Last year, they have give guidance of 250-350MW Pv module sales for FY24 and missed it by a huge margin

Posts tagged Value Pickr

PGINVIT impairment of investments in subsidiaries and book value (02-09-2024)

Has anyone got any idea, if they are really talking to state Transcos for acquisition of their assets ?

It’s a strange situation where in the sponsor (PG) has lost interest in invit route and thrown baby (PGinvit )out of the bath tub just after the birth (IPO ) . PG has adopted securitization route instead of Invit and unitholders are left to the mercy of junior babus of PG who rotate as senior management position in PGinvit! If boss (top leadership at PG) has lost interest in invit then it’s just a vacation posting for junior guys who rejuvenate by their stay in invit and once reenergised go back to parent company for productive service…

I don’t see any real hardwork and efforts these stop-gap management at invit are doing for AUM growth.

Now they have stopped concalls also, so no pressure of answerability to unitholders.

Disc: invested.

Deepak Fertilizers and Petrochemicals (02-09-2024)

@manhar Can you help me out on valuing the entire business? As I am just a beginner and so I need some help.

Kilburn Engineering – Huge undervaluation (02-09-2024)

This is what the management clarified in the Q1FY24 concall. This is a snippet from my notes that I take after going through concalls of all the companies I hold/track. This info could be a bit dated especially when it comes to holding % of different promoters in the company.

Promotor Group Structuring:

□ One part is the promoter group from the Khaitan family. The Khaitan family holding is approximately 22% – 23%.

□ Second, we have a strategic investor who has invested by the name of Firstview Investments. It’s an investment arm of the OCCL group, which is Oriental Carbon group. This group holds 35%.

□ Promoters are there just to give strategic guidance, but it’s a professionally run company. Major promotors brought in new management to run the company but the promoters are not involved in day-to-day management.

□ One of the big changes that has happened is the management change. Mr. Khaitan just explained that now it’s a professionally run business. So, the decision-making processes are far faster, quicker, and very focused. This is a big change that has happened from the past.

Hope this helps to explain what Amritanshu Khaitan’s role is in the company.

Disc: Invested from lower levels.

Deepak Fertilizers and Petrochemicals (02-09-2024)

@Prateek_Mishra Have you studied the business in detail. And, if can you share with me the reasons because of which you think post demerger things will be interesting.

Ranvir’s Portfolio (02-09-2024)

Technocrat Industries –

Q1 FY 25 results and concall highlights –

Revenues – 620 vs 556 cr, up 11 pc

EBITDA – 146 vs 145 cr ( margins @ 24 vs 26 pc )

PAT – 84 vs 91 cr

Segment wise revenues –

Drum closures – 151 vs 127 cr, up 18 pc

Scaffoldings and Formworks – 334 vs 274 cr, up 22 pc

Textiles division – 104 vs 139 cr, down 25 pc

Engineering and Design services – 49 vs 42 cr, up 18 pc

Segment wise EBIT –

Drum closures – 55 vs 40 cr, up 38 pc

Scaffoldings and Formworks – 53 vs 77 cr, down 31 pc

Textiles – (-) 12 vs (-) 4 cr

Engineering and Design services – 8 vs 9 cr

Company is hopeful of an improved performance in the Drum Closure division. No major capex ( except maint capex ) planned in this division

Company is confident about a margin revival in Scaffoldings and Formwork division because of anticipated growth in infrastructure and housing led demand in India. Company’s 02 plants in Aurangabad to make 17,500 MT of Aluminium Extrusion and 6,00,000 Sq Mtr of Aluminium fabrication has commenced production in Q1 ( a reason for lower EBIT in this segment due higher depreciation ) . They will be ramped up over the course of FY 25

Expecting the demand for engineering and design services to remain strong due to the strong acceptance of their offshore global delivery model

Company is the second largest drum closure manufacturer in the world, currently exporting to 75 countries. Company is guiding for single digit growth in this segment but the margins will sustain in > 30 pc band

Because of commercialisation of the Aurangabad facility, company expects incremental topline of 450 cr and EBIT of 80 cr for FY 26. For FY 25, incremental topline and EBIT should be 60 cr and 10-15 cr respectively

The scaffolding business continues to be soft in Europe. However, demand from US is descent

In the textiles business, company has commissioned a new spinning unit in May. Revenue from that will start to flow in Q2 whereas the expenses started to come in Q1. From Q2 onwards, company sees a descent uptick in the textiles business. For full FY, should add around 130 cr of topline to the yarn business. All textiles divisions combines ( Yarn + Fabric + Garments ), topline should be around 650 cr

Also expecting the textiles division ( Yarn + Garments + Fabric divisions ) to be EBITDA positive for this FY ( EBITDA percentage in the range of 8-10 pc )

Company is still awaiting – B certification in Europe for its Scaffolding business. They are expected to get it sometime in Sep

Aluminium formwork’s demand continues to outstrip supply ( despite having local and Chinese competition ). Local demand is so good that the company is not even able to export this product. Company’s current Mkt share in India is around 10 pc or so

Company’s steel formwork business did witness softness in demand in Q1 – because of the elections. Should pick up going forward. However, company’s main thrust and bulk of the business continues to come from Aluminium formwork. ( Steel formwork is mainly used for Infra projects while Aluminium formwork is mainly used in Real Estate sector )

Company sees very good demand outlook for its MAK-1 – aluminium formwork business – both from domestic and export markets for next 2-3 yrs

LY, company’s scaffolding + Formwork division did revenues of 1030 cr. This yr, company is expecting to do around 1250 cr and next year, they are expecting to do > 1800 cr from this segment ( because of the new capacity coming online )

For engineering services segment, expecting to do 20-25 pc CAGR topline growth for next 2-3 yrs

Expecting to touch a PBT of 500 cr for FY 25

Disc : holding, biased, not SEBI registered, not a buy / sell recommendation

Meghmani Organics Ltd (02-09-2024)

- Strong volume growth in both Crop Protection and Pigment segments in Q1 FY25

- Revenue remained flat at INR 411 crore, EBITDA increased by 194% YoY and 40% QoQ to INR 14 crore

- Profitability impacted by lower product price realization across markets

- Management expects price improvement and demand recovery to enhance profitability going forward

- Crop Protection segment revenue was INR 272 crore, EBITDA of INR 11.3 crore with 73% capacity utilization

- Pigment segment revenue was INR 138 crore, EBITDA of INR 9.4 crore with 45% capacity utilization

- Management is optimistic about regaining normal double-digit growth trajectory

- Focus on new product launches in Crop Nutrition segment to provide comprehensive solutions for farmers

- Inventory levels have become reasonable across most products after a period of destocking

- Received Responsible Care Accreditation for Crop Protection segment and Committed Badge from EcoVadis for sustainability efforts

- Launched 8 new products in Crop Nutrition segment during the quarter

- Demand recovery seen across both Crop Protection and Pigment segments

- Gradual price improvement expected going forward

- Focus on new product introductions and improving capacity utilization

- Headwinds: Lower product price realizations, volatile raw material prices

- Tailwinds: Improving demand, potential antidumping duty on Titanium Dioxide from China

- Launched 8 new products in Crop Nutrition segment

- Titanium Dioxide plant in Phase 1 running at 35% capacity utilization, expected to reach 70% in H2 FY25

- Nano Urea plant expected to run at 35-40% capacity utilization in the first year

- Potential antidumping duty on Titanium Dioxide imports from China expected in Q3 FY25

- Targeting 20% revenue growth this year and next year

- Expecting EBITDA margin of around 15% in the next financial year

- Confident about regaining normal double-digit growth trajectory

- Expect profitability to improve from Q2 onwards

- Focus on sweating the current asset base before considering further capacity expansions

- Debt reduction is a priority, targeting significant reduction in the next 2 years

- Question on demand recovery and pricing trends:

- Demand has started improving across both Crop Protection and Pigment segments, not just in one market. This is due to destocking of high inventories and improving market conditions.

- They expect gradual price improvement going forward as the demand picks up.

- Question on Brazil market and monsoon impact:

- Inventory levels have become reasonable in most products, and they expect good demand from Brazil due to the positive monsoon forecast.

- Question on product pricing:

- Prices have been at the bottom level but expect improvement as demand recovers, as the current pricing is not sustainable.

- Question on China behavior and freight challenges:

- Chinese prices are already at rock bottom levels and cannot go down further. They expect the freight challenges to normalize from Q3 onwards.

- Question on new product launches and their contribution:

*Launched 8 new products in the Crop Nutrition segment, which are relatively high-value and have better profitability. These new products will be a key focus area going forward. - Question on Pigment segment performance and capacity utilization:

- Focusing more on profitability rather than aggressive capacity utilization in the Pigment segment. They expect capacity utilization to improve gradually but not drastically.

- Question on Titanium Dioxide facility and its economics:

- Provided details on the Phase 1 capacity, revenue potential, and the expected 20% margins once the facility reaches 70% utilization, along with the potential benefit of the antidumping duty.

- Question on Nano Urea segment’s profitability and utilization:

- Expect 15-17% margins on Nano Urea and the plant is designed to be profitable even at 30-40% utilization in the initial years.

- Question on capital allocation and return thresholds:

- Typically target an IRR of 18-20% for new projects, but the dynamics have changed, and they are now more focused on sweating the existing assets before considering further expansions.

- Question on revenue and EBITDA guidance:

- Guided for 20% revenue growth this year and next year, and an EBITDA margin of around 15% in the next financial year.

NGL Fine-Chem (Animal Health + Human Health + Vet Formulations) (02-09-2024)

Hi! I recently started following this company. Does anyone know what “training expenses” of Rs. 86.5 lakhs the company is bearing on behalf of Mr. Ahaan Nachane (son of Mr. Rahul Nachane)?

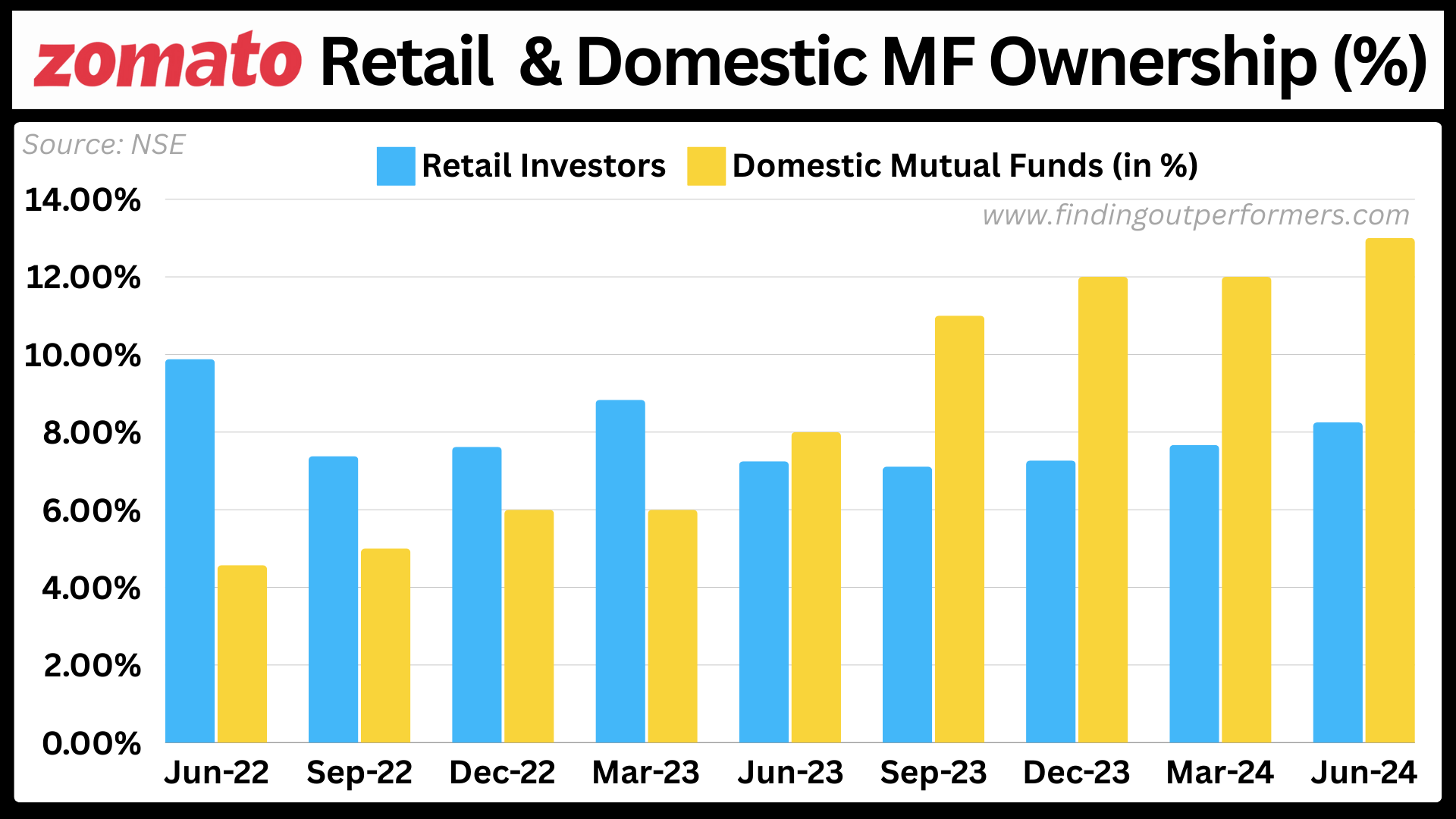

Zomato – Should you order? (02-09-2024)

People on socials have been mentioning a lot on Zomato/ Blinkit in last few months, is it impacting the share price?

In the last 2 years as share price of Zomato has rocketed by 5X, one might think a lot of retail investors are buying into the story. Also because more & more people are now getting to know & experience quick commerce i.e. Blinkit – loyal customers tend to become shareholders more often! (agreed?)

One must note that Zomato’s listed shares have witnessed roughly 45% of its equity being sold by top PE funds & others in last 2 years ever since the lock in restriction by SEBI got over since 25th July, 2022 (which is 1 year post listing). Sellers include Uber, Alibaba Group, Tiger Global Management, Sequoia & more. So there is a huge gap inform of free float that got added, retail investors might have filled some of that gap, right?

BUT DATA TELLS A DIFFERENT STORY!

Retail investors own barely 8% of Zomato and their holding has not increased (rather falling over 2 year period!). Neither do analysis of google search trends confirm any rise in interest in share price of Zomato in last many months!

This week we presented a detailed analysis on fast changing share holding patterns of Zomato in the last 2 years on ‘Finding Outperformers’!

Multibagger Hunt: Opportunities & Challenges Part II (02-09-2024)

**Multibagger Hunt: Challenges and Opportunities Part II**

Maximum Point of Pessimism

Often, investors rush into buying a stock, eager to catch the next big winner in the market. The news is overwhelmingly positive, every analyst is recommending it, and trading volumes are surging daily. Everything seems perfect, and we buy in just when the stock has peaked. But the next day, the price starts to dip, bit by bit. As the initial excitement fades, the stock begins a downward spiral. We wait, hoping our analysis was not wrong, convinced the stock could not fall any further. But it does—first a 10% drop, then another, and soon it seems like everything is conspiring against us.

Regulators notice the erratic price swings and place the stock under surveillance. Now the real pain begins. The stock sinks even further. We cling to the hope that the so-called multibagger, which everyone was raving about, will recover. But eventually, the stock loses most of its value, leaving us with significant losses. At this point, we cannot take it anymore. We exit the stock, often at its lowest point—this is the maximum point of pessimism. Ironically, it is usually when the stock is ready for a rebound. However, the emotional toll prevents us from seeing any potential upside, and we hastily cut our losses, missing out on the eventual recovery.

One recent example, discussed in Part I, is that of Protean. After lacklustre third-quarter results in 2023, the stock plummeted to the 800-850 range, a steep drop from its peak of over 1500. However, the very next quarter saw significant improvement. New verticals were launched, new opportunities arose, and the stock took a dramatic U-turn, now trading well above 2000—all within six months.

Common Sense Investing

Investing does not have to be complicated. Most of it is rooted in common sense. Yet, we often think it is like rocket science and defer to so-called experts who bombard us with complex spreadsheets and formulas. We believe the more complicated the analysis, the more credible it is. But consider a company like Protean eGov Technologies, which builds digital infrastructure with funding from financial institutions and government agencies. It offers e-governance solutions, holds a market share of nearly 50%, and expands its verticals every year, winning global awards. Investing in Protean is almost a no-brainer.

I overlooked Protean when it was trading around 800-900. It only caught my attention after I read an article about digital infrastructure—an emerging theme as more government schemes move to digital platforms. Upon visiting Protean’s website, I discovered that they are leaders not just in PAN card processing but in several other emerging areas.

What’s Next?

With these new verticals, Protean is poised to become an industry leader. The only challenge is the collection of dues from various state government agencies, which sometimes causes them to miss quarterly targets due to delays in payment clearance. However, the growth potential from these new verticals should drive the stock to greater heights. All in all, the outlook for Protean is very promising.