Dear manish962

i have not read this line in the post

“from here on we may expect it to double by end Sept.2016”

and if this is repeated in other threads posts also then its not a healthy practice and must be stopped .

Posts tagged Value Pickr

Cupid Ltd – Helping the world play safe! (22-11-2015)

VP CHINTAN BAITHAK GOA 2015: Ananth Shenoy: GENERICS PHARMA PIPELINE BASICS (22-11-2015)

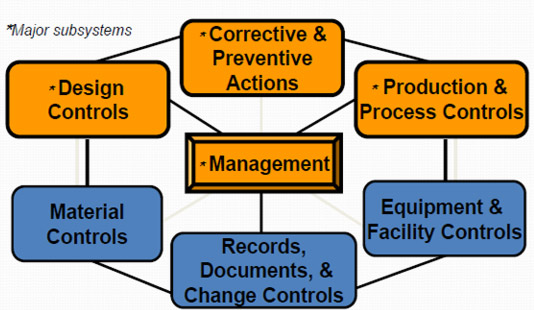

Found an excellent summary of the FDA inspection process.

Recommend to visit the source URL for complete read.

http://www.metricstream.com/insights/FDA-inspections.htm

I have collected the important snippets for reference –

WHO DOES THE FDA INSPECT AND HOW OFTEN?

The Food, Drug, and Cosmetic (FD&C) Act gives FDA the authority to conduct inspections at drug and medical device manufacturing facilities, among other regulated types of facilities. The FDA selects companies to be inspected primarily based on risk . Those companies manufacturing drugs and higher risk devices, top the list. Thus, manufacturers of class III devices, sterile drugs, prescription drugs, newly registered facilities, implantable, life-supporting, and life-sustaining devices, are the primary subjects for inspection.

Facilities having historical significant violations, are also FDA inspected.

For pharmaceuticals and the risk based inspection system, FDA focuses on three types of facilities: sterile drug product manufacturers, those that produce other prescription drugs; newly registered facilities that had not been inspected previously ,and focuses on 3 factor categories: Quality and Product Safety; Facility; Process.

As per the Federal Food, Drug, and Cosmetics (FD&C) Act, domestic drug establishments, and Class II and Class III device manufacturers are to be inspected every two years (surveillance). Foreign manufacturers were inspected on an average of every 9 years. However, due to FDA’s budget increase, an increase in manufacturing plant inspections (domestic and international) has resulted. This budget increase is equipping the FDA to add staff and open international offices in major countries . Consequently, foreign inspections, do not have an every 9 year average anymore.

Inspections are also conducted prior to a company acquiring Premarket Approval Application (PMA) and New Drug Application (NDA) approvals, as well as Biologics License Application (BLA) licensing.

FDA QUALITY SYSTEM INSPECTION TECHNIQUE

FDA uses the Quality System Inspection Technique (QSIT) for its inspections. QSIT is based on a top-down approach to inspecting a manufacturer’s QS. The technique provides different inspectional levels based on reason for inspection.

In the medical devices industry, QSIT is used by the FDA to assess the firm’s QS for compliance with the appropriate regulations and for inspection of domestic and foreign manufactures of medical devices intended for commercial distribution in the United States.

The inspection will assess the firm’s systems, methods, and procedures to ensure that the firm’s quality management system is effectively established and maintained. The QS inspection should include the assessment of post-market information on distributed devices.

QSIT Devices Overview

The manner in which QSIT relates to the Pharmaceutical Industry, is through the guidance document: “Quality Systems Approach to Pharmaceutical Current Good Manufacturing Practice Regulations”. This guidance document defines requirements for all aspects of a firm’s quality structure. Firms that comply with the expectations of both 21 CFR Part 210/211 and QSIT, are aligned to the expectations of the referred guidance.

The Center for Drug Evaluation and Research (CDER) defines and groups QSIT into six major systems which consists of:

THE INSPECTION PROCESS IN A NUTSHELL

Here is what happens on the day of an FDA inspection:

• Receptionist activates the designated alert system.

• Company Inspection Team members go into their roles and designated areas.

• FDA provides the company with Form 482 and identification.

• At opening meeting, FDA explains why they are at your site.

• After a facility tour, the FDA inspection team, requests documents and begin to conduct interviews.

• FDA conducts the Exit Inspection Meeting.

• Findings are reviewed and description provided of any violations/deficiencies from current regulations, deviations from company’s own procedures and further clarification of misunderstandings can be addressed.

• FDA presents Notice of Observations (Form 483) to management and executive management present at exit meeting with annotations (the latter, if both parties agreed to annotations). The 483 lists inspectional observations. However, it does not represent a final Agency determination regarding your compliance.

• Upon return to local District Office, FDA investigator:

o Writes an Establishment Inspection Report (EIR) (normally, they begin writing it right at the firm’s site)

o Forwards report to headquarters and the Agency classifies the inspection

o After headquarter evaluates, you may receive a Warning Letter

WARNING LETTERS

If the inspection has an Official Action Indicated(OAI) classification, the FDA will send a warning letter to the company, describing the manufacturer’s violations of FDA regulations and requesting a reply, usually, within 15 working days after receipt of the letter. In such a case, the company will need to reply using the same format as the 483 response, and including documented evidence of corrective actions.

Usually , FDA conducts a follow-up inspection to verify that the appropriate corrections have been implemented and *are effective.

After the FDA has completed an evaluation of corrective actions via follow-up inspection, it may issue a clo*se-out letter.A FEW BEST PRACTICES FOR SMOOTH FDA INSPECTIONS

Companies can ensure a smooth inspection process by following a few best practices:

• Have adequately trained resources with relevant expertise and accountability.

• Get upper management’s support on compliance and quality programs.

• Don’t underestimate the value of an independent regulatory compliance team and an expert quality assurance team.

• Make sure you have implemented the commitments made from previous inspection.

• Understand your potential quality data sources.

• Implement and assess an effective QS.

• Invest time, designate accountable resources.

• Ensure there is a designated company Inspection Team.

• Ensure proper documentation and records.

• Maintain effective Management Review and CAPA systems.

• Identify true root causes of issues using appropriate problem solving tools.

• In-bed in organizational culture, proactiveness.

• Understand when a product, or quality issue is significant.

• Have defined metric systems to monitor your QS in order to identify trends, gaps, and opportunities.

LEVERAGING TECHNOLOGY TO PREPARE FOR FDA INSPECTIONS

Both for 483s and warning letters, you will need to:

• Put together a project management team and assign accountability.

• Use change and document control systems, CAPAs and other quality systems to implement and monitor the changes needed and to sustain them.

Lycos internet – way to digitalization (22-11-2015)

profit and all is fine if people have confidence on numbers. market perception could be negative also because of relatively complex business. have heard rumours about management being opaque with numbers etc. whats your view on that

Associated alcholols & breweries ltd (22-11-2015)

After seeing the half yearly result there is following points

For growth

3 year sales / profit growth > 7 yr sales / profit growth this will show that a longer period time the growth is sustainable and there is no negative growth in 7 years

For returns

Average ROE 3yr > 12 and TTM ROE > 17%

AVERAGE ROA 3yr = 10 and TTM ROA > 13.5%

For capital

Average ROCE 3 yr > 11.5% and TTM ROCE > 16%

ROIC > 18%

Days receivable in outstanding < 40

Inventory days < 40

Current ratio > 1

Debt management

Debt< Debt 3 yrs back DER < 0.7 Z SCORE > 2.9

Capex growth

Net block > Net block 3yrs

Promoter

Holding increased in last 3 yrs by open market > 5.5

No dilution no bonus no pending warrant no preference capital

Sector

Has problems with government but potential to grow

Promoter quality

Not fully known but no history of non compliance no pending investor compliant and dividend started

No web site

Now as regards the remuneration part I feel that the three people put together that is Prasanna Kumar Sushil Kumar and Ashish Gadia are taking a major chunk nearly > 60%

But the good thing is they have declared it in the PL and even after huge employee cost they are able to show adecent profit in the Pl the cash flow has improved the loan and advance is reduced

The bank grantee of 30 cry to third party has to be understood

And finally as regards the investment made by them in Narmada distillery and Mount Everest has to be clarified

Finally as retail investors we should understand that when HNI like Ayush Anil Kumar Goel dolly Khanna make some investment there financial capacity to hold there ability to cut losses there timing and long term view above all there temperament is different from retail investors

As retail investors we shoul thank them for sharing there perspective on a particular company

Now by fy 17 we can finally say that this is a valuable find if same growth is maintained and promoter clarity comes that I think Ayush has nicely summed up as work in progress watch it for growth and any dieviation

Thank you

Varun 2020 portfolio – 2 strategies (22-11-2015)

Finally started flirting with Camlin Fine sciences and Kitex Garments.

Will look to turn either of them into investments in next 2 days as after that I am going for short vacation to Singapore.

Will invite your views on above stocks. Even Elgi equipments started to look interesting.

Varun 2020 portfolio – 2 strategies (22-11-2015)

Hi

Portfolio Update

Due to some finance requirements have to part away with few stocks like Rallis India, NRB bearings and Gati. While the first two have given very good returns with NRB clocking over 200% the same wasn’t the story with Gati. Exited Gati with some loss.

In the meanwhile have steadily increased allocation to few stocks in downturns

Axis Bank

Marico

Atul Auto – On Diwali Day

Have reduced some positions in

KPIT at 166 and Care at 1300 to finance above increased allocation

Happy Investing

Diversified Portfolio with growth target of 18-20% CAGR (22-11-2015)

Hi All,

Thanks for few suggestions.

I can understand that, ValuePickr forum mainly looks for small caps and mid caps which can generate 20-25-30% CAGR on annual basis. Reason for having large caps in my portfolio is to protect the downside considering that I do not have very long time frame for my financial goals.

Also, I have learnt in the past that, even such a large cap oriented portfolio can give returns of up to 25% CAGR if stocks were bought when undervalued and sold when get overvalued. I have always followed a stringent process for this and it has worked quite well.

Reason for TCS being high in portfolio is due to investments since IPO days, and comfort with the management, vision and ability to grow in tough conditions. Also, I understand that, now onwards it will not give me 20% CAGR returns hence have reduced it from 25% to about 14%, and may reduce it further. TCS is a high ROE/ROCE business with good cash flows and good dividend yield.

Mutual Funds can generate returns close to this, but I do not have control on the portfolio, and they keep holding overvalued stocks for a long time. I have more control on the portfolio and can follow my own style of investing. I do have separate MF portfolio.

I am slowly learning the art of identifying small caps which can give 25% CAGR returns and hence there are some quality small caps in the portfolio now. Due to tendency of not overpaying for some of the quality names I do not have Page, Gruh, Repco, Ajanta in the portfolio.

Rajoo Engineers Ltd – Mfg of Plastic Extrusion Machinery (22-11-2015)

ICRA has upgraded the long term rating assigned to the Rs. 19.50 crore*

cash credit facility of Rajoo Engineers Ltd (REL)† from [ICRA]BBB- (pronounced ICRA triple B minus) to [ICRA]BBB+ (pronounced ICRA triple B plus). ICRA has also upgraded short term rating assigned to the Rs. 16.50 crore short term fund based facility (sublimit of cash credit facility) of REL from [ICRA]A3 (pronounced ICRA A

three) to [ICRA]A2 (pronounced ICRA A two). The outlook on the long term rating is ‘Stable’.

The upgrade in ratings reflect the continued improvement in the performance of the company as witnessed from steady growth in scale of operations in last two fiscals supported by healthy order book, improved profitability and return indicators, moderation of capital structure and healthy coverage indicators. ICRA notes that the improvement in the financial risk profile had been largely on account of discontinuance of relatively low value additive segments (non woven fabric manufacturing machine and polymer trading). The ratings continue to favorably take into account the longstanding experience of the promoters in the plastic extrusion machinery, and the favorable demand outlook for flexible packaging products in the domestic market. The ratings are also supported by the company’s wide ranging product portfolio and its competitive advantage arising from technological tie-ups with the international entities providing access to the latest technology.

The ratings are, however, constrained by the exposure of company’s profitability to any adverse fluctuations in foreign exchange rates and volatility in raw material prices; however natural hedge provided through import of raw material mitigates the currency fluctuation risk to a certain extent. The ratings also consider the increasing competitive pressures both from organized and unorganized players in the domestic market and import threat from Germany, Italy and China as well as the regulatory risks attached with the ban on plastic packaging.

Company Profile

Incorporated in 1986, Rajoo Engineers Limited (REL), promoted by Mr. C.N. Doshi and Mr. R.N. Doshi, is engaged in manufacturing of plastic extrusion machinery at its plant located at Rajkot, Gujarat. The machinery finds application in the flexible packaging industry. The company designs and manufactures the machines and offers customized solutions as per customers’ requirement. Its current product portfolio includes a wide range of extrusion machinery consisting of mono and multilayer blown film lines, sheet extrusion lines, thermoforming machines, non-woven fabric machines, Polyvinyl

Chloride (PVC) pipeline machines, drip irrigation machines and wooden plastic composite (WPC) machines which can process a wide range of polymers.

Recent Results

For the year ended 31st March 2015, REL has reported an operating income of Rs. 116.67 crore and profit after tax (PAT) of Rs. 5.25 crore as against an operating income of Rs. 101.62 crore and PAT of Rs. 3.46 crore for the year ended 31st March 2014. Further REL has reported operating income of Rs. 19.81 crore and PAT of Rs. 0.90 crore during the period from April 15 to June 15 (unaudited provisional financials).

http://icra.in/Files/Reports/Rationale/Rajoo%20Engineers-R-05102015.pdf

Ajanta Pharma (22-11-2015)

Hello Sandeep,

Thank you for your reply and sorry, I did not form my question well !!

Sometime back u posted below content ~~~

It’s heartening to see Ajanta gaining market share in Risperidone in the US market.

Source: https://pbs.twimg.com/media/CJm1APEUAAEA4fZ.png:large

Risperidone is a crowded place too; 12-13% market share is quite an achievement. Not clear to me if it is through Breckenridge Pharmaceuticals or through its own front-end sales and marketing team in the US.

So how to know the market share information for a particular drug in US ??

Thank You

Nabendu

Ajanta Pharma (22-11-2015)

Hi Nabendu,

Unforunately, no public source AFAIK. IMS Health tracks prescription/OTC sales and derives market share data (for a particular drug); information is behind paywall.

At times, IMS data may not portray full picture. e.g. snippet of Torrent Pharma Q2FY16 transcript

{kind=link}

Source: http://www.torrentpharma.com/download/financials/gen_info/Transcript-Q2-FY-16.pdf