Dear Jana,

A very nice effort.

As Munger says:

“The best thing a human being can do is to help another human being know more.”

Wish you good health, happiness and a fulfilling 2016.

Warm regards.

Dear Jana,

A very nice effort.

As Munger says:

“The best thing a human being can do is to help another human being know more.”

Wish you good health, happiness and a fulfilling 2016.

Warm regards.

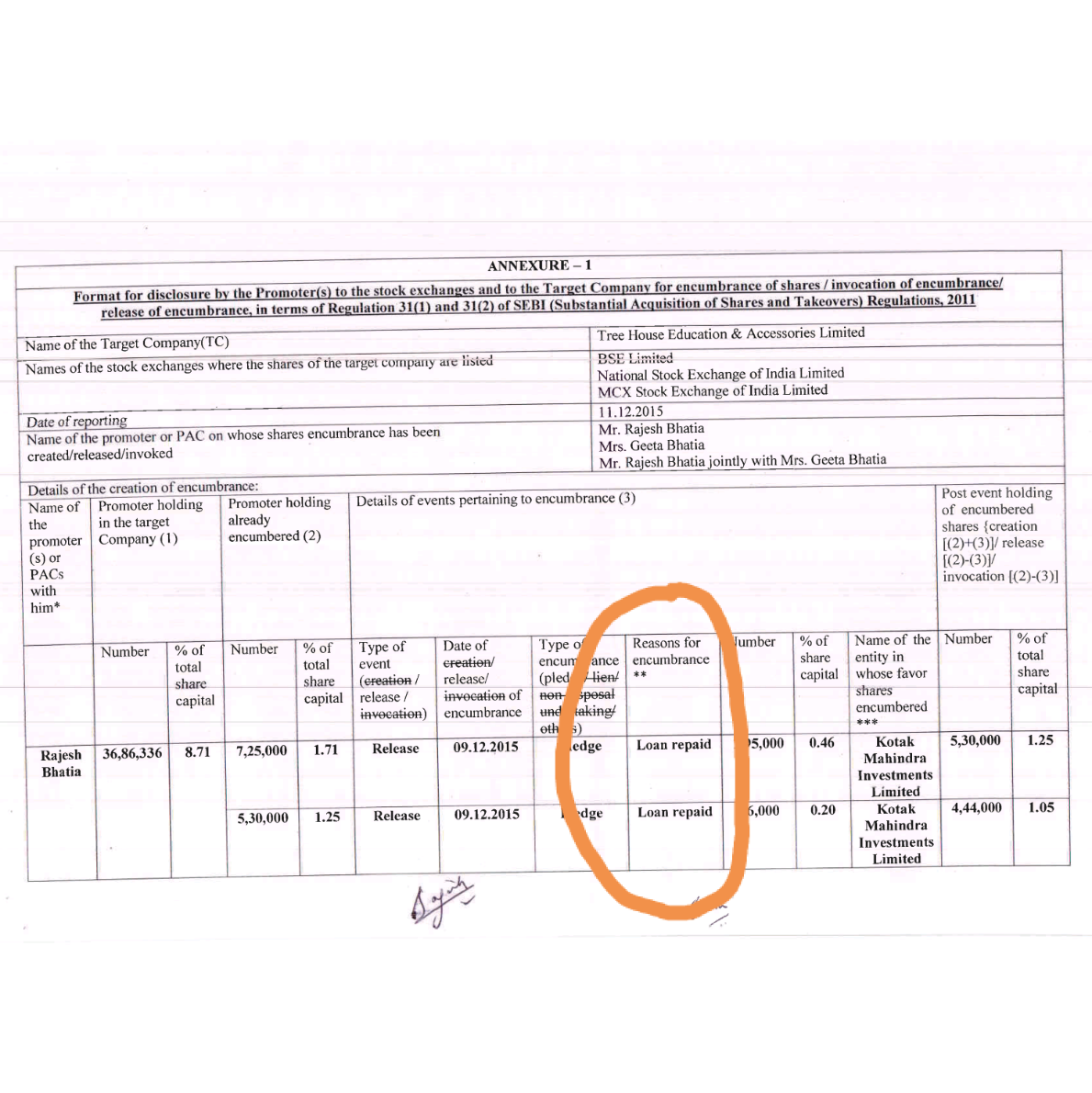

The pledged shares are released bcoz the loans are repaid by the promoters.

Please reread hazariwalapu ‘s and my post on this issue, it will give you some clarity . It has played out the same way. The promoters sold their unpledged shares – 9.5% of total outstanding shares . At a price of Rs 200.5/share via bulk deal . They used this money to repay the loans to the lenders. The lenders have released or given back the shares to the promoters.

Now the promoter holding is at 19-20.5% . The coming q3 shareholding pattern disclosure will confirm this.

Some value add information on Cupid as per the information available publicly, sources provided wherever required:

FC is expected to grow at 9% per annum until 2018. Cupid could possibly grow at 3 times this growth given the sweet spot it is currently at (required approvals in place, low cost producer, visibility in largest African markets).

Cupid is awaiting US FDA approval. Any approval must be a very big trigger as it opens the market for USA. Only FHC holds FDA approval.

http://www.psmag.com/health-and-behavior/female-condom-next-big-thing-safe-sex-78628

Summary is, it took a long time 6-8 years for the current female condom design acceptance and about 15 years to reach the current awareness. It may be that this awareness may turn into real sales now.

Typical feedback: Hard to use at first, but once you get used to it, it’s nice. This is where customer education is important.

http://www.bbc.com/news/magazine-25348410 -> Very insightful article.

It was written then in the article that “A smaller version aimed at the Asian market is in trial by Cupid”. Mr. Om Garg mentioned that this product is ready in his latest interview few days back in CNBC Awaaz.

I think Mr. Garg sensed this turnaround/opportunity and timed his return around 2008. He being an industry veteran as well helps in sensing the market opportunity.

Very informative website –

Important points from the above link:

Functionality Study

This Female Condom functionality study (Lancet), funded by the UAFC and carried out by MatCH (Maternal Adolescent and Child Health) of the University of The Witwatersrand, South Africa, was undertaken in 2011-2012. The trial aimed to assess the functional performance (breakage, slippage, invagination and misdirection) and safety of three new condom types — the Woman’s Condom, the VA worn-of-women (VA w.o.w.) Condom Feminine, and the Cupid female condom — against the widely available WHO/UNFPA prequalified female condom from the Female Health Company; the FC2.

Interpretation

This has been the largest and most comprehensive functionality trial to date and has provided important function data for these devices and has been used to compile evidence for WHO/UNFPA prequalification. Because of this trial, the Cupid condom has already been approved by WHO/UNFPA and is available for public sector procurement. Manufacturers of the other female condom products are using these data in their ongoing applications to regulatory authorities.

The attached study provides the in depth tests/trials done before providing approval to Cupid’s FC. So, getting this approval could be a built in moat as well for Cupid. See attached PDF below.

Excerpts From FHC annual report – “negative tone” actually. FHC is the competitor of CUPID.

Other parties have developed and marketed female condoms. None of these female condoms marketed or under development by other parties have secured FDA approval. FDA approval is required to sell female condoms in the U.S. The Cupid female condom became the second female condom design to successfully complete the WHO prequalification process in July 2012 and be cleared for purchase by U.N. agencies. FC2 has also been competing with other female condoms in markets that do not require either FDA approval or WHO prequalification. We have experienced increasing competition in the global public sector, and competitors including Cupid received part of the last South African tender. Increasing competition in FC2’s markets may put pressure on pricing for FC2 or adversely affect sales of FC2, and some customers, particularly in the global public sector, may prioritize price over other features where FC2 may have an advantage. It is also possible that other female condoms may receive FDA approval or complete the WHO prequalification process, which would increase competition from other female condoms in FC2’s markets.

The global public health sector market for male condoms is estimated to be greater than 6-7 billion units annually. The private sector market for male condoms is estimated at 10-15 billion units annually. The combined global male condom market (public and private sector) is estimated at a value of $4.5 billion annually. The female condom market represents a very small portion of the total global condom market.

Our success is dependent upon the success of FC2. FC2 is ‘low price’ alternative to FC1.

At this time, we derive our revenues from sales of our only current product, FC2. The ultimate level of demand for FC2 is uncertain, and we may not be able to grow our business if demand for FC2 does not increase. We also depend on public sector agencies around the world to continue to include FC2 in their STI prevention and family planning programs; and on our commercial sector distribution partners to successfully market and distribute FC2. A decline in demand for FC2 would reduce our net revenues and profitability.

Competition from other products, including other female condoms, may have an adverse effect on our net revenues and profit margins.

We may be unable to compete successfully against current and future competitors, and competitive pressures could have a negative effect on our net revenues and profit margins. Other parties have developed and marketed female condoms, although only one such product has WHO pre-clearance and none of these female condoms have been approved by the FDA.

Disclosure: I hold Cupid as disclosed earlier and am extremely bullish. Please do your own due diligence.

It is matter of time and hard work of the promoters is what the investors really want.

Cupid acceptance study.pdf (593.2 KB)

That is what I was trying to understand, @Lynchfan. Does a release of pledged shares in the open market (see the left column of that screenshot) not amount to a sale, in this case.

A pledge can be released either by the loan borrower paying back the loan and taking back the pledged shares, or the shares being sold in the open market by the lender, because the borrower is unable to provide additional collateral, should the lender so request.

In this case it seems it is the latter. Please clarify, if you know the answer. Thanks.

Hi Rajeev,

Many thanks for digging in and sharing the info. Whats worrying me is if individual equity investor would ever be able to get benefit of this deep undervaluation due to huge real estate value on books. I mean will management let retail investors benefit from it? Your views on that.

Thanks

Omkar talking about acquisitions and new business :

wow. end product has come out nice & thanks for sharing it so freely!

you make the boring subject of investing sound so interesting.

is this the culminating work of your year long hibernation or can we expect more interesting things

thanks, raghav

Relax,Any Equity Share transaction done through stock exchange will attract STT. So in LTCG no tax & in STCG 15 percent.