i dont know if you are aware of this nice post @safalniveshak

http://www.safalniveshak.com/2-year-course-in-smart-independent-investing/

i dont know if you are aware of this nice post @safalniveshak

http://www.safalniveshak.com/2-year-course-in-smart-independent-investing/

As far as I understand, Strides had taken a hair cut on these outstanding from Mylan mostly on these FDA observations so they would have to take confrontation route to recover anything from Strides.

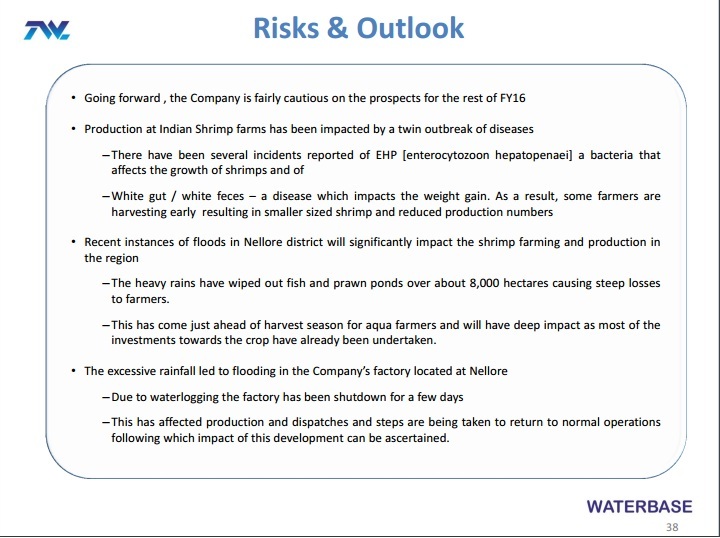

Strides arcolab also got affected.

Force motors…I do not know how much BMW and Merc contributing to their topline..

girish can you please share name of some good reads

Not sure how after a Sale this issues are dealt with

Bharat Group –

Comprises 3 companies : Bharat Rasayan Ltd. (BRL), Bharat Insecticides Ltd. and Bharat Agrotech Ltd.

Though in allied businesses of catering to agriculture industry, inter-company transactions / related party transaction are negligible – undermines good corporate governance. Total turnover of Bharat Group for FY2015 is Rs. 1035 cr. with BRL contributing majority of it at ~Rs. 470 crs.

Product –

BRL is manufacturer of Technical Grade Pesticide (TCP). Any pesticide has active ingredient and non-active ingredient. Active ingredient, also known as TCP, is a constituent working to destroy pests.

Non-active ingredient facilitates storage, transportation of product in totality. Basically, TCP is key raw material going into manufacturing of pesticide. TCP seem to be functional equivalent of OEMs to auto manufacturers. Link below gives more insights into TCP – http://www.vikalpa.com/pdf/articles/1990/1990_apr_jun_23_33.pdf

Capacity –

2 units at Mokhra (5000 MT) near Rohtak and Dahej (15000 MT) in Gujarat.

Dahej capacity commissioned in FY2013. It has filliped sales and profitability. Expansion was funded by debt. D/E increased to 2x in FY2013 from under 1x in FY2012.

Sales filliped from 97 crs. in FY2011 to 188 crs. in FY2013 and 439 crs. in FY2015.

Not sure why have OPM has tripled to 18% in FY2015 from 6% in FY2010

Certifications – BRL has ISO 9001:2008, ISO 14001:2004 and OHS 18001:2007 certification catalyzing long term partnership with institutional and foreign clients.

Clients – No meaningful data available. Will have to dig further.

Competition – very thick competitive space including companies like Kanoria Chemicals, Dhanuka Agrotech, Sabero Organics, Insecticides India, Camson Biotech, Kaveri, Rallis India etc.

Some concerns/aberrations –

1. Co. passed a resolution in FY2015 AGM to invest/advance loan/guarantee transaction up to Rs. 500 cr.

2. R&D expenditure as % of total expenses is too low (0.2%). Google search and some on-ground research suggests, TCP manufacturing involves lot of research to sustain

3. What are the growth drivers in coming years – expansion completed 3 years back, no new high margin products underway?

4. Raw material price risk – drivers of OPM?

Some highlights from AR read –

1. Foreign exchange earnings and outgo almost net each other, hedging exchange rate risk. This is consciously done by management.

2. Rising exports are mitigating vagaries of domestic monsoon – Exports as % of sales have risen from 20% (Rs. 27 crs.) in FY2012 to 30% (Rs. 117 crs.) in FY2014

3. No equity dilution over last decade while capacity quadrupled

and stock price falling could just an icing on cake for investors to load on

yes nexium is only recently launched, approval was on 19 oct 2015 and will take some time to get established. innovator astra zeneca still has around 60% market share.

the benefit in nexium is that a potential strong competitor in form of dr reddys is temporarily out of the field.

needs to be seen how torrent exploits this opportunity.