I think it could range between 10-15 PE if its showing good growth which it is currently doing.

It could go up to 20 PE if there is roaring bull market or if there is froth in the counter.

I think it could range between 10-15 PE if its showing good growth which it is currently doing.

It could go up to 20 PE if there is roaring bull market or if there is froth in the counter.

Pratik one doubt, please help to resolve –

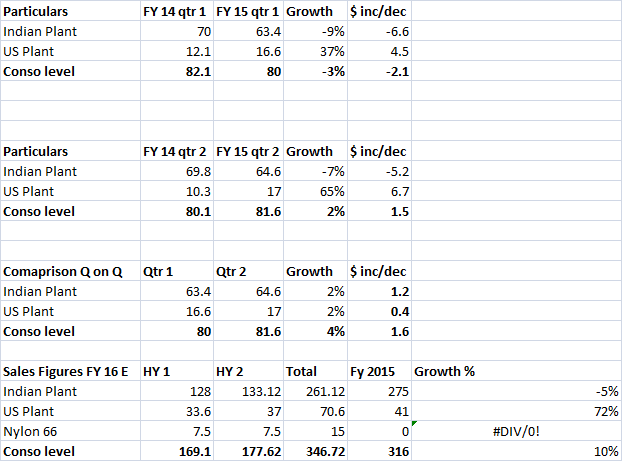

1). volume grew by 4% Y-o-Y – As per my understanding this should be at the consolidated level.

2). GP margins increased from 50% to 60%(approx) – this means that the decrease in raw material prices has not been passed out to the clients, If this is true then, the Indian sales might have been shifted to US sales and the volume growth might be just because of sales of Nylon 66. It can be also that the crude benefit might be bigger than 10% (around 15%) and 5% has been passed back to clients. In this case then, the Indian sales might not be shifting to US plant.

Once again, an education stock seems to be getting caught up in corporate mis-governance. Like real estate, it seems this sector is filled with landmines which you can walk around for a while but will eventually end up blowing yourself. I dont mean to generalize but after so many corporate misdemeanours in the education sector, it seems like this one was inevitable.

On the face of it, the company looks like a fantastic buy at this price. It seems to be growing rapidly, taking the right steps by trying to sell off assets like the land and building in Baroda and sweating preschool assets by adding day care services. However, the primary question that needs to be answered is about the integrity of the promoters. If there is no problem with that, at this price, the company is a no-brainer. With all the questions being raised about change of company secretary, change in CFO, change in auditors, receivables, possible fund diversion, incessant pledging for reasons not known yet, it is better to stay out and wait for the dust to settle for clarity to emerge.

The best thing for minority shareholders will be for the promoter to come out and explain the current situation and particularly bring some transparency as to the deployment of the 140 crore capital being used to buy rights to manage K-12 schools. Although, it is the personal right of the promoter to do whatever he wants with the capital that he raised through pledging, I think it will also be very helpful for him to clarify how he has used those funds to answer the question as to why there is so much pledging. Bringing a big 4 auditor will definitely help as well as it will give confidence to investors that the numbers are verified and real.

@Anindya, You are correct

The fall has been truly spectacular both in magnitude and in duration. Any contrarians out there? Care to explain the thesis if you’re contrarian and willing to go long / chase the price?

Disc: no position

(post withdrawn by author, will be automatically deleted in 24 hours unless flagged)

@abhishek90

The fall in RM prices is mainly the reason for decline in the standalone/consolidated sales at the nominal level.

The real growth do exists through volume growth of 3-4% (not commendable though  ) but Sarla’s focus on value added product is a plus point.

) but Sarla’s focus on value added product is a plus point.

Plz correct me, if I’m wrong!

Sarla Performance Fibre was presented award at Karur Vyasa Bank – Dun & Bradstreet SME Business Excellence award under “Mid Corporate” segment in Textile category at the hands of Mr. Jayant Sinha – MoS Finance. I watched it on CNBC TV yesterday night. The news is here. But it does not spell out list of awardees

http://www.thehindubusinessline.com/money-and-banking/kvbdnb-awards-for-smes/article7919898.ece

Disc : created tracking position

Can someone help me to know more about suppliers of Atul auto for all variants of its passenger and cargo vehicles ??

Today’s news

Modi to launch solar alliance on first day of Paris climate summit