there’s a lot happening on social media and this subsidiary financials auditor’s note is the latest after Q2 results

Posts tagged Value Pickr

Page industries (09-11-2015)

Hi S Das, I agree with you. Tho riche’s head and shoulder and a target of 10000 was interesting and scary. And he maybe right. But the kids wear and the online portal should be the next drivers. As fr the online sales, I am a bit curious. Will these bring offline sales online? Page has abt 30,000 points of sale. Would online complement offline sales, which means growth in revenue+online revenue? India has a low broadband penetration, i think abt 20% as compared to S Korea or Japan with more than 70%. And the overall scenario says 40% of all retail sales wld be online by 2020. Just to give an example, Maggi was back today, sold online thru snapdeal.

Chembond Chemicals- A Perfect Misvalued Bet (09-11-2015)

This was mentioned somewhere in their website or through their concall.

Direct competition would be companies as Omkar, Gulshan Polyols, Grauer etc

Disc: Invested

Page industries (09-11-2015)

If i not wrong page management had already told some analyst about a slower Q2. they also said things will be normal from Q3 onwards. though diff opinion makes a market i will wait for the earnings to catch as its difficult to find a stock like page with 20%+ growth and nearly 45% dividend payout ratio for 3-4 years to come. I feel market will always give page some premium i.e some more pe multiple for every quarter dividend policy and increasing dividend every year. its very difficult to find such stock and if we are lucky will get one or two in many years. Needless to say i hold page shares.

Excel Industries : Experience Certanity (09-11-2015)

Bad Sep results, company seems to suffer due to lower sales affecting operating leverage.

However one positive, RM to sales ratio is same and the affect has been from fixed costs only which has affected margins. Lower sales could be due to lower agrochemicals demand in the last quarter, hopefully should improve in the next quarter results.

Today’s drop seems to be a good opportunity to buy.

Discl: Invested at CMP

Avanti Feeds (09-11-2015)

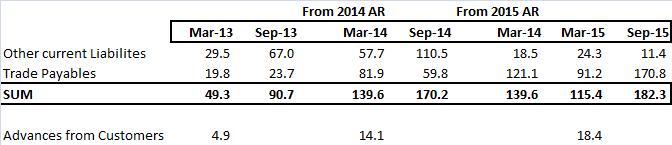

Till 1 hour ago, I was in @dkirand camp on this- This big decrease in Other current liabilities is sign a worry since most of this should be Advance from Customers. And we all know, a big decrease on that front is a big sign of worry.

However, after @ashwinidamani and @ayushmit explanation, my mind asked me- Now which camp are you in, Sir?

So, I decided to check the past trends of Other Current Liabilities, Trade Payables & Advance from Customers.

And the result is – There was Reclassification (from Other current Lia to Trade payables) in March-15 Annual Report.

i.e March 14 Balance sheet numbers were reclassified in 2015 AR.

So, Sept-14 & Sept-15 Other current liabilities are not like-to-like.

Full data below-

Have captured Mar-14 numbers from both the balance sheets – AR 14 & AR 15.

Page industries (09-11-2015)

Disclosure: I’m no way remotely can be called a technical analyst. But I usually see trends when I want to sell any of my core holdings. I hold page and I have trimmed it as disclosed in my portfolio thread earlier in order to make way for alpha returns and I intend to trim it further.

Page Industries 1 Year Daily chart

Chart source: Chartlink.com

- As indicated in one of my earlier posts above, Page though briefly breached the upper line it soon resumed its down trend and it looks it is headed towards touching the lower line at around 12000. However, currently the stock is in over sold levels (look at RSI and CCI indicators) so there could be some lower selling pressure before the downturn resumes towards 12000. It appears as if Page made a significant top at 17000 though on low volumes.

Page industries 5 year weekly chart

{kind=link}

- It looks like Page is forming “Head and Shoulders” pattern in the weekly 5 year chart and if the chart plays out the targets could be around 10000 which is the difference between neck line and head top. Any break down below 13000 on weekly close could proved to be negative. Since this is a weekly chart the targets also play accordingly on medium term. So if the above daily chart plays out, it paves way to weekly chart as well.

Fundamentally too, it looks like the high PE coupled with lower growth relatively as well as in comparison to its track record could mean PE compression.

Again my amateurish technical skills could be playing a confirmation bias here as my previous post played out as predicted when Page fell from 14500 to 13000 levels.

EDIT: I’m as bullish on the Page business prospects as ever. Business prospects are different from stock returns prospects. With back to back lower revenue growth my perspective on stock prospects have changed.

Page industries (09-11-2015)

Decent set of numbers in this environment. Even the dividend is consistently being increased. I too am in a dilemma. There are so many companies reporting massive degrowth in sales and/or profit. at least this one is showing some growth. The TTM PE is now 67. ( looks good compared to 90 plus PE it had a few months ago). that gives some comfort

discl: invested since 2010. no buy/sell in last one year.

Indian terrain—play on consumption (09-11-2015)

True.

Read in AB nuvo annual report that Madura is delivering 70% roce. Please let me know where can I get detailed balance sheet, profit and loss and cash flow of Madura garments. This would help to compare as to whats main difference and why is Indian terrain not able to get that ROCE or why is Madura garments getting that ROCE.

thanks for your valuable inputs.

Tasty Bites: A proxy play to India’s QSR industry (09-11-2015)

Hi Bhaumik – Please write to Kagome Japan and try your luck. Being a publicly listed company, they might be obligated to send if enough of us write in.

Anyway, stellar results from Tasty Bites – http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/E50EA6CF_42E2_40C1_BE43_86E6D535822D_152901.pdf

16% sales growth, 67% profit growth. On track to cross 50 rupees EPS for FY16.

Disc: Invested. No transactions for last 30 days.