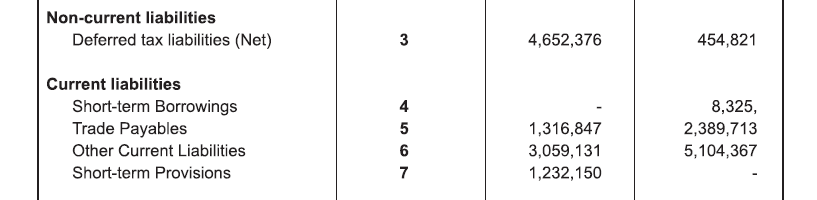

many companies borrow between the year and return it before 31st March. Its a common enough practice.

Thus, you will see interest income but no debt when the accounts are finalized.

many companies borrow between the year and return it before 31st March. Its a common enough practice.

Thus, you will see interest income but no debt when the accounts are finalized.

Company business

KLRF Ltd is a diversified company having interest in food, textile (Now closed as it was making losses) and engineering.

Its food division sells wheat, maida, sooji and aata under the brand ‘Kuthuvilakku’, ‘Kera’, and ‘Alaraman’. These products are packed in 5 kg to 90 kg bags (recently introduced 1 kg packs).

KLRF’s also has engineering operations that has interest in sheet metal fabrication like main door speed frame and cover printing machine. This division is also engaged in the business of iron castings. It exports iron castings to France and Germany.

It has nine wind mills with an aggregate power generation capacity of 6.25 MW. The company uses this for captive consumption for its engineering and wheat divisions.

Food division is located in Gangaikondan, Tirunelveli District, Tamil Nadu

Engineering division is located in Coimbatore, Tamil Nadu

Key Strengths

Established infrastructure from storage to warehousing of finished goods: KLRF’s food division has infrastructure from warehousing to storage of finished goods. Its warehouses can store upto 3,000 MT of wheat (raw materials) and has modern handling equipment. Its screen room, used for wheat cleaning and blending, has equipment to temper and blend 700 tonnes of wheat. Its roller flour mill has indigenous and imported equipment with capacity of 200 tonnes. It also has warehouses to store 2,000 tonnes of finished products.

Iron ore prices have decreased.

Key concerns

Engineering division

Availability of iron ore fines and scrap is the key requirement for foundries. Iron ore fines are the key inputs used to produce iron casting. Availability of fines at reasonable price is a key requirement for foundries.

The uncertain supply of iron ore to the industry and volatility in its prices impacts the operations of the industry.

Food division: Increase in the prices of wheat could impact the operating profit of the company

Other key strengths:

Equipped with modern technology for quality assurance:

To ensure the supply of high quality food products, KLRF has equipped its laboratory with equipment like rapid moisture testers, muffle furnaces, etc. and dough rheology testing including expamograph, photo calorimeter, sedimentation and maltose value estimation apparatus.

The textile division manufactured 100% cotton yarn in its two units. This division also had the latest machinery from Lakshmi Machine Tools, Reiter, Schlafhorst and Savio Orion. It also has a quality control and monitoring systems.

Trading income from the sale of coffee roasting and grinding machinery

Its sheet metal fabrication business has clients including Lakshmi Machine Works. Apart from having facility for sheet metal fabrication under one roof, this division trades in range of coffee roasting machinery of Probat Werke, Germany and range of coffee grinding machines of Mahlkonig, Germany.

Though this unit now appears to have been shut down.

Foundry has capacity to produce iron castings of 10,800 MT/annum. The company has an iron foundry that can produce iron castings upto 10,800 MT per annum. These castings are sold in domestic and export market.

Captive power (windmills) KLRF’s has 6.25 MW power generation facilities through its nine windmills. The entire production is used for captive consumption.

Increasing promoter holding Y-o-Y

Year Promoters

Mar-15 50.73

Mar-14 49.27

Mar-13 49.13

Mar-12 46.30

Mar-11 43.74

Mar-10 39.02

Mar-09 38.69

Mar-08 33.70

TTM eps is near about 10-11rs

Stock is trading at 57-58 rs

Book value is 55

ROCE stands at 12.5%

ROE is 13.88%

ICR is low at 2.05

D/E stands at 2.1

Debt at 48 cr as on March 2015

The management has been able to reduce the debt in last 4 years.

Food products from the company are available on some online sites

Due to the closure of textile division we might see the company making a turn around

Disclosure: Holding tracking quantity near 50 level. Will increase the holding as the conviction becomes stronger.

Please do your own research as the company is still at a nascent stage of a probable turnaround.

P.S.: Views invited

Recent management interview on Stake increase decision:

Suven has been granted a patent each by Eurasia, Europe, Israel and Macau for neuro-degenerative drug.

http://www.thehindubusinessline.com/companies/suven-life-gets-patents-for-neurodegenerative-drug/article7976497.ece

Let’s not jump to conclusions.. Promoters are too smart to “force” a sale. The non reported part of the buy would likely have been distributed to Institutional investors and Hni’s as well. Salil Singhal is In his 7th decade and would have his own motivations, which the market will doubtless query. This thread has sufficient discussion on the quality of Pi’s business which I do not want to regurgitate. The question to ask yourself is this. Would I buy this business at the cmp of 600 plus minus 10 pc; would I be willing to hold it for the next 5 years if the markets were shut. Will this business compound at 20 or plus pc at superior capital return ratios; will the cash generated be deployed keeping in mind the interests of all shareholders; what superior alternatives do I have to grow my invested capital? In case you are unconvinced sell now and sleep well. I’m happy to hold on take decisions based on Business performance.

On an unrelated note, Cartica who came in this June have 3 other investments in India, Page, Eicher and Supreme Ind. As far as I know they are in for the future that they feel this Business has.

this perfect setup any kind of such sale…they might have contacted operator to do the sale…There are lot of examples of this kind(in the book Reminiscences of Stock Operator..must read)

Central government heeds to demands of cotton seed sellers. The royalty issue may be settled in favour of seed companies. Could this be a savior for Kaveri in this distressed times of bad weather.

mgt should clarify their rationale for such forced sale

Somehow, I get a different feeling on this whole episode, my thought process as I look back the past 2 days is written below. I may be thinking unnecessarily and all the below will not have any impact on the business at all, but let me put my views anyway.

1 day before the stake sale, there was a huge spike of the stock until about 710 and there were pending buy orders of 28000 plus on BSE, if I remember correctly as I have looked at this data due to the unusual spike.

a. Someone might be testing the upside strength of the stock

b. This spike would have given psychological advantage to sellers the next day as looking at a stock which touched 700+ a day before and being available at around 600 the next day will make buyers plunge for a buy.

The above points are important because only half of promoters stake were bought by big boys while the other half is a forced sell on the market as observed by boarder in the above post.

Interestingly, promoters could secure big boys for only half the amount of stake sale and the rest is sold to public! Of the 8800000 shares sold by promoters, 3716692 were bought by big boys.

Anyway, I will rest my rant on this topic here, let me move on.

Have a nice weekend.