Man, so many actionable insights. I love how every time u refer as us (hum) rather than (mein) which I have seen in a lot of businessmen/ founders. Would love to be in ur network in the future when i will do something worthwhile. Thanks for sharing.

Posts tagged Value Pickr

Piccadily Agro Industries Ltd (02-09-2024)

The real question is – Can Indri be a million cases per year brand in 8-9 years ?!!

If the answer to that question is yes, then Indri will generate: Revenue of about 3100cr

(current EDP ~21000 per case + price escalation of 4.5%/yr for 8 yrs = Rs31,000 per case)

(Assuming GM of 70% (per mgmnt) and advertising + dep + Other Expense =300cr )

And, PAT of around 1400cr same as United Spirits PAT in FY23

That is PAT of just Indri alone = Entire United Spirits with a MCAP > 1lac cr

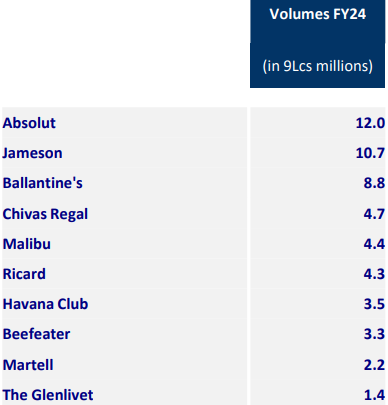

Some million cases (worldwide sales) brands:

Johnny Walker – 22 M

Glendifddich – 1.4 M

Teachers – 1.3 M

And obviously, many Indian non-premium brands from United Spirits (Diageo) & Radico sell more than a million cases per year.

Some questions to think about:

Can Piccadily come up with another blockbuster brand just like Indri in the next 8yrs ?!!

Can they come up with maybe 2 more in the next 8 yrs ?!!

If yes, then what happens to PAT in 8 yrs – can Piccadily’s PAT be twice or three times that of United Spirits FY23 PAT ??!!

Hero Motor – Leader in two wheeler (02-09-2024)

Hero MotoCorp registered a month-on-month growth of 38% in its overall dispatch volumes and has sold 24,17,790 units in FY’25 (Apr-Aug), a growth of 8% over the corresponding period of FY’24.

Adani Transmission – High growth potential (02-09-2024)

AESL won the project through the tariff-based competitive bidding process and will commission the project in the next 24 months on BOOT (build, own operate, and transfer) basis and maintain it for the next 35 years, according to the statement.

“As the world’s largest renewable energy park, Khavda demands power evacuation infrastructure that is not only world-class but also resilient and future-ready,” AESL Chief Executive Officer Kandarp Patel said.

Adani Acquires 7 GW Khavda Transmission Project – Rs 4,091 Cr Investment: Rediff Moneynews

E-pack durables – ODM worth a serious look (02-09-2024)

I agree with your point that there are no big differentiators for Epack vis a vis others and PG has a better margin among the lot. Epack seems to be having an edge on the valuation front ( relative to peers ). Also Epack is one the most backward integrated players among AC ODMs ( My opinion and I might be wrong ).

As mentioned in the risks earlier most of the OEMs have started manufacturing ACs and it is a threat to ODMs like Epack, Amber and PG while overall AC demand and growth is here to stay .

Indiabulls Housing – A compounder from here? (02-09-2024)

Thank you Mihir for your views and the crisp analysis in the thread. A couple of things standout for me from the excel sheet that you shared. Shouldn’t a sub 2x gearing on an equity of >20k Cr be easily more than >30k Cr? That should hopefully help with a better RoE than projected by you.

The estimate of 1800Cr PAT in FY27 just gives a PAT CAGR of 15-16%. The current PAT is already in excess of 1200Cr. So, essentially you are saying that someone should be investing more for the market to re-rate the stock and not so much on the earnings potential?

Cambridge Technology Enterprises (02-09-2024)

This article illustrates the development made by the company

Premco Global — Narrow Fabric (A critical component for inner wear) (02-09-2024)

@HIMSHAH

That’s the perfect way …

It’s very meaningful if u can disclose ur portfolio…

Thanks🙏

Pitti Engineering Limited: Is it on an inflection point? (02-09-2024)

Target of Pitti Engineering Limited revised by K R Choksey

The new target is 1552

PGINVIT impairment of investments in subsidiaries and book value (02-09-2024)

@praveen_sham I mailed PGInvit regarding concall. Their response as follows.

“Regarding the earnings call, we would like to inform you that the Annual Meeting (AM) was held on 26th June 2024, where investor queries were addressed. Given the short time difference between the AM, the quarter ending, and the release of results, an earnings call was not conducted. While it is not mandatory to hold an earnings call every quarter, we have consistently conducted them each quarter. Once the next earnings call is scheduled, the information will be disclosed on our website and through stock exchanges for the public at large.

As for our growth strategy, we are actively pursuing acquisition opportunities for operational power transmission assets. However, it is important to note that the availability of such assets from private developers is currently limited. The adoption of the Government of India’s guidelines for asset monetization by state entities is expected to be a gradual process due to the novelty of the proposed mechanisms and the complexities involved in their implementation. We are in continuous touch with the Government authorities on the issue and updates shall be provided to the unit holders as an when the clarity emerges on the subject.”