Dear Ankit, Your posts are very informative. BTW do you track CAPITAL TRUST. I do not have economics background. Somehow the numbers seem to be appealing. Can you shower some light?

Posts tagged Value Pickr

Bhageria Dye-Chem (07-11-2015)

Hi,

I wanted to mention that Roce has varied a lot the last 5 years. Though the last two years have been excellent.

2015 14 13 12 11ROCE (%) 71.12 42.63 9.24 2.46 13.1

Source: http://www.geojitbnpparibas.com/company-information/Key-Financial-Ratios/-/530803

Thanks,

S

Avanti Feeds (07-11-2015)

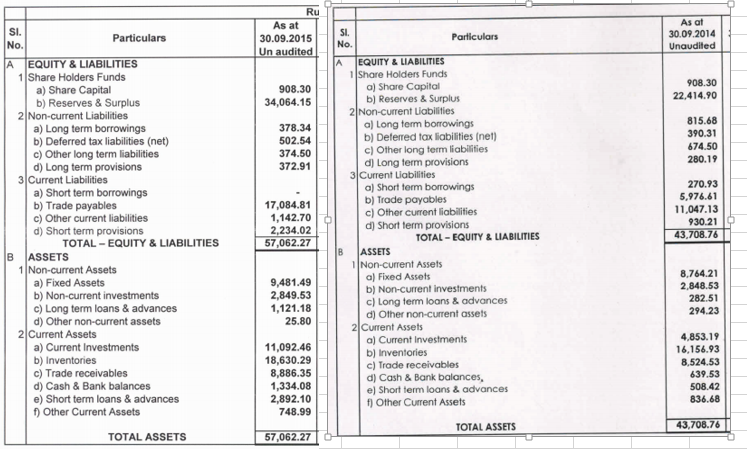

Current Liabilities -> Trade payables (increase); Other current liabilities (decrease)

Is this you want to highlight ?

Disc: Invested, more than 10% of PF

Avanti Feeds (07-11-2015)

(post withdrawn by author, will be automatically deleted in 24 hours unless flagged)

Please congratulate our new Heroes! (07-11-2015)

Thanks Vimal and Pratyush, i am new here but from first looks can say it will be an enriching experience to be with you guys and this site for a long time to come. thanks again cheers

[/quote]

Realtime Alerts for BSE Corporate announcements (07-11-2015)

Hi Sunil – Thanks for heeding to the request. It’s working smooth now. Just in time for a crazy Saturday of too many results

Kiran

Eicher Motors (07-11-2015)

Concall Details in brief:

Expect to sell in FY16 – 6.2 lac RE motorcycles.

New model to be introduced in FY16 and another one in FY17.`

Total 9 lac bike capacity by FY18. This includes availability for the year and not end of the year.

Major overhaul in the design of the retail stores. Total 500 dealer/stores this year target and 5 stores/dealer average each month next year.

More emphasis on”Soft-Sell” than “Hard-Sell”.

Infra and hardware set up for the process. Huge benefit accruing because of this new design format. Able to attract huge footfalls when compared to “Traditional” Stores and also enabling to convert to Sales thereby increasing the orders!!!

FY17 bike selling target between 6.2 and 9 lacs. i believe they should do 40% volume growth.

Vallam Vadagal plant expansion going on. Oragadam will fuel the next leg of growth along with Vallam Vadagal. Tirivattiyur will be providing the exisiting functionalitites as is.

60% of sales happening from Top 20 cities rest 40% from others.

There has been huge traction in the Tier 2 and 3 citites. Small towns which were selling 10-15 bikes are now seeing sales of 20-30. Hopeful of this growth going on…

10% of sales from first time users and youngsters. This was 1-3% few years before. This when converted is a massive growth. 3% on 3 lac sales in Fy14 comes aroung to 9K. This has moved to 40K-45K which is 10% of 4.5 lac this year.

Huge work going on in the international market. US will have the first roll out from Wisconsin in H1 FY16. 2nd store opened in London. Madrid and paris also have RE stores now. Increased store count in colombia. Also entered Indonesia.

Good growth in HeavyDuty vehicles. Light and Medium duty CV also recorded growth.

Raw material cost has come down for RE especially since the falling commodity cost made to good use. Not so much when for VECV when compared to RE.

Very much hopeful of replicating the success of India in developing markets like Latin American and South east Asian since there is a huge scope and huge market.

- There can be success like india, some markets may be not so successful and some markets may be better. The actual turnout will be clear after 5 years and all steps being taken to ensure success.

Export markets segmented to – developing nations and matured/developed markets.

There is a huge gap between 250-750 cc market and in the range of 3-4k dollar. Very less options available in this market and the company trying to fill this.

The waiting period is in the range of 1-4 months depending on the motorcycle models and has been reduced from 9 months in the peak time few years before and this is what company had also intended.

Overall liked the honesty, confidence of the management where they were even open in saying that there can be failures in some market , success in some markets like in India and there could be even better success than India in some markets.

FY16 will be a consolidation year. They want to increase the production to 50-52K per month average and will not be a straight line growth but skewed more to the end of the year with higher production. They want to stabilize the production/procurement/supply/vendor management first and then take it higher. Capex required will be clear in Feb annual meeting.

Disclosure: Invested. Investors pls do the due diligence before investing.

Need for KYC to be enforced when Forum Abuse is detected (07-11-2015)

Sure Admin.

Happy to work on this. Will come up with the template and share with you.

Regards.

Need for KYC to be enforced when Forum Abuse is detected (07-11-2015)

Good suggestion.

Like many places, at VP we like to give the ownership of good workable suggestion to the idea initiator.

a) Coming up with a reasonable idea initiation template where you are satisfied that there are multiple checks and balances – your job

b) You can then take the help of some VP Top Contributors to refine and present to Core Team

c) Meanwhile @pratyushmittal – please check feasibility of a pop-up/check mechanism that doesn’t accept the initial post unless it has this filled-up template, or some other work-around of achieving the same