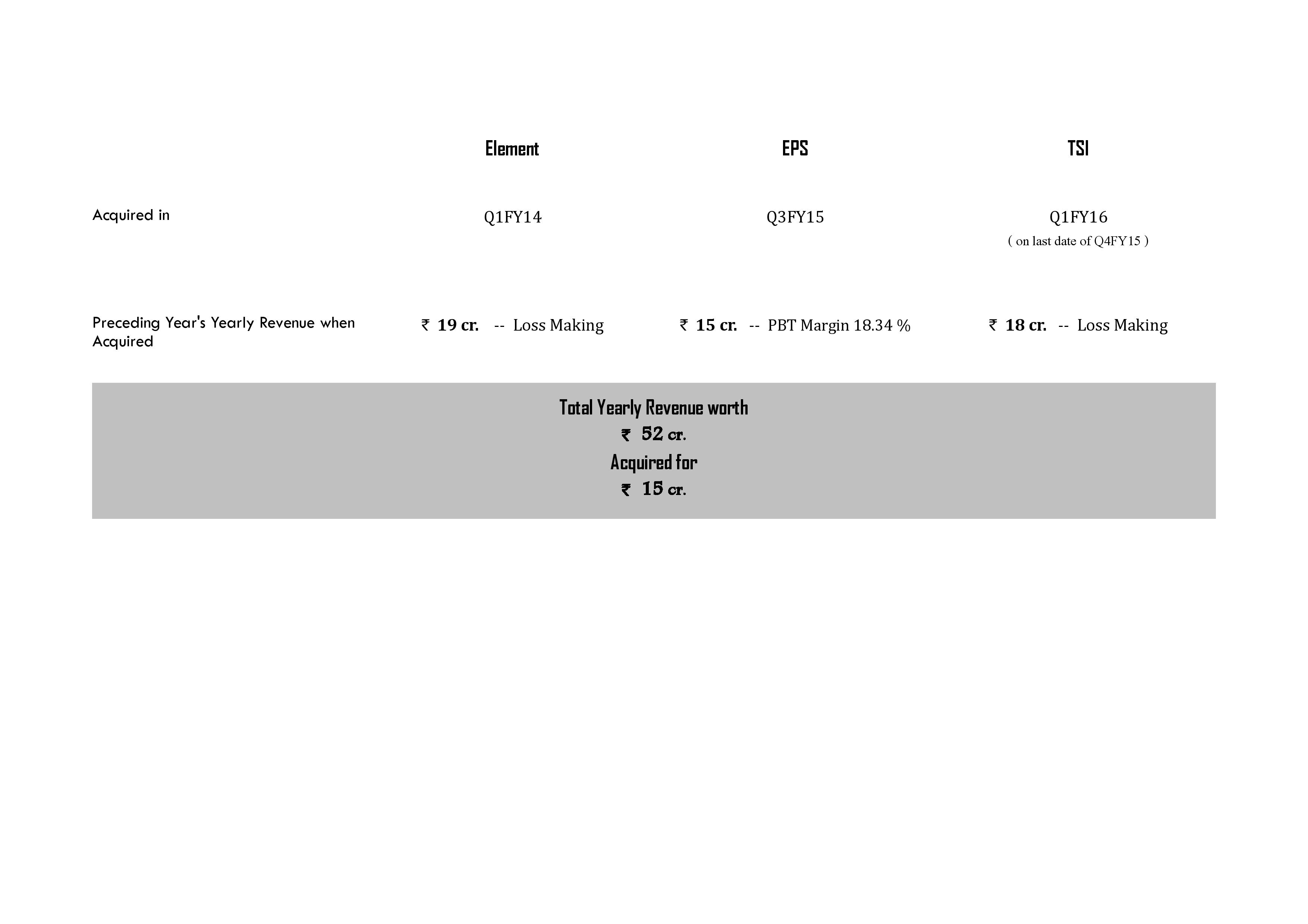

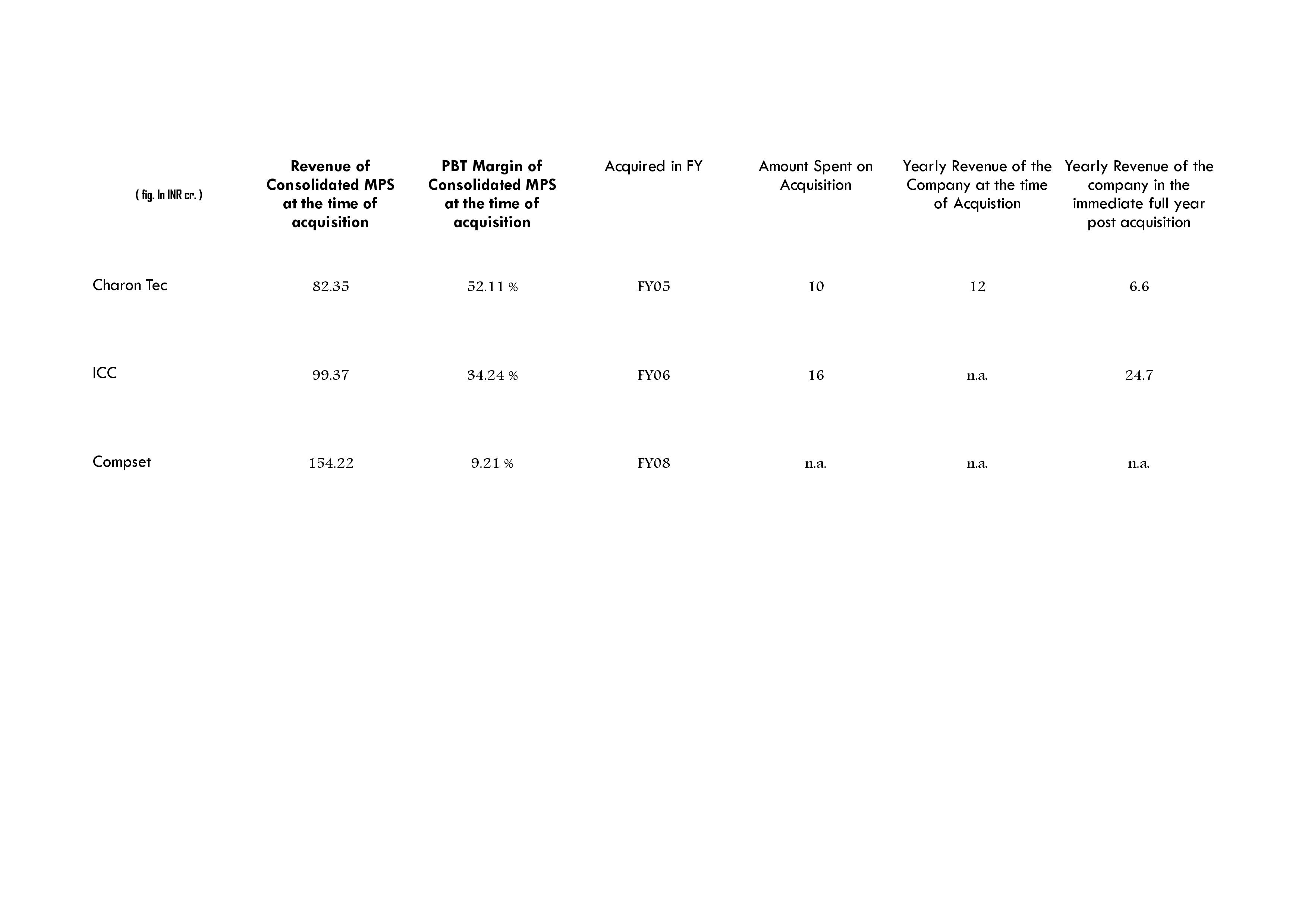

Let’s first have a look at key financials of the companies before they were acquired by MPS (under Mr. Arora) and the amount spent on acquisitions :

— By spending just INR 15 cr., a yearly revenue of INR 52 cr. were acquired which prima-facie seems a great deal. However, key thing to note is each of the company was almost on verge of extinction and so Mr. Arora extracted maximum bargain out of them.

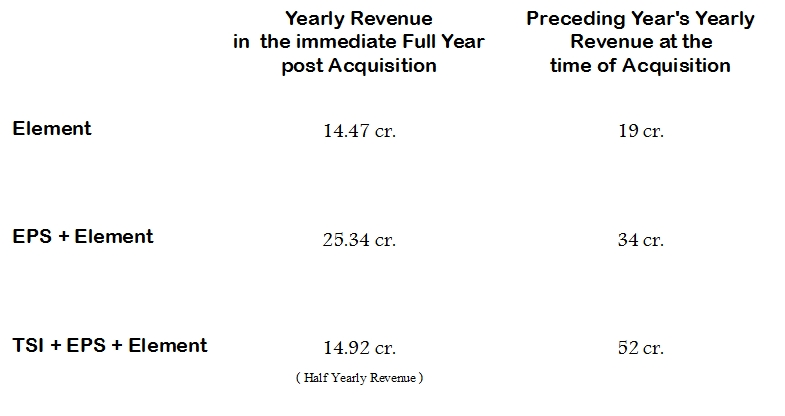

— Key lies in performance after acquisition of such distressed assets and it is given below :

— Since TSI is only a recent acquisition and has not passed even first full year, so we need to wait for couple of more quarters for its performance to show up.

–Regarding Element & EPS, although post acquisition topline has suffered but that is understandable as Element was in distress at the time of acquisition whereas EPS was more of a steady business which promoter wanted to sell out. There would always be overlap as also phasing out of some contracts once ownership changes hands and so a cut of 25 % on topline is perfectly fine and reasonable.

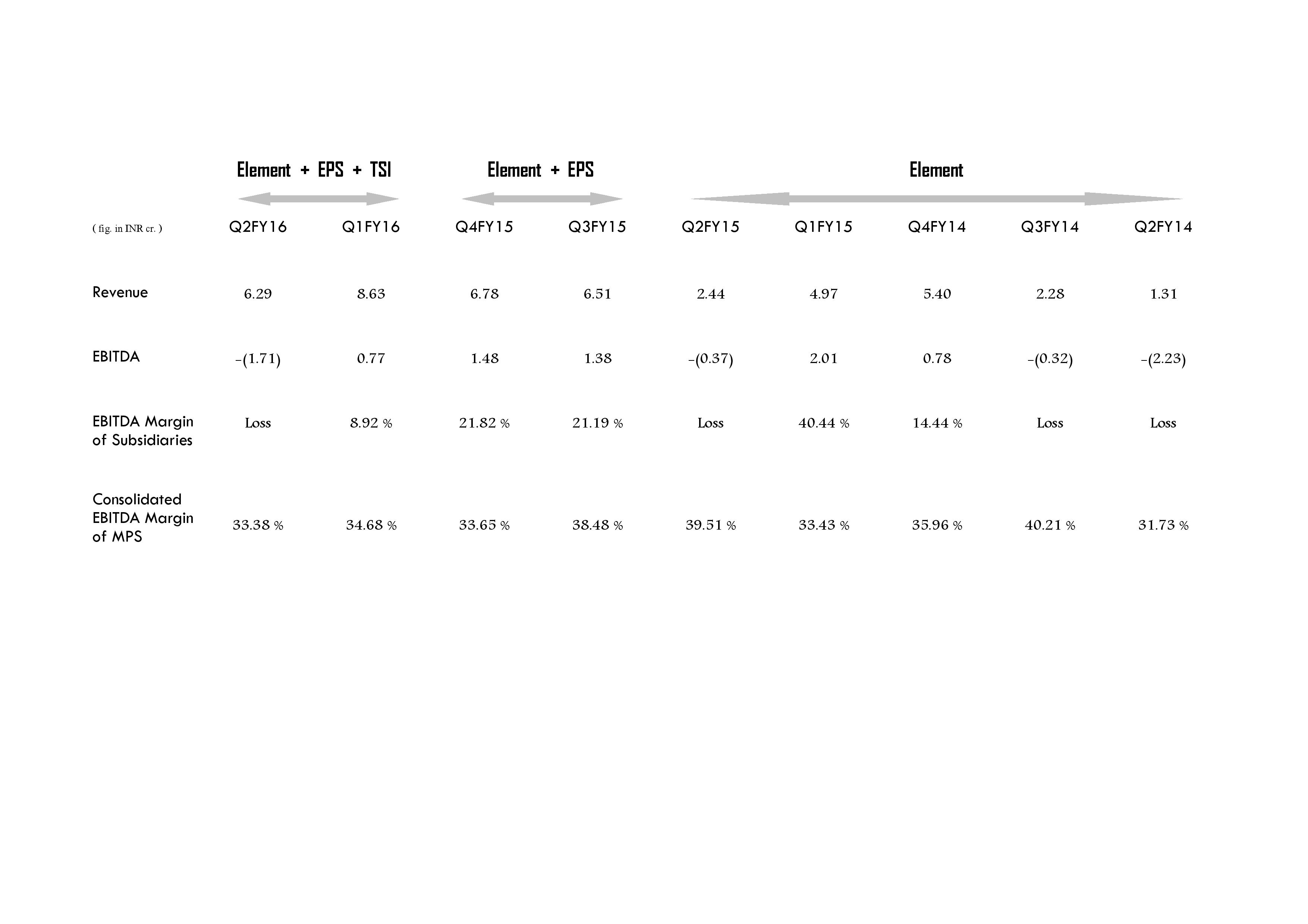

–Key is bottomline which is the crucial aspect as it is this factor which failed MPS under its previous owner. MPS under Macmillan never recovered from the huge losses it acquired because of acquisitions and that led to the debacle of an otherwise healthy robust cash generating business (Yes !! It will be interesting to note that MPS under Macmillan also was operating at 40 % + margins before embarking on inorganic journey). We will be able to assess this aspect from quarterly performance of subsidiaries as have done below :

–From above it is apparent that Element had more or less stabilised and was, and is, operating at almost breakeven level (we can’t take quarterly margin spikes into consideration and need to look at the whole picture).

–EPS seemed a good acquisition as it provided much needed support to bottomline because of 18 % PBT margin at which it was already operating before the acquisition.

–From the first two quarters performance post TSI acquisition, it clearly seems a drag on the margins (even if we exclude one time charge of 1.60 cr. in Q2FY16). However, its too early to draw any conclusion as only two quarters have passed and such distressed assets take time to recover and breakeven.

–Some things are clear from the acquisitions done so far :

these acquisitions were only for plugging gaps in the offerings of MPS

these acquisitions were only for plugging gaps in the offerings of MPS

we should not expect significant bottomline improvement in any acquired company post its acquisition ; atbest a loss-making acquisition could turn breakeven or low double digit margin as is evident from the nine quarter performance of oldest acquisition Element.

TSI also might go the Element way and operate at breakeven few quarters down the line. So, in medium term atbest we can expect a 18-21 % EBITDA margin (because of strong EPS margins) at subsidiary level from the acquisitions done so far.

acquisitions have failed to grow significantly in topline (w.r.t. their topline before acquisition) under MPS and even they have not been instrumental in aiding topline growth of consolidated entity (except simple addition) as is evident from muted standalone growth even post acquisitions.

It is important to understand here that this analysis is only based on past nine quarter performance of Element, past four quarter performance of EPS and past two quarter performance of TSI. Distressed assets even under best management take atleast couple of years to show any meaningful performance.

Still, there are two main reasons of drawing this analysis at early stage (and also keep revisiting our analysis every quarter) :

Mr. Arora is on record saying that acquisitions are crucial for future of MPS and success majorly hinges on right inorganic moves. This is the reason why he has dedicated himself completely to this goal.

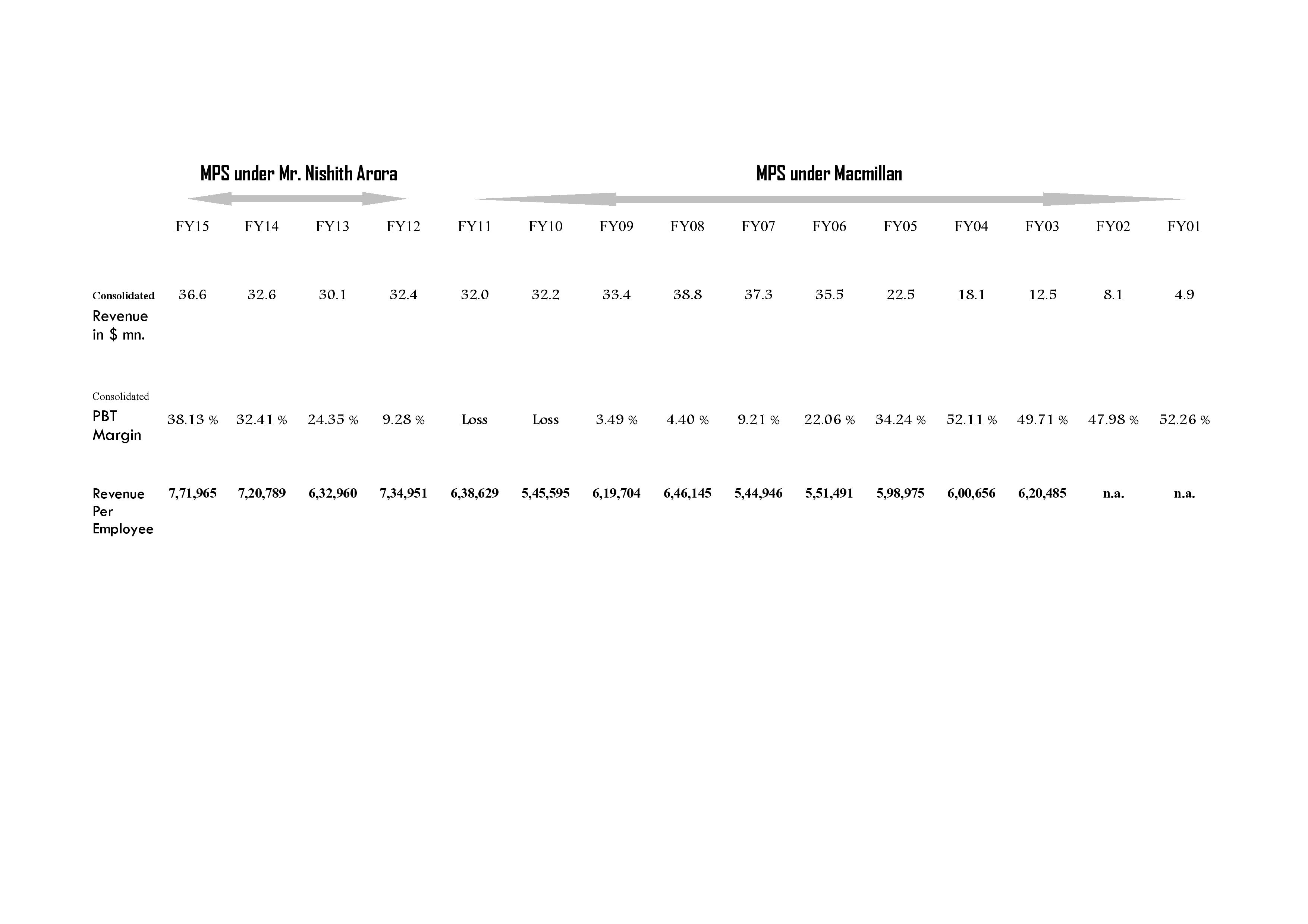

MPS under its previous owner failed miserably in inorganic moves. If we draw a comparison here, MPS under Mr. Arora seems to be at a similar stage where MPS under Macmillan was in FY04 post which inorganic journey was started by then management to double the topline in three years. Let’s have a brief look here :

MPS under Macmillan & MPS under Mr. Arora

— It is worthwhile to note here that in above comparison, we have taken into consideration the financials of only business related to current MPS and other businesses like book publishing business (which were part of Macmillan till FY08) are kept out of our analysis.

— Revenue is compared in USD mn. to enable fair assessment excluding currency movement.

— Standalone Revenue of MPS in FY14 & FY15 is 31.1 and 33.2 mn. USD respectively.

— Company was operating at an average 50 % PBT margin till FY04 post which starting FY05 it embarked on inorganic route which saw its margin dwindling to 4.40 % in FY08 when last acquisition was made, finally pushing the company into losses and eventual sell-off to Mr. Arora.

— Let’s have a look at acquisition history of MPS (current business) under Macmillan :

— Within three years of initiating inorganic journey, company’s topline almost doubled from 82 cr. to 154 cr. whereas margins saw a decline from 52.11 % to 9.21 %. Part of it was because management at that time made big loss-making acquisitions with a hope of turning them around which never happened. Part of the current acquisition delay can be explained by this background which Mr. Arora must be very well aware of.

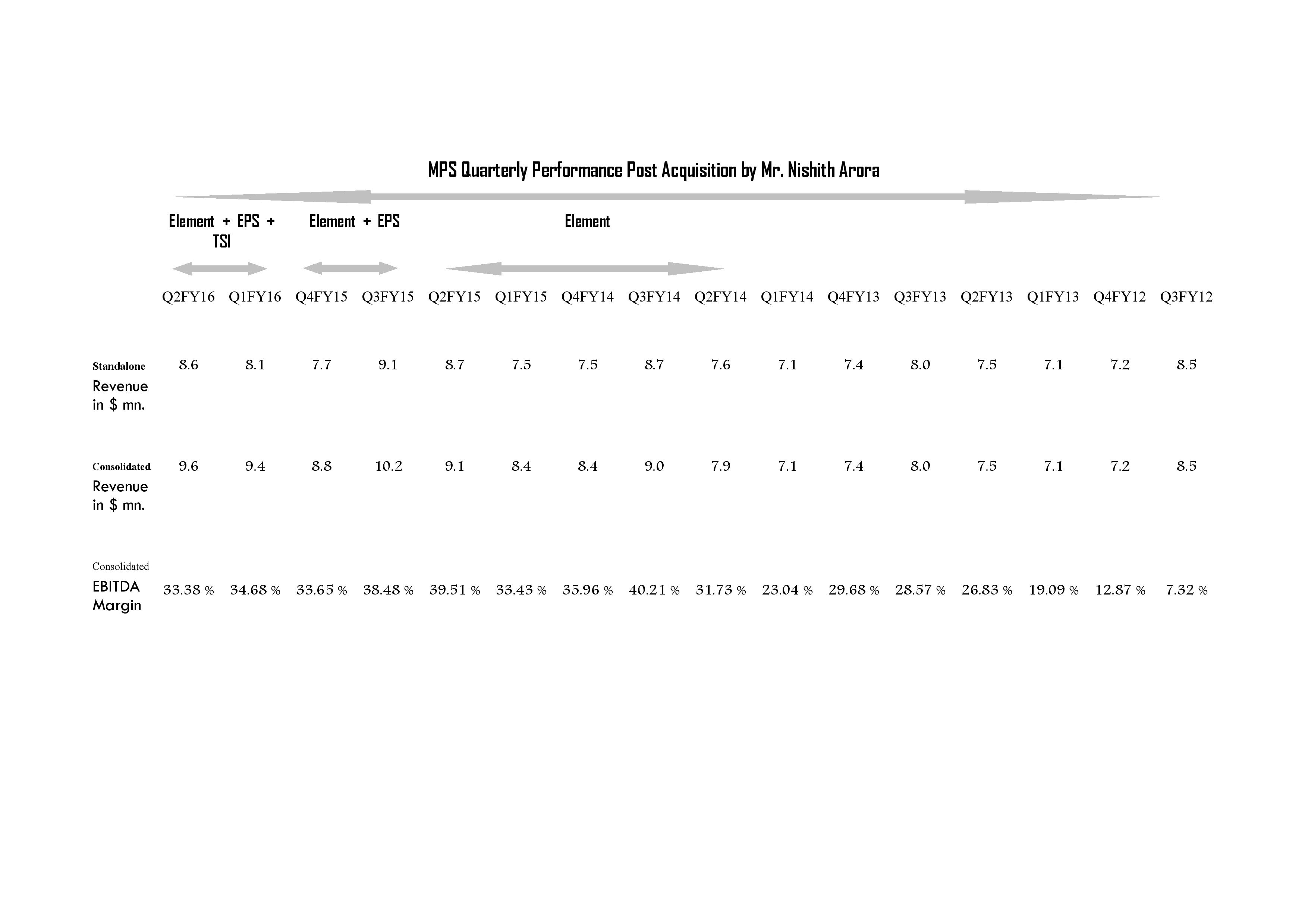

Quarterly Performance of MPS under Mr. Arora

— Having done all these, it is also worthwhile to look at quarterly performance of MPS under Mr. Arora :

— We have done assessment in USD mn. only to arrive at fair conclusion regarding actual growth in business excluding currency movement.

— On standalone basis, topline is almost at the same level as Macmillan era. It is the acquisitions which have provided simple addition to the topline on consolidated basis.

— Key thing to look at is margin performance wherein from single digit EBITDA margin, Mr. Arora has gradually scaled up to 35 % + margins which is commendable. Macmillan was able to operate at this margin level (infact slightly more than this level) when its scale was almost half the current scale whereas Mr. Arora has corrected the mistakes and almost regained Macmillan-golden-era’s margins at increased scale.

— It is the sustenance of these margins and therefore robust cash generating ability of this business at this or even increased scale which is appealing. A simple example can be found below :

Dividend Policy

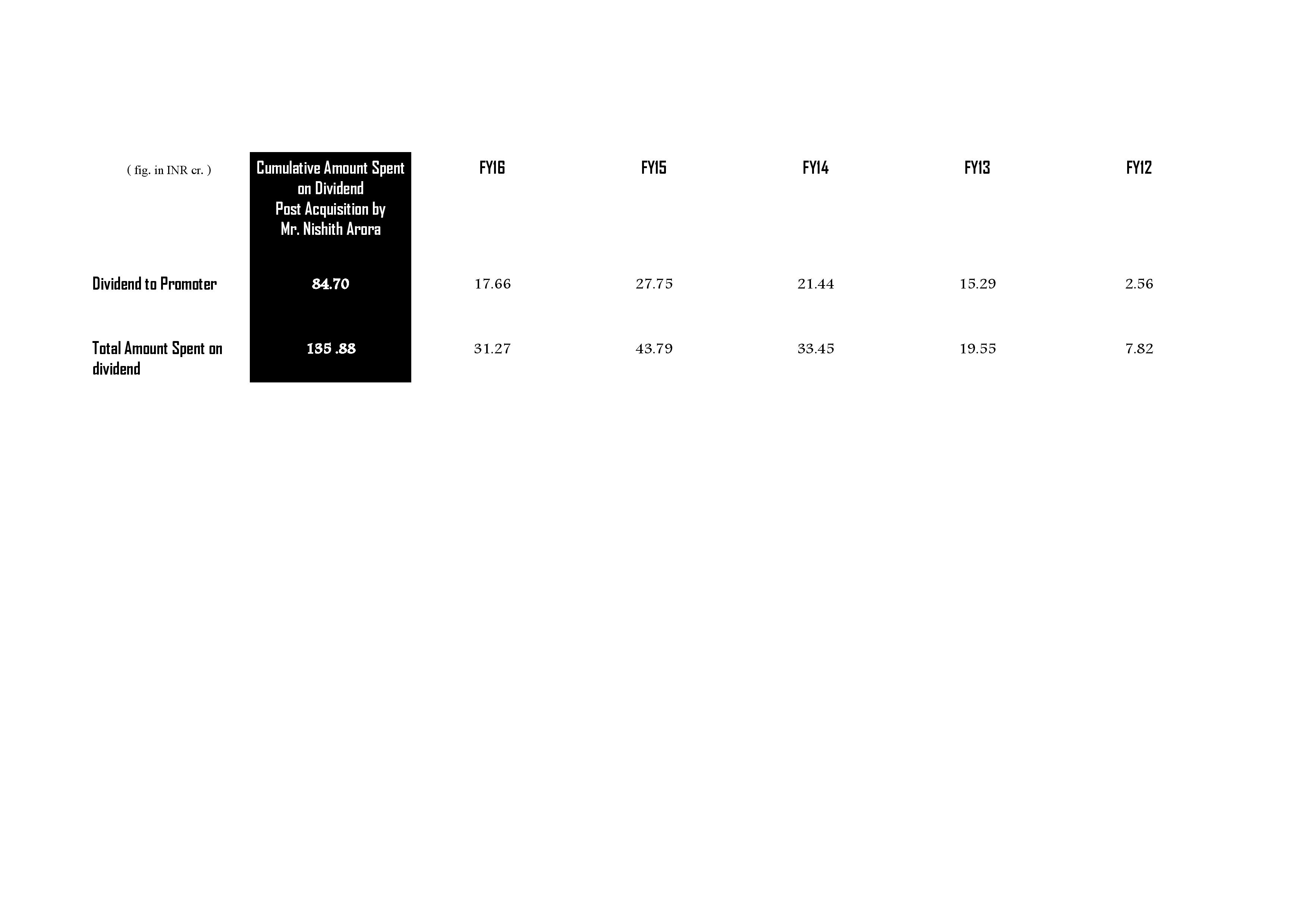

— After Mr. Nishith Arora acquired MPS uptill now, company has spent 135.88 cr. on dividend payment. Out of this 135.88 cr., 84.70 cr. are received by promoters as dividend.

— When we add this amount to the 30 cr. net cash company has as at September’2015 ex-QIP funds, after four years post its acquisition, if company had not paid any dividend, the net cash at its disposal would have been 165 cr..

— Because of generous dividend payment, company had to dilute its equity to the extent of ~10 % and raise 150 cr.. QIP funds. This is the reason why we see serious long term investors in the company like Enam constantly requesting Mr. Arora to have a relook at generous dividend policy.

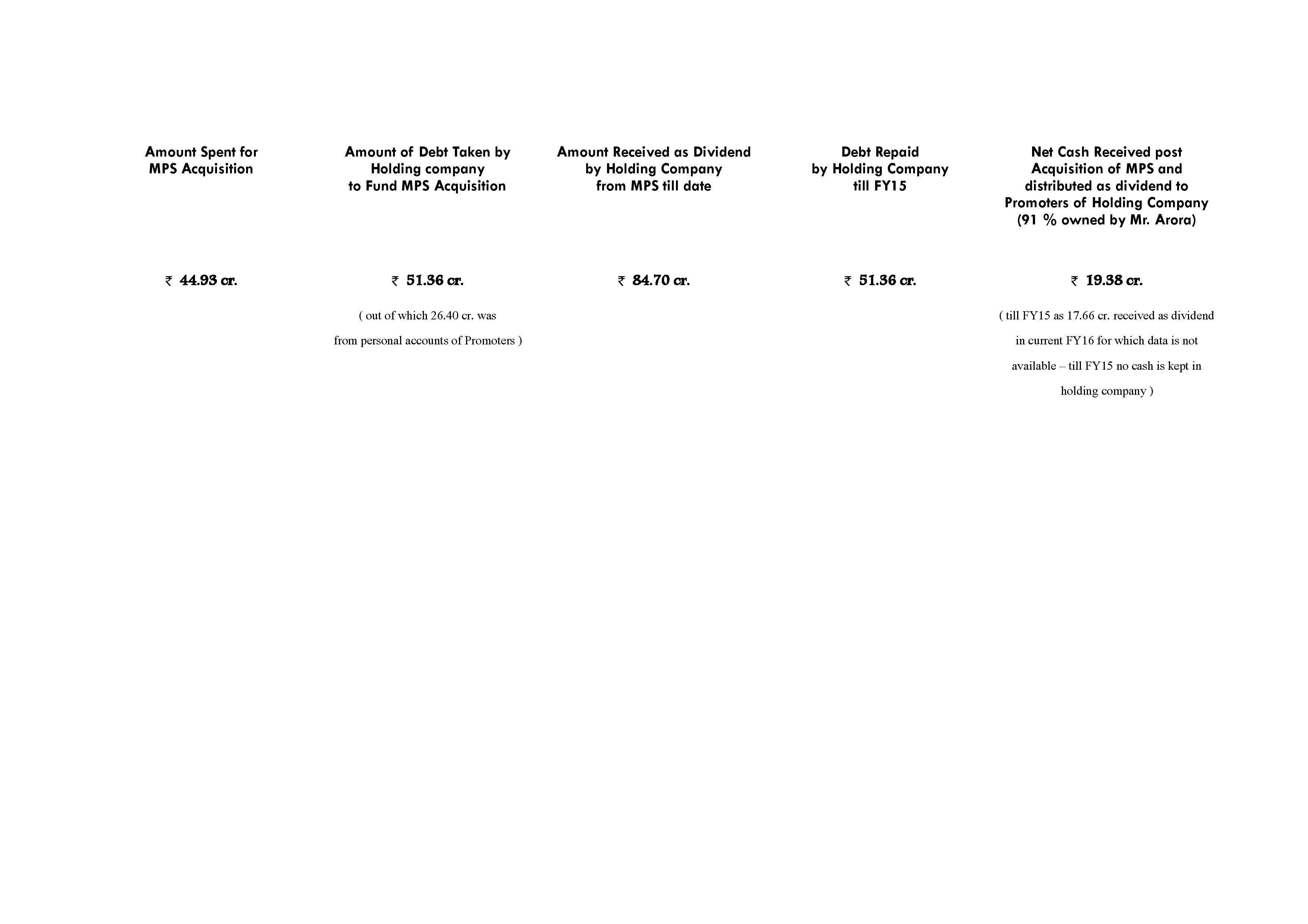

— Part of this approach towards generous dividend payment uptill now can be explained by the need of the promoters to pay back debt they raised at holding company level to acquire MPS :

— Mr. Arora spent ~45 cr. for acquiring MPS for which he raised 51.36 cr. debt at holding company level. Out of this 51.36 cr. debt, 26.40 cr. were lent by Promoter family so in effect external debt was to the tune of ~25 cr..

— Out of the dividends so far received from MPS, the holding company has, till FY15, repaid entire debt and has started returning money to the promoters via dividend payment – in FY15 a dividend of 19.38 cr. was paid to promoters.

— Now, there is nothing wrong in these and seems perfectly reasonable as Mr. Arora took a very big risk by acquiring ailing MPS via his personal money then, and, so it seems fair to compensate him with reasonable return on his investment.

— The key is what lies ahead – in a reply to Enam in the concall, Mr. Arora was quite forthwith in saying that he will be the first person to curtail dividend payment if he feels its in the best interest of business. Now, with entire debt repayment done and being paid back his own money too with reasonable returns, he can afford to have a relook at generous dividend policy. But, much will depend on profile and financials of acquisitions that he will do.

— It is worthwhile to note here that MPS has a history of generous dividend payment under its previous owners, Macmillan, too (although not to the extent Mr. Arora has done). In a similar fashion, before embarking on inorganic journey, MPS in its previous avatar was known for quite a generous dividend payout till FY06-7. In FY05, it initiated its aggressive inorganic journey by acquiring three companies and doubling its topline in just three years (talking about business related to only current MPS and not book publishing business) ; acquisitions backfired and it went into losses and dividend payments were curtailed to reach 0. Again, part of the reason Mr. Arora taking his own time in making acquisition decision could be because of this almost identical background and I am sure he will be extra cautious this time not to repeat the same mistakes again.

Rgds.

Discl. – Invested in MPS. No Trading in last 30 days.

Marico Kaya (MaKE) (18-12-2015)

The company’s foreign subsidiary Kaya Middle East, DMCC, along with its local partner has entered into a share purchase agreement to acquire 75 percent beneficial interest in Iris Medical Centre LLC situated at Abu Dhabi. Iris Medical Centre LLC carries out business of skincare services and operates one clinic in Abu Dhabi. Iris Medical Centre LLC has reported revenue of AED 2.24 million as per its last financial statement for half year ended on September 30, 2015. Kaya had reported consolidated profit of Rs 2.6 crore in Q2 FY16 (Aug-Sept) against Rs 12.6 crore in corresponding quarter last fiscal. The company has added 4 clinics and 35 Kaya skin bar outlets across format in India in Q2 FY16. Overall in India Kaya has 106 clinics and 64 Kaya skin bar outlets and operates 19 clinics in Middle East.

APL Apollo Tubes (18-12-2015)

Why don’t we revisit this stock? Please go through this news article for inspiration

Ajanta Pharma (18-12-2015)

Getting FDA approval alone is not enough but making it profitable is the real test. I think Ajanta Pharma is one right track in getting approval for the drugs which has the potential of profitability rather than just for the sake of approvals.

Emkay taps and tools (18-12-2015)

Sep results have been on track.

http://emkaytapsandtools.com/wp-content/uploads/2015/11/Financial-Results_September-30-2015.pdf

About 40 Rs EPS for 6 months.

Totally ignored company by the markets.

Tasty Bites: A proxy play to India’s QSR industry (18-12-2015)

Today there is volume spurt of 24x coupled with breaching of upper circuit…any news on this stock which led to this??

Last time before open offer announcement there were similar high volume spurts and then finally the news came out.

Disclosure: Tracking but not invested

Spenta International (18-12-2015)

i think what could be added to your assessment is that virat has not grown too much in last 3-4 yrs whereas spenta has…also spenta has a much larger capacity than virat. Last but extremely important is the cash generated ability of spenta which is far superior than that of virat… i had evaluated both stocks, met the management, talked to factory employees and its customers and eventually decided in favor of spenta… infact if you do the last bit virat, does not stand a chance.therefore, I invested in spenta a few quarters back but have booked out fully due to this bse circular of price caps…else my personal fav was spenta…

disc: as of now not invested in either.