@ Dwanil…..super good job indeed….ur analysis and the attention to detail is really praiseworthy.

I just have one question( pardon me if its too naive)….Is there any clarity on the licence renewal fees of the frequencies awarded in phase I and II?

If yes, How much are these companies expected to shell out for the renewals?

Thanks!!!

Posts tagged Value Pickr

Entertainment Network India Limited (ENIL) (21-11-2015)

Panyam Cements & Mineral Industries Ltd – turnaround taking roots? (21-11-2015)

Vinay,

While it may make sense in valuation, I would still ask to you to check same at operational efficiency and management paramter. In my opinion, a fake note of 10 and 1000 are both valued as waste paper unless we find a greater fool. While the Telengana region is expected to show demand improvement, not sure whether the company has any brand in market. Also, it would be critical to see local demand supply situation. Typical cement capacity are at least in 1 mn to be MES (with recent one are more in range of 2 mn tpa), against which the production of the company is 0.5 mn tpa which may be very close to mini cement.

Not seen valuation in EV/Tonne (Ambuja Etc are traded at around USD 170-200/ tonne EV), so the better way to calculate EV/tonne for the capacity. May also look at Dalmia Bharat and other mid size players to get more understanding.

Your thread was worth reading and points were very well highlighted (as usual, I can say because seen your work/note for almost decade now !)

Discl: I hold shares of Heidelberg Cement and my view may be biased.

Shree Hari Chemicals – Get 18cr Cash & Business for free (21-11-2015)

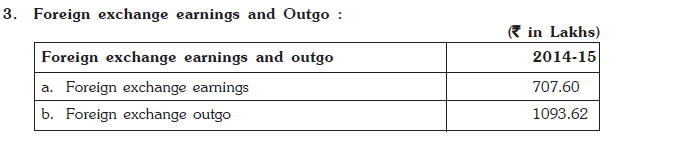

While studying the AR 2014-15, I came across following

Being exporter, I thought their forex earnings would be much higher than outgo, can somebody throw light on this disconnect?

Disc : not invested but started looking at it

Shree Hari Chemicals – Get 18cr Cash & Business for free (21-11-2015)

I entered at 91, received dividend. I assumed Q2 will be poor due to factory closure issue hence exited at 110. Post Q2 result – stock nose dived and I re-entered at CMP

Entertainment Network India Limited (ENIL) (21-11-2015)

Thanks Dhwanil for the additional docs and the nice Investment Note.

I had a quick look through to first familiarise myself with the terrain quickly.

Following are top-of-mind very basic questions as of now, which you can help me understand better/quicker

-

I am yet to place a finger (from all the Notes) – what is/are the Key Success Factors for success in the radio business – among the few Top players? What is it on the ground that ENIL does better (it obviously has done much better than nearest competition) that makes them stand apart among teh top players?

-

If they are known, why aren’t others able to replicate the same, or unwilling to do the same, or execution-wise very difficult to do – requiring a different mind-set (different business models for e.g as in commodity yarn vs Ambika yarn, or extensive field-work being the decisive tilting factor in case of an Avanti or Kaveri that others just aren’t upto) – just what is the secret sauce

We usually want to be able to articulate that fairly well for businesses where we have done extensive work on.

-

What are the 6 cities where ENIL Pricing is at a discount to Competition. How much is the discount and to who all – the leading player, or it lags a few?

-

Pricing power is a function of?? – pardon me for trying to get this off you

-

What are the components of its Marketing/Brand-building spend? Why is Marketing Expense not a variable expense in line with Revenue growth? I read somewhere it being clubbed under Fixed Expenses

-

Risks as enumerated by you look Low probability. In order to understand Risks at a more granular level – are there any critical must-get cities/must-get renewals in phase III or Renewals? Like some Key-Metro licenses for Mobile Operators used to queer the pitch? Has ENIL lost out on any such key must-have cities/locations so far?

Will start doing the basic reading up on domain/ENIL specific business.

Shree Hari Chemicals – Get 18cr Cash & Business for free (21-11-2015)

I used to be in this stock with a small allocation for all the above reasons but the the nosedive, following the Maharashtra pollution board’s closure notice in June scared me. My attempts to reach the management and get a possible resolution date was of no avail. Manufacturing restarted in July but I had exited by then.

Indocount notes from AR (21-11-2015)

Recently bumped against Indocount and came to know about it’s growth story, after digging a little more I found the entire cotton spinning/textile industry boomed explosively in last year and half. I see nice bit of data here but I had a couple of questions which I find no one explains properly:

1) What changes in demand or supply or production or pricing brought in such a magical surge that it flew from Rs10 to Rs1000 in less than 2 years.

2) And more importantly will that kind of growth be sustainable, is there any reason to expect it to be Rs 20k or Rs30 per share in two more years. Maybe we can understand all that if we understand the reason of such an explosive growth and how much untapped growth opportunity is still open.

Shree Hari Chemicals – Get 18cr Cash & Business for free (21-11-2015)

Dear ValuePickrs,

This is my first post + 3 months investing experience – so may not b able to answer your queries (but will try as much as possible)

First of all humble gratitude to Prof. Sanjay Bakshi – who has taught so many students (actively or through his blog). Got interested in equity investment after reading his post on – Seven Intelligent Fanatics From India.

Shree Hari Chemicals

Listed in 1992 by ex-Birla guy (K.LRamuka – no public info about Ramuka)

Market Cap – 36cr

Cash in Hand – 35.5 cr

No debt (short term or long term)

Total Shares – 44 lakhs

Promoter Holding ~ 48% (promoters were buying from open market few months back)

Public Holding ~ 52%

get a loan of 18cr become majority share holder and get access to 35cr cash + business

repay back your loan of 18cr with 35cr cash (net net – u will get access to 18cr + business for free  – I am aware this is unlikely to happen – just thinking aloud)

– I am aware this is unlikely to happen – just thinking aloud)

About Product

Manufactures – H-Acid (80% contribution to revenues) – used as an intermediary product in Dye-Chem industry – commodity product – exported to multiple countries

Competition – China / Local Manufacturers

Pricing – v.competitive with China (as per mgmt – during my call 1-2 months back)

Balance Sheet

No Debt

Cash in Hand ~ 35.5cr

Account Receivable (13.75cr) ~= Account Payable (10.4cr) – if not zero / negative (Buffet’s float money) – net account receivables is v.low

P&L

growth in earnings observed in past couple of years – mainly due to China factories were closed down – pollution issue. Highly regulated industry by Pollution board. Even Shree Hari factory was closed in Mar’13 compete financial year and approx 1 month in Q2FY16. Company reported a loss in Q2FY16 – i guess mainly for 2 reasons

1. Factory was closed – hence sales dip

2. Bureaucrat expense – to get the factory operational (though I guess Pollution norms must have been met – after Mar’13 issue – just guessing)

High Margins – in spite of low cost manufacturer

High ROE – due to low equity base

High ROCE

cash rich

Disc – Invested – tracking state

Arvind infrastructure: Godrej Properties in the making? (21-11-2015)

One think I want you to know about how property markets operate in india.

Yes i am optimistic about the prospects of the company but Dont go by the bookings.

My freind have recently money to a reputed developer in NCR. As a security a villa is booked in his name in case builder defaults.

Also some booking are done by property dealers. About 25 % of initial inventory is sold this way. And here also as I can see about 25% of project is sold. So wait for some clarity to emerge.

I know about it as I invested about 3 months as I want to buy a house in delhi ncr but the trend is applicable throhghout india.

Panyam Cements & Mineral Industries Ltd – turnaround taking roots? (21-11-2015)

Panyam Cement as a stock investment idea came from came from AceInvestorTrader blog (link at the end). Coincidentally, SP Tulsian recommended it in the last few days (as I was compiling this post) and there was a management interview also (links provided below).

Date – 21.11.15

CMP – 79.65

Mcap – 128 cr

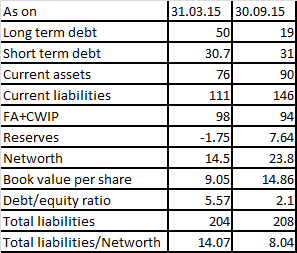

Book value – 14.9 (as on 30.09.15)

Enterprise value – 175 cr (Mcap plus total debt less cash, as on 30.09.15)

Basically, it’s a turnaround case. The plant was shut in Nov 2013 due to lack of power and was restarted only on 21.07.14. Sales and profits since then are showing some signs of improving.

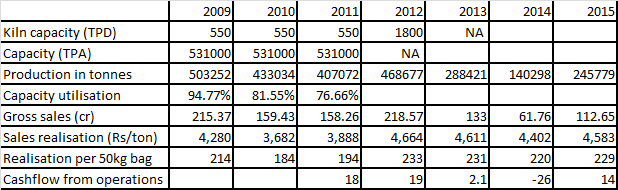

Its current capacity is not exactly known, however, they commissioned an enhancement in capacity from 550TPD in Kiln 1 to 1800TPD on 10.08.2011. The company reported capacity of 5.31 lakh tons per annum in their 2011 annual report (when their Kiln 1 capacity was 550 TPD), however stopped reporting the capacity thereafter. In any case, they haven’t been able to make full use of their capacity for one reason or the other.

The owners are part of Nandi group and I had read earlier that they had political affiliations. The MD however is an IIM Ahmedabad graduate and is said to be running the company professionally.

The company is based in Telangana region which is expected to witness very high demand given the planned infra development activities (there are several new bits regarding how this region is expected to attract lot of demand, so this bit seems plausible). In addition, it also sells in neighbouring states like Goa, Karnataka. It has access to limestone mines close to the plant.

Following information is compiled to indicate that turnaround is taking roots:

Point 1:

Reduction in debt and debt equity ratio is positive. Though it is still high at above 2x. Total liabilities to networth is uncomfortable

Accretion to reserves is also positive.

Current assets have reduced (ex cash), and current liabilities (ex short term debt) have increased, which taken with profits, reduction in debt and depreciation, shows cashflows are improving.

They had 25 cr of CWIP as on 31.03.15, which seems to have come down to 20 cr as of Sep’15 which indicates some capex is on – either balancing equipment or debottlenecking or some such. 2015 annual report had a figure of 4 cr under Estimated contracts remaining to be executed under capital account (Rs 6 cr as on 31.03.14).

Point 2:

Pledged shares are down a lot and promoters are slowly buying shares from market (albeit marginal). There was one internet link which had compiled information (it was a paid site) for potential acquirers. However, acquisition (ie promoter selling out) is not a part of my thesis yet.

Historical data:

Some historical financial and production data:

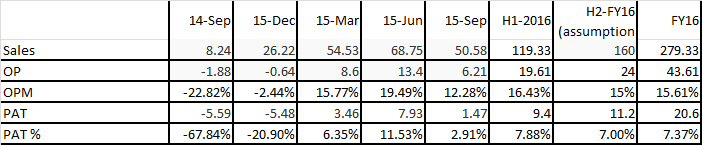

Recent Quarterly trends:

Some recent Quarterly data, which indicates improvement in financials:

Management says they will achieve 160 cr sales in H2-FY16 compared to 120 cr in H1-FY16, which looks possible.

They say that they will produce total 8 lakh tons in FY16, which works out to approx. 175 Rs per 50 kg bag, which considering current prices of anywhere from 250-300 Rs per bag, looks conservative and achievable.

They also say margins would remain in line with 1st half of the year. Assuming margins as given in the table, expected net profit in FY16 is around 20 cr, and current market cap is 128 cr.

Some Negatives in financials:

There are huge statutory liabilities under dispute shown as contingent liabilities (eg. IT claims of 42cr, Excise claims of 11 cr, Royalty delays penalty 13 cr etc). If these become payable, then the company would be bankrupt.

There is a component of interest received of 5 cr in 2015 (4.3 cr in 2014) which is included in the profits. Sustainability (genuineness?) of this is unknown.

The company had taken unsecured loan from promoter of 35cr in 2014 (the amount as on 31.03.14 was 41 cr) which came down to 30 cr as on 31.03.15. Why are promoters taking out money, when it could have been used to repay more debt.

Significant related party dues within the group – eg. 60 cr given to associate company as deposits/advances, corporate guarantee on behalf of group companies of 220 cr etc

These are significant figures, on which there is no clarity.

Concluding remarks:

I admit, this would appear as a leap of faith kind of stock.

It corrected 20-25% after Q2 results, which I was not very happy with, especially the profits. However later it struck me that Q2 is monsoon quarter, and in such a period, if they have done sales which is just 25% below the Q1 figure, then it is actually quite decent.

Given presence in Telangana, cement demand being especially good in 2nd half of the year, access to limestone mines close by, some bit of capex going on, reduction in debt, increase in promoter holding, reduction in pledged shares, near term prospects appear good. Part of it seems to already be in the price, but if they continue like this even in 2017, then it could really turn out to be cheap at this price. This would need close monitoring and hence current allocation cannot be high.

Disclosure:

Taken starter position at 60, added a bit recently. However it’s a very miniscule portion of my PF allocation as yet.

Links and other info:

http://www.moneycontrol.com/news/results-boardroom/h2fy16-to-see-higher-production-rs160cr-rev-growth-panyam_4212821.html

http://bullseye.in.com/video/stocks-views/positivepanyam-cements-target-rs-125-tulsian_4190881.html

http://www.panyamcements.com/panyam%20files/Annual%20Report%20Final-2014-15.pdf

http://www.sebi.gov.in/takeover/panyamloo.pdf

http://www.researchandmarkets.com/reports/2775378/panyam_cements_and_mineral_industries_ltd#rela0