US opposes India’s latest round of incentives to boost textile exports

NEW DELHI: The United States has opposed India’s latest round of incentives to provide a fillip to exports, alleging violation of a global trade rule for export competitiveness in textiles.

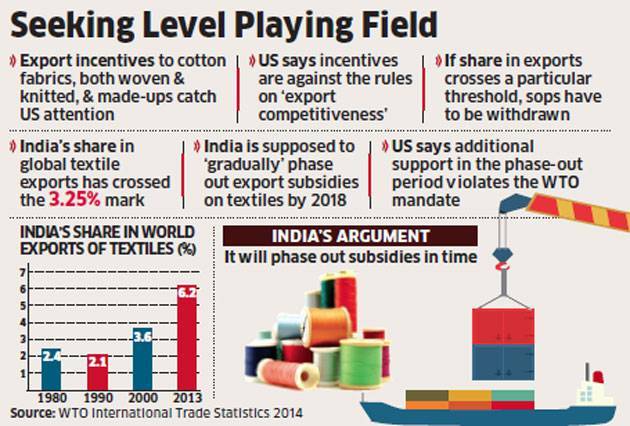

Commerce department officials said the US raised this issue more than a week ago, after India increased support for exports of several products including textiles while expanding the scope of the Merchandise Exports from India Scheme (MEIS) on October 30.

The government included exports of cotton fabrics, both woven and knitted, and made-ups to leading markets including African countries under the MEIS. Under the World Trade Organisation’s agreement on subsidies and countervailing measures, when the export share of a developing country with per capita income below $1,000 a year touches 3.25% in any product category for two consecutive calendar years it is deemed to have gained “export competitiveness”.

Such a country is then required to phase out export subsidies for the items for eight years from the second year of breach. The WTO mandates developing countries to phase out the export subsidies within the eight-year period, preferably in a progressive manner. The WTO had in 2010 asked India to consider phasing out the subsidies for textiles and clothing.

“However, a developing country member shall not increase the level of its export subsidies, and shall eliminate them within a period shorter…when the use of such export subsidies is inconsistent with its development needs,” the agreement says.

The US has flagged the issue of export competitiveness in textiles and said that India cannot give additional subsidy during the phase-out period, said an official, requesting not to be identified. Another official, in the Cotton Textiles Export Promotion Council, said India has crossed the export limit and the government is aware of this but the market is moving slow.

“As for the removal of subsidies, we can either gradually phase them out or immediately stop them in 2018 on a pre-decided date,” he said.

What will be likely impact of this on Ambika??