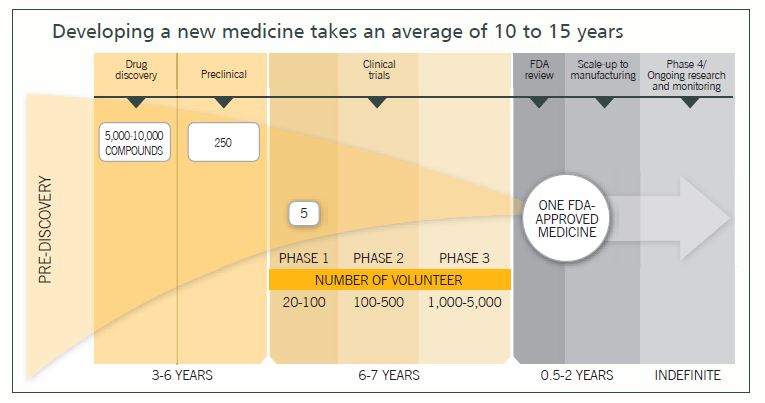

What about Phase 3 trials and the Global trials ?

Posts tagged Value Pickr

Suven Life Sciences – Embedded triggers (30-11-2015)

As per management commentary in AR 2014-15, the Phase-Ib trials for SUVN 502 is completed and commenced preparations for the Phase-IIa (POC) trial. The management hope to initiate patient trials during the second half of the current year and are hopeful of monetising this molecule post successful completion of the study in fiscal 2017.

Suven Life Sciences – Embedded triggers (30-11-2015)

So we can assume that still it might take 5 years for SUVN-02 to get approved by FDA taking assuming it takes 1.5 yr for Phase 2, 2 for phase 3 and 1.5 for final approval and building manufacturing capacities.

Kellton Tech – Fast growing IT guy in ISMAC space (30-11-2015)

What I am trying to understand is the reason for difference in margins. The difference is huge. 8kmiles have 50% more margins than Kellton and even Cambridge has more margins than Kellton. I think you are right that everybody is going for IOT and I believe that we should have a basket of 3-4 companies if we want to play ISMAC. Big gun like Oracle is also entering into cloud service (one of my friend based in US told me).

I did not entered into Cambridge because it was ultramicrocap and now continuous upper and lower circuits scare me. I was invested in 8k miles soft from 600 levels and booked out completely at 1750 because I think the stock price completely discounts next 1.5 year performance. I will be willing to add if there is any fall as I like its clients and the margins 8k is making from those clients.

Neuland Laboratories Limited – Transformation towards niche APIs? (30-11-2015)

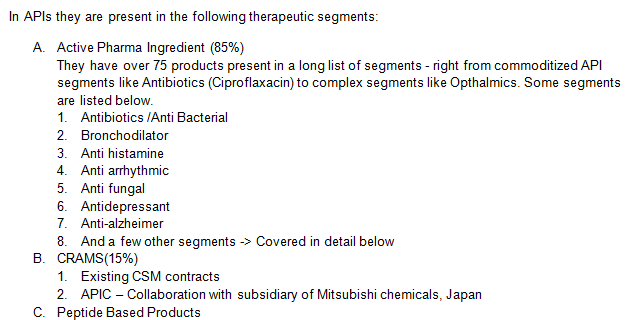

Neuland Laboratories Ltd a 30 year old pharma company is a predominantly API manufacturer (85% ) with a some presence in CRAMS (15%) derives 88% of its revenues from US, Europe & Japan.

Neuland claims to have to transformed itself from manufacturing commodity APIs towards having capability to develop complex molecules in niche segments – Opthalmic, Schizophrenia, anti-asthma, anti-fungal. -> This is verifiable easily. We will see in the subsequent sections.

Their top five products contribute to ~4% of the topline while top 5 customers contribute ~40% of the topline.

Active Pharma Ingredient (85%)

In API manufacturing, the competitiveness of a manufacturing company is determined by one of the following ways:

1. Build massive scale, cost advantage in commoditized APIs – A new competitor won’t be able match you (or)

2. Identify niche APIs which has complex chemistry so that competitors will find it difficult to imitate. -> How to verify this? Look at the molecule, find out the # of DMF filers for that molecule(may give a hint).

Neuland claims(or HAS IT?) to have graduated from #1 (above) towards building capabilities in developing niche complex APIs in segments like Opthalmics, Anti-asthma & Bronchodilator segments.

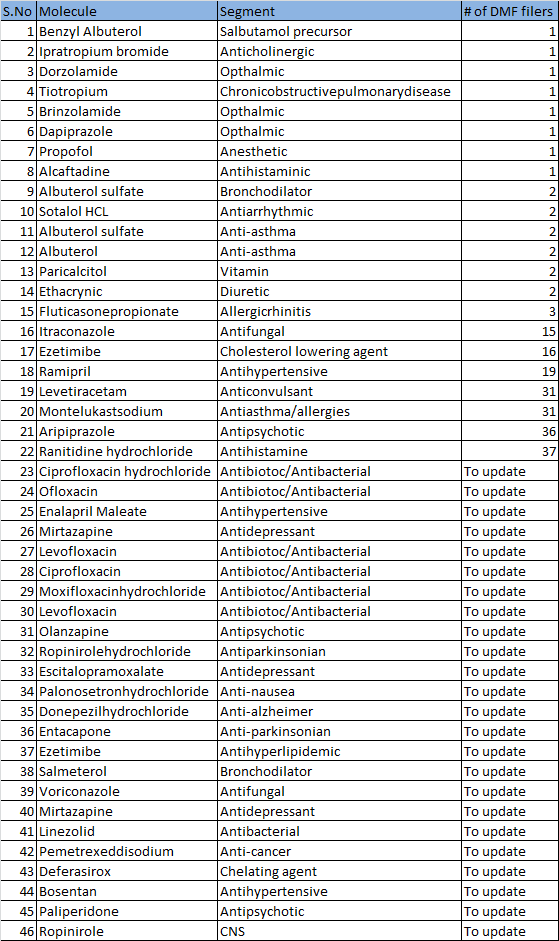

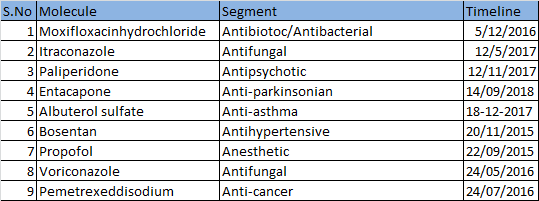

Here is the current list of Products from Neuland’s with the # of DMF filers:

To update – I am working on identifying the # of competitors for these molecules. Will update after I complete. All these molecules have more than 1 competitor.

Some observations:

- In about 15 molecules, Neuland is either the only player/ has only one another competitor.

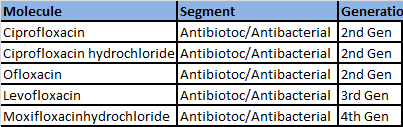

- In antibiotics:

a. Higher the generation the molecule is present in, higher the margin for the company. The company’s presence in 3rd and 4th Gen molecules indicates R&D capability of the company.(check the table below)

b. In Antibiotics, Ciproflaxacin is a commoditized API. Neuland is moving away from this molecule. A few years back, 65% of their revenues were from this molecule vs 15% of their revenues from Ciproflaxacin now ->Aarti Drugs is the global leader here.

3.For commoditized APIs, Neuland’s claims to play the volume game. – this contradicts in case of Ciproflaxacin – Aarti has taken away significant market share in the last 3 years from Neuland.

4.Visibility of earnings : About 10-11 APIs for which DMFs have been filed, are expected to go off-patent in the next 3 years. Timeline column indicates the expiry date for the patented version of the molecule in US market.

CRAMS:

Contract Manufacturing involves manufacturing APIs based on custom specifications of the customer.

1. Their Contract Manufacturing segment has grown at a CAGR of ~70% in the last three years.

2. They have non-exclusive agreement to manufacture custom products with leading Europe & US customers.

3. Recently a large US customer has filed an NDA for the US market which is said to throw up an interesting opportunity – have to verify this claim

Pact with Mitsubishi Chemicals:

Neuland has entered into a pact with API Corporation (subsidiary of Mitsubishi chemicals ) to manufacture custom products for APIC.

APIC has invested 15 crores in their existing Pashamylaram facility to create the manufacturing infrastructure.

Neuland gets reimbursement of the operating expenses incurred at this facility – Don’t understand the revenue model here. Need to research more.

Neuland has developed some expertise on Peptide based products which are considered very complex in chemistry field.

Questions/Summary:

The company definitely looks decent especially:

a. it looks like it is trading at 12 PE based on FY17 earnings

b. # of molecules where they have limited competition.

c. Added Revenue visibility from APIC contract with Mitsubishi

But the following questions are key before one considers investment here. The management seems very transparent as they have disclosed most of what is required in every concall.

- Imitability: The above pipeline of molecules going off-patent in the next few years looks interesting. But how difficult is it for a new API manufacturer to develop these molecules?

-

Debt: API manufacturing companies go down when they take the path of debt – Wanbury (global leader in Metformin), Parabolic(Cephalosporin), Indswift labs all failed because of financial distress and not because of lack of demand for their products.

As of now their D/E ratio at ~1 looks decent for an API manufacturing company especially considering the future growth possibilities. What is their approach towards debt? - What is their revenue model with API Corporation?

I wanted to look at some pharma names outside our comfort zone – i.e. Torrent, Shilpa, Ajanta etc. That’s when I zeroed in on Neuland after researching other API manufacturers like Aarti, SMS, etc.

I am still researching on this idea. Will update this thread as an when I find out more.

Thanks,

Ravi S

Disclosure: I have no positions in Neuland as of today. I may initiate a position in the next few days in this company based on further analysis.

Kellton Tech – Fast growing IT guy in ISMAC space (30-11-2015)

With all due respect, I think it would have been good to have a more balanced view including risks and few other points, etc,.

For e.g.

-

What are the risks associated?

-

What other businesses have promoters been into if they are serial entrepreneurs, i.e. their track record etc,.?

-

What is the focus of promoters on this business i.e. they being serial entrepreneurs, are they involved in other businesses too at present?

-

Kellton seems to have multiple other business interests like:

Kellton Commodity & Derivatives Pvt. Ltd

Kellton Infra Pvt. Ltd.

Kellton Financial Services Pvt. Ltd.

Kellton Insurance Services Pvt. Ltd.

Kellton Securities Pvt. Ltd.

What is Kellton doing with all these businesses? Any relation with Kellton tech? Are their any other group companies? -

What synergy or value add or capabilities have the acquisitions brought in? Are they just to acquire more customers or do these acquisitions bring in specific skills that were missing?

-

More details on margins, EPS accretiveness, funding of acquisitions, etc,.?

-

More details on nature of work i.e. run of the mill work or say any niche, etc,.?

-

Views on dilution (past, present, future)?

-

Basic note on financials and/or valuations?

Also, I think expected topline of 600 Crs is by FY16 (I just glanced through a news item headline on moneycontrol on Kellton’s page).

I had a look at Rs.30, but gave it a pass as wasn’t able to find many answers and didn’t understand the differentiating factors etc,. very well.

Making the suggestion in the spirit of admin’s (@adminph2) and moderator’s focus on presenting a balanced view, as the starting post doesn’t give much information.

Kind Regards.

Kellton Tech – Fast growing IT guy in ISMAC space (30-11-2015)

-

This is in my watchlist for sometime but didn’t make any entry as I’m still trying to figure out what is USP for Kellton? Now-a-days every company whether it is microcap or large cap, everybody is adding a fancy line of SMAC / iot to their tagline. How can Kellton sustain this growth & margins with cut-throat competition out there ?

-

Their mobility platform / solution – Need to find out how many customers use it.

Kellton Tech – Fast growing IT guy in ISMAC space (30-11-2015)

Cambridge Tech is a 35 pe microcap (mcap 190 odd crore). I consider it a crazy valuation for a microcap; not surprised by the recent fall in its share price.

8k miles is growing at 100% run rate, has fantastic margin, but is available at 70 pe odd. Its AR looks superb. But haven’t studied it much because of its super valuation.

Kellton Tech is expected to grow fast, is not a microcap, is available at a decent valuation, that is what attracted me.

As far as SMAC is concerned, the whole world is moving towards it, and I find it good for early entrant like 8K/Cambridge/Kellton.

Suven Life Sciences – Embedded triggers (30-11-2015)

Can somebody tell me how much does it averagely takes for the molecule to reach from Phase 2 Clinical trials to the FDA approval. I checked Cadila’s website for Lipaglyn Development(for Indian markets) after Phase 2 Clinical trials it took them 5 years to get the final approval. Can somebody guide me?

Here is the link for Lipaglyn

http://lipaglyn.com/key_milestones.html

Disc- I am Invested in Cadila and it forms 10% of my portfolio.

Not Invested in Suven as I see it a jackpot which might or might not hit.