The half yearly result has proven that company perform with consistency they are able to maintain opm above 12% reduced finance cost and debt even though small they are started paying dividend there is no reduction in promoter holding or pledge as of today the important thing is friends

See the SALES GROWTH IN 3 yrs > SALES GROWTH IN 7 yrs and PROFIT GROWTH IN 3 yrs > PROFIT GROWTH IN 7yrs and ROE > 15% and ROCE > 15% DER< 0.5 CURRENT RATIO> 1 NET BLOCK > NET BLOCK 3 yrs back the ROA> ROA 3 yrs back once DONALD explained this theory for Aarti drugs if I remember correctly but this fits this company very well now if they are able to maintain the historical topline growth of 30% even over next two years or assuming the growth at evn 10% we are talking about 370 cr Rev and at opm of around 12/13 EBITA of around 40/45 cr over fy/16/17 I attended the AGM in Kolkata they are decent guys but yet not aware of PRO hence awareness is lacking otherwise it is good they are able to explain about the growth prospects but not willing to dilvulge many details as to whether Mr ayush has bought or not it does not make a difference if the company fundamental is maintained the same way and top line improves than we can see some value generation in the share price

Posts tagged Value Pickr

Associated alcholols & breweries ltd (15-11-2015)

Avanti Feeds (14-11-2015)

Avanti Feeds Ltd has fixed November 27, 2015 as the Record Date for the purpose of ascertaining the entitlement of the members for sub-division of equity share of Rs. 10/- each into 5 equity shares of Rs. 2/- each.

http://www.equitybulls.com/admin/news2006/news_det.asp?id=173558

Stylam- Decent Fundamentals with Cheap Valuation (14-11-2015)

Their Balance sheet looks to be in a mess! Look at the increase in debt and receivables

Vidhi Dyestuff Management Meet (14-11-2015)

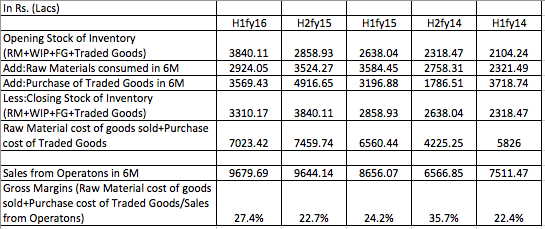

Results look bad prima facie but this was expected. The nos. do suggest drop of volumes in manufacturing business. May be the co. faced teething troubles with new capacity and it didn’t add anything to the quarter.

One respite is overall gross margins can be seen moving in the right direction,thanks to declining volume of trading business. I always had a doubt about trading business being loss making at worst and 2-3% margin business at best,data available on both lines of business leaves us inconclusive but following table can give a rough idea.

Disclosure-Invested.

Cranex Ltd : A Material Handling Company and a value buy (14-11-2015)

Results are out . Sales up 22% from 3.38 Cr of Q2 LY to 4.11 Crs this year.Co seems to be investing for the metro project scheduled for completion by Sep 2017 .EPS 0.1 vs 0.14 .

- Long term Borrowings increased to 14.17 Cr in Sep vs 7.72 Cr in Mar.

- Short term Borrowings increased to 5.48 Cr in Sep vs 1.65 Cr in Mar

- Trade Payables has decreased to 3.39 Cr in Sep vs 11.85 Cr in Mar

- Inventory moved up to 10.48 Cr in Sep vs 7.24 Cr in Mar

- Drs has come down to 11.14 Cr in Sep vs 13.44 Cr in Mar

- Cash in hand 4.7 Cr in Sep vs 8 Lac in March

Balance Sheet Size at 28 Crs (Rs.46 per share ) . Cash in hand equals current m’cap ! Land with current market value between 30-60 crs not priced in.

Vidhi Dyestuff Management Meet (14-11-2015)

Given the wide difference in profitability of trading ops (2-5% as per @desaidhwanil) and 20% on manufacturing why should PAT fall 14% if sales fell 18%.

La Opala RG – Aspirational consumer story (14-11-2015)

As expected stellar results from Laopala today, they contnue to grow as per management’s earlier interviews. They plan to grow by 25% or more on YoY & I see them doing much better. The sitarganj facility is starting day after tomorrow on 16.11.2015 & we may see its positive impacts as early as annual results. It has stood well in recent times despite major indices & markets having tough time… As results are better than expectations, I see LaOpala moving above 735 or above with little support from markets which is likely to stabilize or turn positive from current levels … Happy Investing

Stylam- Decent Fundamentals with Cheap Valuation (14-11-2015)

Decent numbers from Stylam

Disc: Invested

Abbott India: MNC pharma play on increased consumer spending (14-11-2015)

@m1hirk Hi Mihir

I too was looking into Abbott – Pediasure and came across this link. It claims the drink doesn’t have much nutritional value. (vs competitors.)

http://www.madhuriesingh.com/superindiankid/index.php/2012/pediasure-health-drink-supplement-is-not-for-every-one/

Digene seems to be a good product. Its widely used by doctors here in Kerala. It was prescribed along with a dose of antibiotics for me.

Thanks,

S

Disc: No shares owned.

Ajanta Pharma (14-11-2015)

As I said Amit I considered the impact but in my opinion it felt as a tall order but is not impossible.