One reason i see inc in profit is due to fall in power cost to sales Ratio.. Any update on that front

Debt has reduced from 295 cr to 159 in five years ( approx 100 cr )though in starting thread its written 359 cr..

.

One reason i see inc in profit is due to fall in power cost to sales Ratio.. Any update on that front

Debt has reduced from 295 cr to 159 in five years ( approx 100 cr )though in starting thread its written 359 cr..

.

I am not sure about the objective of the Buyback announced by the Management few days back. The

At the buyback price of 270 for 52.26 Lakhs shares, the outflow is Rs. 141 Crores.

I could think of the following reasons for the management to go in for the buy back:

The Management thinks that the share is undervalued in the market, and would like to bring up the market price to a fair value. (or)

The promoters need funds for meeting some personal commitments / investments. (or)

The company does not need any additional funds for expansion. Hence, by returning the idle funds to the share holders, RoE can be improved. (or)

The Promoters intend to participate in the buyback as well implies they want to take out the cash from the company. I believe the risks mentioned in my previous post seems to be realizing since management themselves don’t feel the room to expand or increase operational efficiencies.

Discl. Tracking position

Thanks hitesh for the reply. I am looking at db corp even though i feel growth will be atleast couple of years away

They have entered the baby-care market now with acquisition of more OTC brands :

I managed to attend conf call and below are my notes. My objective is to learn more about the business model. Disc: I hold a tracking position (2% of my PF).

Added result update presentation Q2 FY16 link

http://corporates.bseindia.com/xml-data/corpfiling/AttachHis/F38F8553_E867_4CF1_ABCB_D94584393C80_200608.pdf

Ethos: H1

41 stores: 8 summit stores, 3 duty free stores, 27 Ethos format stores, rest 3 could not capture ?

2 new stores in Mumbai:

Store at Ambience mall gurgaon – very good performance.

Same store sales growth 18%.

56% increase in online leads generation.

Expenses reduced from 13.5% to 12.6%.

Advertisement / Branding initiatives: half page ads in few newspapers

Trust campaign: increase consumer awareness, receiving positive feedback.

Brand recall of Ethos is strong now as compared to last 2 years.

Inventory carrying

H1 FY16: 8.6 months

H1 FY15: 9.3 months

New initiative:

Special section in shoppers stop for premium watches. Trial basis in Mumbai and Hyderabad. This is in line with global trend of premium watch location in departmental stores

Parent business:

1. How things are shaping up next 12-18 months ?

⦁ Expect to grow 10-12% per year

⦁ Hit a bit of speed breaker due to global soft conditions

⦁ Now an indicator of strength

⦁ Domestic demand turning up

⦁ Revival expected from Q4

⦁ 10-12% growth on watch components side

Precision business:

a. Electronics & Electricals

b. Aerospace & Defense – expect to improve

c. Auto

Expect growth from 25crs to 100 crs over next 3-4 years. Average growth 30% with earnings lumpiness.

Growth much better. Aggressive plans Precision stamp -> Precision moulding.

Capital raise 30 crs – funds for expansion. Capital expenditure – engineering side.

Land in aerospace development park in Bengalore. Some capex has already started.

Ethos business:

25% growth. Offline and online combination – depends on effective logistics

Next trigger: GST

Expand portfolio of brands and products

320 employee strength in Ethos.

Trend more on digital media.

Absolute spend -> advertisement / marketing 2.2% of Ethos sales.

Same store sales growth 1Q 16%, 2Q 19% 1H 18%.

Margin contraction: overall market business has been soft.

Overall 1H better than previous year.

EBITDA margins 5% last year to 8-10% next 3-4 years

Ethos Market Analysis:

Market growth single digit, we are growing 25%. Some competitors are bleeding and we are gaining market share. Online business share set to improve.

Number of leads are increasing.

High focus on leads conversion improvement.

Capex plan 25 crs next year. KDDL will invest more in Ethos. Will strengthen equity holding in Ethos.

Pressure point on the margins – due to higher discounts offered. Increase in discount 1% lead to drop in EBITDA margin by 1.2%. Higher than budgeted consumer discounts. 1% higher than what was budgeted.

Number of watch specialists 25

Implementing a program of watch specialists: deputing then to physical stores.

Visits to website: 17 lakhs as compared to 14 lakhs last year

Leads 33000, little bit lower than last year. Focusing on quality of leads.

Conversion rate 8.1% this year as compared to 4.5 % last year. Q3 seeing a big peak.

Club Ethos membership 99800

Service & Repair watch vertical (important vertical)

Online and integrate. Looking for robust platform.

Over next 4-5 years span, premium & luxury watches 30crs a year. Plan to capture 1/3rd of this.

Packaging business – assessing whether to continue or not

ROE estimates:

a. Ethos (KDDL retail business) next 3-4 years > 20%

b. KDDL manufacturing business – already > 20%

Do customers research before buying a watch ?

– Yes if it is expensive. Active dialogue with our information centre (> 30 people)

Rationalizing brands, how do we add a new brand ?

– Check high leads. People are enquiring. Global trend.

Luxury value – making brands rare – corporate strategy. Reduce point of sales.

Top 50% online sales (10-12 brands)

Visit website: watch articles and blog

Pushing brand knowledge

Brands are embracing more online presence

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/58D3F983_792D_461F_AC9D_694C2372A2E6_171743.pdf

Lumax results have been announced

Aah.. what a coincidence. I was busy watching the video when i was compiling this post and you raced me in posting the same video

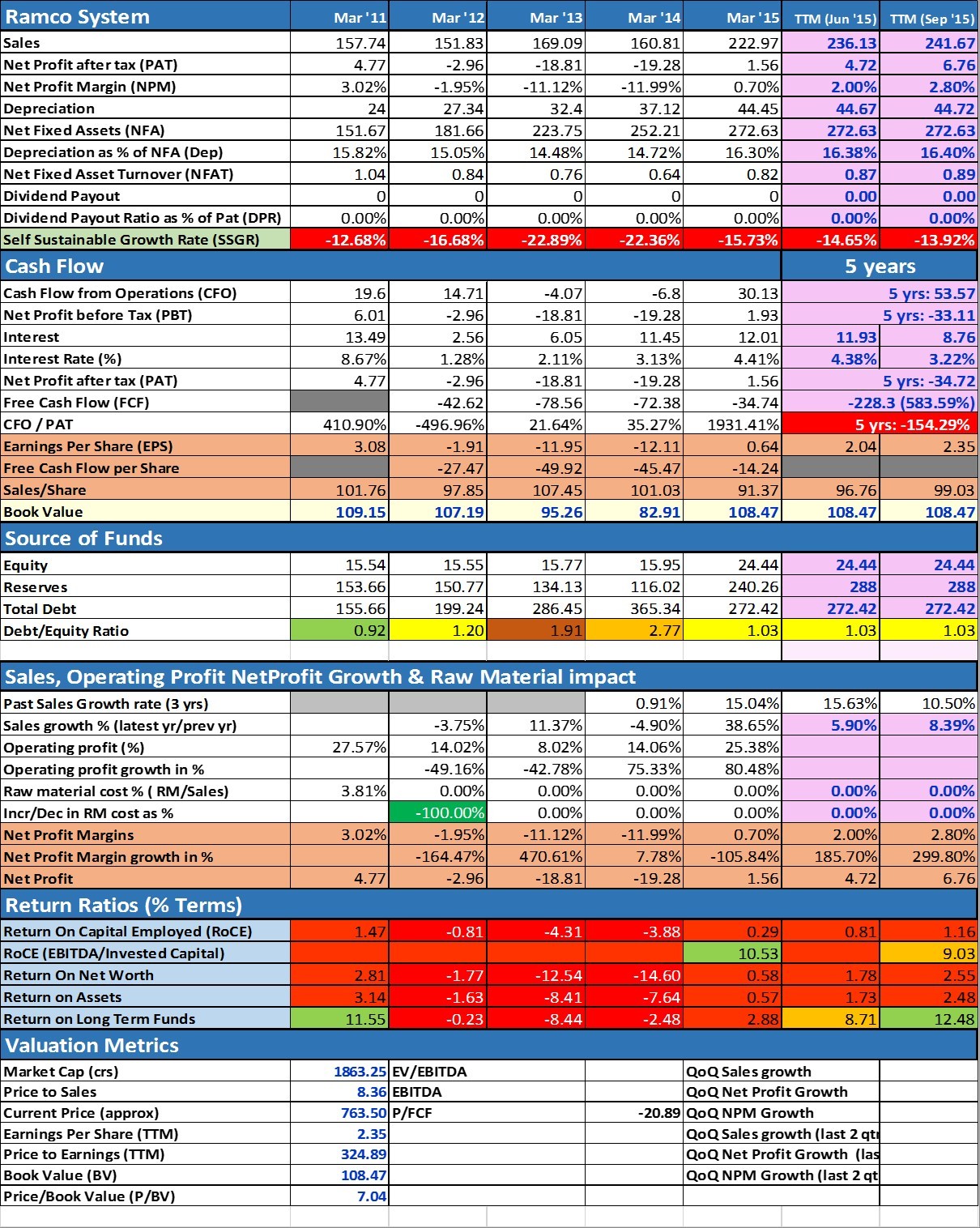

Interesting watch. Ramco CEO VA talking about FY16 Target in a HR Meet. Not sure if that was intentional. With Q2FY16 results just released, Half Year FY16 Revenue is USD 32.86 Mn. From his talk, FY16 Target looks like USD 89 Mn. Not sure if this doable by Fy16. But I believe his SAAS model can do wonders, and a nextgen IT company in making.

Some of the Company/HR policies he discussed is path breaking in Indian IT Industry. No wonder Ramco is getting good reviews on Glassdoor. And VA seems to have good flair on the latest technology.