Broaders can lit me on this , as what is happening with kaveri is it possible that government tries to put price control on herbicides and pesticides, and besides this govt doesn’t gives subsidy to farmers and also doesn’t support manrega schemes will this impact on how farmers spend on agrichem ,that in inturn will impact on agri business of pi

Posts tagged Value Pickr

REPCO home finance – another Gruh in the making? (13-12-2015)

Floods have affected Chennai, Kanchipuram (more rains than Chennai), Thiruvallur, Nagapattinam and Cuddalore districts in Tamilnadu and also in Pondicherry/Karaikal. North East monsoon season is not yet done with and maybe other districts are affected. For example, I’ve read reports that in cauvery delta (Tiruchi and Thanjavur Disctricts) samba paddy cultivation areas are inundated.

It remains to be seen if floods this will seriously affect Repco’s business. In medium-long term I think this would be a non event. Anyway we need to wait for the quaterly results to gauge any hit in the earnings of finance companies. Auto companies who have manufacturing base in Chennai are the ones who are affected and will post lower earnings for sure. Eicher Motors have already announced that they have lost production of 11,200 motorcycles and still as of today running in 50% capacity only.

Sundaram Finance who is a dominant lender (they also have a HFC arm) in Tamilnadu has taken a hit in the markets. They have announced special 8.5% loans for flood affect home renovations upto 10 lac. This is from the NHB’s 6.5% refinancing package. So there might be opportunity like this to gain market share or earn goodwill & trust.

Disc: Invested in Eicher Motors only from the businesses discussed.

A Gentle and Practical Introduction To Value Investing (13-12-2015)

I will be delivering my final lecture tomorrow. You can find all my lecture notes in one file – https://goo.gl/TDsHnm

P. I. Industries Ltd. – A Unique Business Model can make it a Great Play on Agri & CSM Space (13-12-2015)

Long Term Capital Gains tax exemption will apply as STT would have been paid at the time of sale. Some CA friends can confirm this.

REPCO home finance – another Gruh in the making? (13-12-2015)

floods have not sunk the whole of tamil nadu it has damaged mainly chennai.one needs to find how much of their loan book is in the chennai area.disc invested 13% portfolio

Kaveri seeds company limited — kscl (12-12-2015)

I believe the main question currently is the visibility for FY 17, knowing that FY16 earnings can be considered given. Do we have more pointers from the field what are we really looking at? Any more data points available?

PS- Management Interview from Chand: http://www.moneycontrol.com/news/business/poor-rains-low-acreage-to-weighcotton-seed-vol-kaveri_4231621.html

REPCO home finance – another Gruh in the making? (12-12-2015)

What i heard, saw from TV it seems flood is mainly concentrated in Chennai. Can anyone help me to understand which are other areas in TN which are badly effected in flood. I doubt repco having too much ex-poser in chennai.

REPCO home finance – another Gruh in the making? (12-12-2015)

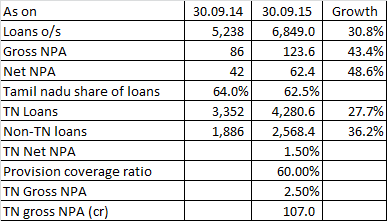

To try and guage the impact of Tamil Nadu (TN) floods, lets look at a few numbers:

Assume TN loans don’t grow (this is debatable, as there may be opportunities to lend for home redevelopment)

Assume TN gross NPA doubles to 5% of the loans outstanding (I think this is possible and maybe conservative assumption, given that loan repayment would be the last thing on the mind in current situation)

While this will not have to be provided immediately on default, it will attract 25% provision after 90 days.

![]()

The additional provision of Rs 53.5 cr (25% of gross NPA) appears significant considering FY15 PAT of 123cr and H1-FY16 PAT of 69 cr

One argument is that the loan would have to be classified as NPA only upon default extending over 90 days. In the next 3 months, it is possible that some of the borrowers are able to stabilise and resume their repayment. Upon full stabilisation, which could be 6-9 months away, and clearing off all the overdues, these loans can be re-classified as normal, leading to write-back of earlier provisions. Therefore, any adverse impact on financials might be a temporary situation.

Another is that the company can try and focus to compensate the situation by growing the non-TN book so that the overall impact is minimised.

A black-swan (sorry for use of the term) event could be that RBI gives a temporary concession/reprieve to banks and financial institutions to defer recognition of NPAs due to the floods situation.

Disclosure: I anticipate a spike in NPA over the next 2 quarters, impact on loan growth rates that the company has been posting till now, and impact on income and profits of the company (how much impact I am not able to gauge – and the above exercise is only an inexact attempt to quantify the discussions surrounding the topic).

Hence I reduced by holding by 20% at 690-700 levels recently. It still remains one of my top holdings and I remain convinced about the long term story. I will buy back my position if the price corrects significantly from here.

Neuland Laboratories Limited – Transformation towards niche APIs? (12-12-2015)

After reading some concall transcripts I noticed two critical things

1> EBITDA margin to improve to ~20% over the longer term

2> They have given a kind of guidance to grow at 25% CAGR for the next 3-4 yrs.

Taking these two into account I get close to 50% CAGR for PAT in my rough model. My understanding of their key strengths.

1> Regulatory compliance: they have huge expertise in handling regulatory issues so no US FDA shocker expected. They have more than 15 yrs expertise in dealing with US FDA without any adverse observations.

2> I believe their R&D capability is top notch. The promoter himself has spent considerable time as R&D head in an MNC pharma firm.

3> API pipeline is very strong and innovative. As mentioned above contract mfg. is also expected to grow strongly given their expertise in complex processes

4> Have not come across any other API manufacturer which is developing expertise in Peptides. These are complex molecules. Business potential looks good but don’t know much about this segment neither I have found any management comments.

Some cons:

Management is not yet shown any interest in developing formulations so margin kicker has to come from innovative APIs

Quarterly earnings have been lumpy and will remain so given their B2B focus

Their existing capacity utilisation suggests they need to invest in a new capacity by FY18 for which funds have not been finalised.

All in all a niche pharma company to watch out.

Disc: Have taken initial exposure and will watch closely

Satin Creditcare Network Ltd – Reaching out! (12-12-2015)

@anand6 and @Vivek_6954 and others have covered the relevant points on Satin and MFI nicely.

I think the NPAs are less due to

a) behavioural aspects like social/peer cognisance

b) Tiered structure of loan (quantum of loan increases as they complete pre-paying past loans)

c) Group loans

d) Relationship with lender due to timely/needy lending

e) If defaulted, the next option is from loan sharks which is very burdensome.

Particularly with respect to Satin vs. SKS Micro, I’m not sure how relevant is this valuation metric but I typically go by this –

a) Valuation Approximate figures –

1) SKS : AUM/Market cap = 6000/6000 = 1.

2) Satin: AUM/Market cap = 2200/1100 = 0.5.

PE and Book value wise as well Satin is a bit valued lower than SKS while I think Satin needs to be valued at or more than SKS valuations due to reasons mentioned in the thread I have initiated and below.

b) Geographic presence –

Satin is working in relatively under penetrated North Indian market and it has first mover advantage in some important states like UP/Bihar and also the leader in these important states.

c) Promoter stake, quality, experience –

I think both are neck to neck here and Satin would have upper hand as even during the AP fiasco days the NPA level did not cross 0.3%, which is great.

d) PE investors –

As Vivek mentioned, the PE investors are specialised MFI investors, for example NMI – Norwegian Microfinance who also invests in other countries like Bangladesh which is the originator of Microfinance concept.

http://www.nmimicro.no/about-nmi/introduction

e) Debt ratings and Opex/AUM metrics –

The current debt rating of BBB+ will move few notches up as the company ups scale with efficiency and so cost of funds will come down and better profitability while the same scope for SKS is limited as already SKS costs of funds is lowest among its peers. Opex/AUM for Satin is the lowest at around 6% which provides the efficiency with which Satin operates.

The risks are already mentioned in the Indian Microfinance thread by others and me.

As a general note, Microfianance companies should do well with the required regulations almost in place. Passage of MFI bill should provide further fillip (I need to read further on this).

Related thread initiated by me for further details on risks etc:

Disclosure: I hold Satin shares and this is a genuine discussion on the company. You need to evaluate and invest according to your risk profile.