Posts tagged Value Pickr

HBL Power: Signs of change (03-09-2024)

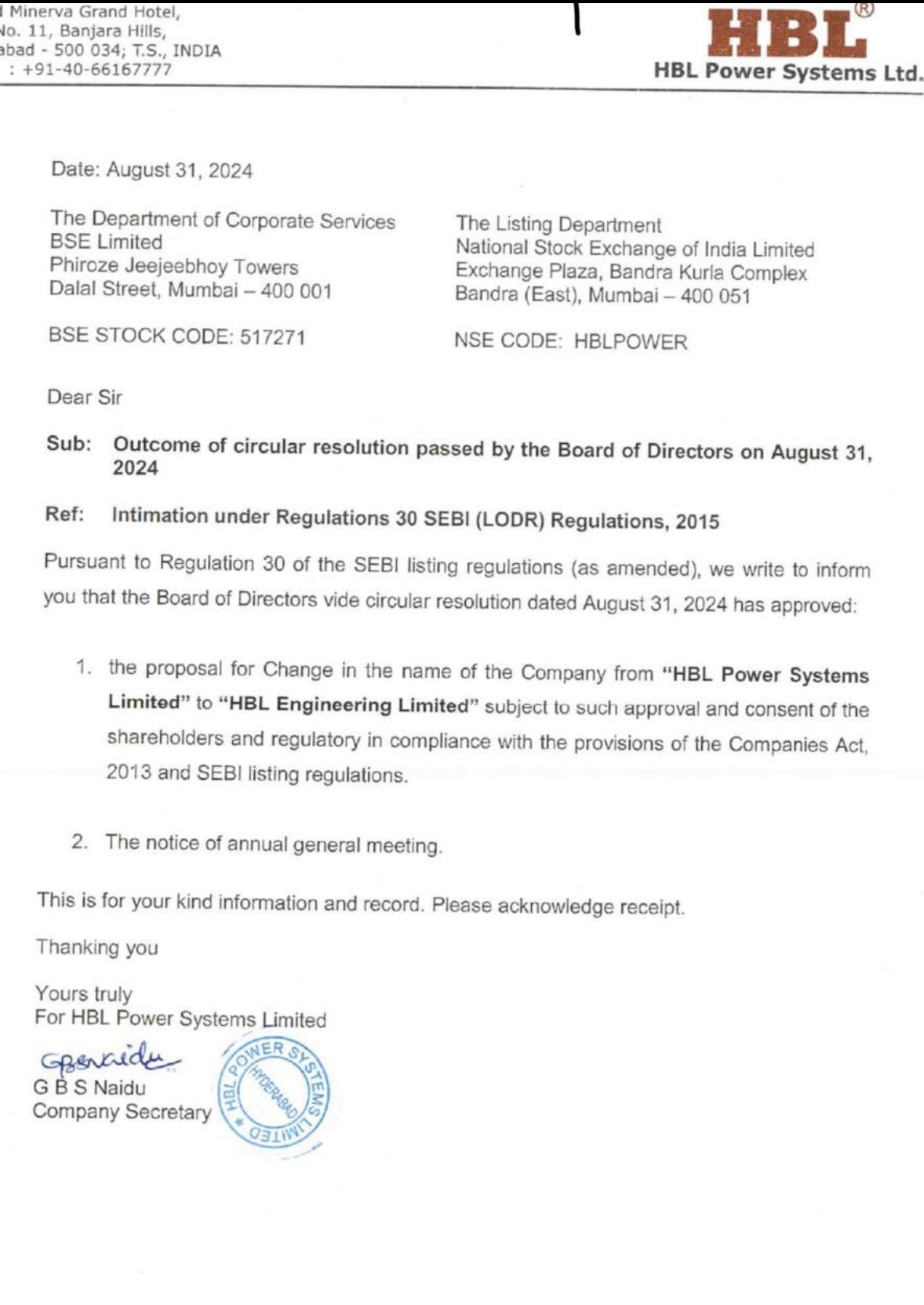

Compny name change -The Board of Directors of HBL Power Systems Limited approved a name change to HBL Engineering Limited on August 31, 2024.

Mayur Uniquoters ~ Market Leader in Indian Synthetic Leather Market (03-09-2024)

Mayur Uniquoters –

Q1 FY25 results and concall highlights –

Revenues – 213 vs 201 cr, up 6 pc

EBITDA – 48 vs 39 cr, up 28 pc ( margins @ 23 vs 20 pc )

PAT – 37 vs 31 cr, up 22 pc ( Q1 saw higher tax rate vs last FY )

Company expects their export OEM sales to be buoyant this yr and in next 2 FY’s as well

In light of increased business prospects from US based OEMs, company is looking to acquire industrial land to set up manufacturing and warehousing facilities in Mexico. Total planned capex for the Mexico expansion should be around 200 cr. Company is looking to set up a 60 lakh mtrs capacity in Mexico. But company will take the final decision only after the US elections are over by end of this calendar year

Export : Domestic sales for Q1 stood at 32:68

Total volumes in Q1 stood at 71.3 vs 70.4 lakh mtr YoY

Capacity utilisation of the PU plant is currently low @ 20 pc. Working with a lot of foreign brands to introduce company’s PU material for their leather goods and footwear. Hopeful of good order breakthroughs inside next 1 yr

Company is looking to clock 15 pc kind of topline growth for current FY

Company’s Marnie business is showing steady improvement. However the base there is small at present

Disc: hold a small tracking position, biased, not SEBI registered

Ranvir’s Portfolio (03-09-2024)

Mayur Uniquoters –

Q1 FY25 results and concall highlights –

Revenues – 213 vs 201 cr, up 6 pc

EBITDA – 48 vs 39 cr, up 28 pc ( margins @ 23 vs 20 pc )

PAT – 37 vs 31 cr, up 22 pc ( Q1 saw higher tax rate vs last FY )

Company expects their export OEM sales to be buoyant this yr and in next 2 FY’s as well

In light of increased business prospects from US based OEMs, company is looking to acquire industrial land to set up manufacturing and warehousing facilities in Mexico. Total planned capex for the Mexico expansion should be around 200 cr. Company is looking to set up a 60 lakh mtrs capacity in Mexico. But company will take the final decision only after the US elections are over by end of this calendar year

Export : Domestic sales for Q1 stood at 32:68

Total volumes in Q1 stood at 71.3 vs 70.4 lakh mtr YoY

Capacity utilisation of the PU plant is currently low @ 20 pc. Working with a lot of foreign brands to introduce company’s PU material for their leather goods and footwear. Hopeful of good order breakthroughs inside next 1 yr

Company is looking to clock 15 pc kind of topline growth for current FY

Company’s Marnie business is showing steady improvement. However the base there is small at present

Disc: hold a small tracking position, biased, not SEBI registered

Finolex Industries – Long Term Compounding Story (03-09-2024)

September 2, 2024

Finolex Cables Unveils Advanced E-Beam Irradiated LT XLPE Solar Cables

Finolex Cables, a leading player in the wire and cables industry, is proud to announce the launch of its new range of E-Beam irradiated LT XLPE Solar Cables, providing exceptional UV and ozone protection. Manufactured in-house at Finolex’s new state-of-the-art E-Beam facility in Pune, these solar cables leverage advanced electron beam technology. This investment in the E-Beam facility is part of a broader Rs 500 crore capex plan announced earlier that included expanding manufacturing capabilities, adopting advanced technologies, and enhancing supply chain infrastructure.

Designed to withstand extreme operating conditions, these innovative solar cables are capable of handling temperatures up to 120°C, with higher current ratings and superior durability making them ideal for demanding industrial applications and large-scale solar installations. Additionally, these cables are environmentally friendly and halogen-free, reducing the release of toxic gases in the event of a fire.

Compared to traditional chemical curing methods, E-Beam technology significantly improves the insulating properties of the cables, allowing them to sustain higher voltages with lower radial thickness and extending their life expectancy to over 25 years. This technology is now operational in-house which will be used for various upcoming products.

“As India accelerates its shift to renewable energy, Finolex Cables is strategically positioned to support the nation’s ambitious goals with our durable and high-capacity solar cables. The government’s target to expand renewable energy capacity to 500GW, including 270GW from solar power, has greatly increased the demand for top-quality and efficient solar cables. With solar power now contributing 18% to India’s total power generation in 2024 and expected to grow further, our solar cables are designed to adapt to the market’s evolving needs. As utilities face growing requirements under the Renewable Purchase Obligation (RPO) to integrate renewable energy, the demand for specialized solar cables is set to rise, making Finolex a crucial partner in India’s renewable energy transition,” stated Mr. Amit Mathur, President – Sales and Marketing at Finolex Cables. He further noted, “At Finolex, we aim to capture approximately 15% of the market over the next two years. We anticipate securing over 70% of this from the retail market by leveraging our extensive network of 200,000 retailers, 5,000 channel partners, and more than 750 distributors.”

Further, with the launch of solar cables to its portfolio, Finolex Cables is also committed to supporting government initiatives such as the Rooftop Solar Yojana (PM SURYAGHAR), which aims to solarize one crore households with an allocation of over INR 75,000 crore. This initiative provides up to 300 units of free electricity per month for solar rooftop systems up to 3 kW capacity, along with easy and affordable loans.

Rajesh’s portfolio (03-09-2024)

my biggest bet on cellecor is on management. they are young, 1st gen entrepreneurs and aggressive. taking on board experienced members with them will fetch them good results in future.

And as they have promised in past, they are launching new products also which will decrease there dependency on keypad phones.

Rudra’s PF and Information attic (03-09-2024)

Great reading list

While such detailed reviews are a good refresher, it is important to read the books yourself as there are always different takeaways from every reading for individuals and revisiting the key pointers post your own reading adds a lot of value towards retention as opposed to merely reading the reviews alone.

This thread is a treasure trove of such multidisciplinary readings which is so critical for an investor.

Sula vineyards – pioneers in indian wines (03-09-2024)

I checked few restaurants in Pune and found that they don’t serve Sula wines at all. Most of them serve Fratelli wines. Has anyone of you did some check on the restaurants in your vicinity? Is Fratelli more popular than Sula?

Krishca Ltd : A SME offering steel strapping Solution (03-09-2024)

Investing Accelerator Summit 2024 | Idea Presentation |

Krishca Strapping

Investing Accelerator Summit 2024 | Idea Presentation | Krishca Strapping

Valuepickr Nagpur (03-09-2024)

Starting this thread to interact with like-minded investors based out of Nagpur.