This is trading @80-90x FY16 while the promoter seems to be acquiring companies left, right and centre. They have projected only 15% organic growth so acquisitions should continue to justify these valuations. I am still not very convinced about Kellton’s overall strategy. Could anyone explain what causes cost of material as negative? All ISMAC players are trading at astronomical valuations attracting circuit filters. It would be great if someone can share AGM notes.

Posts tagged Value Pickr

US based NRI’s – How do you guys invest in equity now? (18-12-2015)

https://www.valueresearchonline.com/story/h2_storyView.asp?str=29684

Documentation required for US NRIs

To invest on a repatriable basis, the NRI investor must have an NRE or FCNR Bank Account in India

Some AMCs like UTI Mutual Fund now accepts investments from US citizens (NRIs). What is the documentation required? And from which account they accept the funds? NRO or NRE?

You must check with the mutual fund. Typically, individual investors should produce their Proof of identity (Photo PAN card copy or PAN card copy) and Proof of Address (any valid documents listed in section B of the KYC Application Form for Individuals). Apart from the certified true copy of the passport, an NRI investor should also provide a certified true copy of the overseas address and permanent address will also be required. If any of the documents (including attestations/certifications) towards proof of identity or address is in a foreign language, they have to be translated to English for submission. The documents can be attested, by the Consulate office or overseas branches of scheduled commercial banks registered in India.To invest on a repatriable basis, the NRI investor must have an NRE or FCNR Bank Account in India.

Pix transmissions – low profile microcap company (18-12-2015)

There is no margin of safety in the investment. The stock is already trading at PE ratio of 51.

Keerthi Industries (18-12-2015)

Can u please tell about cement capacity of Keerthi Ind ?

Portfolio check up (18-12-2015)

Would help if you share whats your expected returns every year, your risk profile, your buy price and how many years you can hold these stocks.

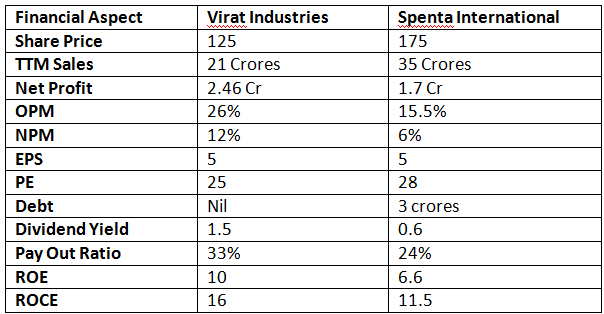

Spenta International (18-12-2015)

Hi,

Here is the comparison between the 2 players.

In comparison between the two clearly Virat Industries is having upper hand.

All the parameters such as Profit Margins or ROE ratios, Debt front, Dividend history Virat industries reports better figures. But In my opinion both are fully priced in at current market price.

Recently both gave nearly 100% returns because of following reason.

Spenta got attention by aceinvestortrader blogger where as Virat got fame by smallcapvaluefind blogger.

References:

Virat : http://www.screener.in/company/530521/

Spenta : http://www.screener.in/company/526161/

Disclosure: I don’t hold any investment in these scrips, i am a safety investor i will never buy stocks of 25+ PE multiples generally.

Introduction & Portfolio (17-12-2015)

Hi Intelligent Investors !

I have recently started investing in stocks. I prefer value investing- try to buy good companies below Intrinsic value. I do comparative valuation, DCF & EVA sometimes  Not always accurate but manage to reach some number in excel. I am thrilled to be part of this group with so many active, vibrant yet sincere minds. I hope to catch up fast on better investing skills.

Not always accurate but manage to reach some number in excel. I am thrilled to be part of this group with so many active, vibrant yet sincere minds. I hope to catch up fast on better investing skills.

Below is my portfolio for your reference. Would be great to have feedback, advice & suggestions on quality, duration & risk factors.

P. I. Industries Ltd. – A Unique Business Model can make it a Great Play on Agri & CSM Space (17-12-2015)

On 11.12.2015 Salil Singhal sold 88 lac shares of which we know buyer identity for 10 lac shares (India Midcap Fund ) , 9 lac shares (SBI Fund ) , 865808 shares (GMO Fund),950884 shares (Stichting Fund) . This comes to only 3716692 shares leaving a balance of 50.8 lac shares . Now there are 3 “large deals ” mentioned in money control without buyer identity on same date – In BSE 2212465 shares at 610 , In nse 99926 shares at 589 and in nse again 100414 shares at 592.55 .

It would be very interesting to find out the mystery HNI buyer for the block of 22.12 lacs shares . If anyone has any info please share .

Pix transmissions – low profile microcap company (17-12-2015)

Hi guys,

I am new to this forum. I would like to take this opportunity to open this thread on this microcap company.

The company is located in Nagpur, Maharashtra and commenced its operation from 1981. The company manufactures wide range of rubber V-belts and related products.

The key raw materials are synthetic rubber and natural rubber.

Key financial data – 2014-15 (Rupees in crores)

Equity 13.62

Reserve 135.59

Revenue 221.86

Of which exports 94.94

Net profit 3.91

EPS 2.87

As against market cap of 68 crores, the company is having net debt of Rs. 134.43 crores which is a cause for concern.

The company borrowed term loan @ 13.75% to 14% towards capital expenditure, new product .

The company sold one of its business for Rs.85.62 crores in the year 2012 and partly retired the debt.

Incidentally, the company declared special dividend of 30% in addition to 15% out of the profit on the above sale.

The company has exported products to more than 50 countries particularly to Europe and Middle East.

To cater the exports, the company is having two subsidiaries, namely, Pix Transmission Europe and Pix Transmission Middle East.

Pix Transmission Europe is having Pix Transmission Germany as its subsidiary.

Further, the company is having joint venture at Ireland and Middle East.

Though, the key raw materials synthetic and natural rubber are at low level , the margin is low due to stiff competition and economic slowdown.

The company is number one in India in this field.

The company is commanding brand equity in local and abroad.

It is having state of the art technology in adopting for manufacture and excellent infrastructure for hi-tech applications.

Hence , its products fall in special category.

The future performance of this company hinges on the growth of automobile industry, machinery manufacturing and agriculture.

The net profit of the company for the year 2014-15 has been halved over 2013, due to exchange rate fluctuation, high depreciation and interest cost.

The financial cost of the company itself is around Rs.15 per share.

For the current year also, the Q1 performance was dismal.

However, the company came out with better performance in Q2.

WHY THIS COMPANY?

The promoter, over the period, increased their holdings from 52% to 60.54%.

Though the dividend has been reduced from 15% to 10%, the dividend yield is attractive at 2%.

This shows the promoter’s confidence over the company.

The company is servicing the debt very well.

On clearing of at least 75% of debt alone, the earnings will increase substantially.

There is no pledge of shares by the promoters.

The company will show reasonable CAGR by cashing development of new products, capital expenditure made and rupee depreciation.

Due to economic slowdown, the company is not in a position to take opportunity of low key raw materials cost.

The company is continuously spending amount for new product development.

Once the economic revive, the company can increase the business as well as improve its net profit margin.

CONCERN

As on 31.03.2015, the company was having investment in liquid funds to the extent of Rs.12.9 crores and cash and cash equivalent at the extent of Rs.15 crores. It is not clear why this amount has not been utilized for prepayment of high cost debt. (In the year 2013-14 also, the company kept cash and cash equivalent at high level)

The company share is listed only in BSE.

Dis. Since I invested, my views are highly biased. The views are only to share information and it should not be construed as my recommendations for purchase/sale .

I request the members to critically analyse the company and to understand the future prospects of the company.

Suven Life Sciences – Embedded triggers (17-12-2015)

So consolidated books will shown an eps of 3.14 ( 40 crs on 12.73 cr shares ) for next 2 years ! Say between 3 and 4 eps for coming 2 years