I will let the number do the talking

Posts tagged Value Pickr

Need for KYC to be enforced when Forum Abuse is detected (07-11-2015)

IF I may be allowed to extend the suggestion by @reacher.

Yes ranking of idea is a good idea and should be available to each and every member.

Members can revise their ranking based on their gut feeling, available information, risk that are discussed on the thread.

Amol

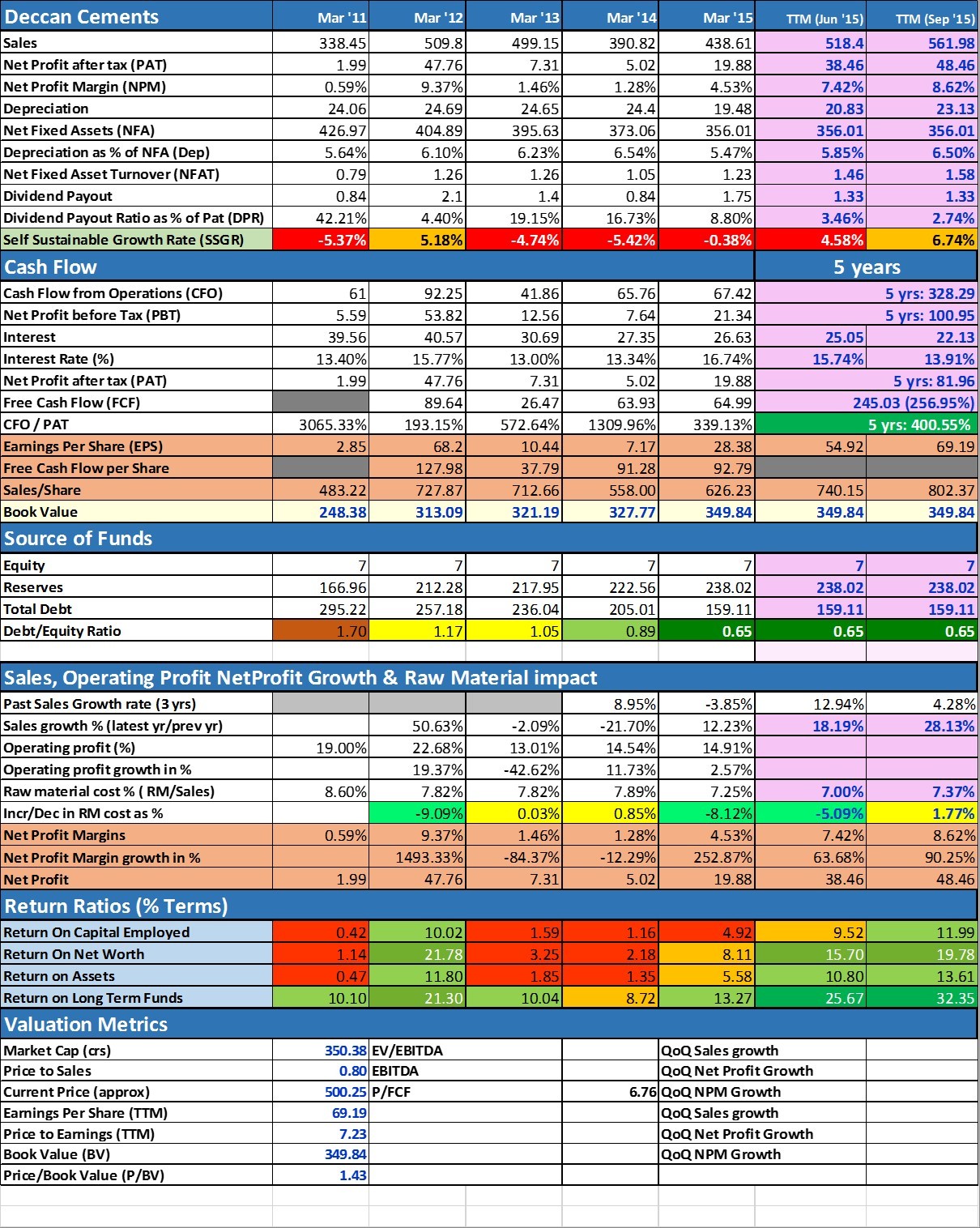

Deccan Cement : Dull company.Dull business.Big wealth creation opportunity (07-11-2015)

Seasonally this is the weakest quarter for cement companies due to rains & slow construction activity. If company can deliver such strong performance in this quarter with EPS of 22 then there is high probability of doing 25-30 EPS per quarter in the coming two quarters.

Looks very nice bet with almost negligible downside given current circumstances.

Disc. – Invested

Small banks (MFIs) v/s NBFCs – future? (07-11-2015)

Hi guyzz,

This thread is initiated to have a general understanding of the future of NBFCs in transforming India. With the introduction of small banks like Bandhan (MFI) in Indian markets I see a big threat for the NBFCs operating as of now. There are many reasons/views on this. I note down my points below. Would request others to share their views on the same to help the forum members have a clarity on the future of this financial market niche-MFIs !!

–> Banks have an advantage of low cost funding – they can have current accounts (0% cost), savings accounts (3-5% cost), fixed deposits (8% cost), external commercial borrowings and much more. Now we can argue that who is going to keep deposits in current, savings and fixed accounts – since the target market is low income class people. I have the knowledge that small people invest in VCs (chit fund type) wherein they earn more than 20% p.a. Why would they invest in FDs or mutual funds, etc. But with the increase in the share of organised sector in lending business (like Bandhan) number of people who used to borrow from VCs will reduce (since they will have access to cheaper source of funding – bandhan) – this will eventually lead to end of VCs. This along with level of economic activity and basic education levels will turn people to invest in mutual funds, FDs, etc. (this seems impossible but India is changing). One example – my servant never had a bank account and never believed to even. His son has a business and is having a savings and a FD account. With this assumption – Bandhan can have real low cost funds and can break the NBFC market in future.

Again one point to note is that the housing NBFCs like Gruh, GIC housing get some cheap funds from NHB (at 6% only). This needs to be taken in consideration.

–> Banks can act as one stop solution – you get every service with door step banking. DD, cheque facility, deposits, loans and much more like ATMs. NBFCs can not provide that. You can also invest in mutual funds through these banks. You can take insurance through them.

–> Bandhan has a good reputation and track record. they have been helping people by creating self help groups and advising them on their funding requirements, how to deploy them in their business and bring efficiency. This not only creates a good business, but also helps company build a social brand in market.

I am trying here to compare Gruh Finance, GIC housing with Bandhan. What do you think – who has a bright future !!

Disc – Not invested (none of them). Just want a general understanding of what can happen to this industry niche in coming years.

Deccan Cement : Dull company.Dull business.Big wealth creation opportunity (07-11-2015)

How to get this information of capacity utilization???

Ashok Alco-Chem (07-11-2015)

Q2 results were out few days back

Link : http://corporates.bseindia.com/xml-data/corpfiling/AttachHis/66C25777_2CEB_45FC_BD25_2AD18178C088_164430.pdf

The results have been decent. Though zero growth Y-o-Y but impressive Q-o-Q.

High ROCE business but markets seems to ignore it as the company is into commodity chemical trading.

Regards,

Sri Krishna Bhutra

Realtime Alerts for BSE Corporate announcements (07-11-2015)

Thank you Sunil. Investors breathing smoothing now, all over twitter investor was not feeling good due to non functioning of bsealerts.

Appreciate your hard work !!!.

Thanks,

Mahesh

Realtime Alerts for BSE Corporate announcements (07-11-2015)

@sunilsurana

Hi Sunil,

i was able to login and create my list.

Thanks a ton. Appreciate the effort put up by you, will be really helpful for so many fellow investors.

only issue , i could not find few names – Piramal Enterprises, Shriram city union fin, Tribhovandas

MPS Ltd (07-11-2015)

Thanks Donald for Mgt Q&A, I have atleast some basic understanding. Also read the entire VP thread. I think Mahesh Shah has posted some really very useful information.

Chuck Akre describes very well in his speech how to determine the fair value of any business and to surprise of most of us he do not use PE, PB or EV/EBITDA it depends more on qualitative factors read here https://www.evernote.com/shard/s68/sh/aa3cabf9-6e8f-477e-8c82-1ae14805a8e7/7cbbb92de7c10752

My understanding of MPS remains very limited and I remain scared of technology. For me the biggest block is to understand the organic growth drivers and the market opportunity itself. Are we talking about prospective market and possibilities or are we talking about ready market which is not served or explored. Is their a problem which MPS is trying to solve or MPS is selling a better execution strategy and need to convince prospective customers of its use.

Let me just pose few questions which are already discussed to some extent but remain important in my view

Key takeaways: 1) Not a commoditized business. Slightly better than a pure IT services company. 2) Organic growth of max 10-15% over next 3-5 years. infact for me this is the main impediment. I do not want to bet only on inorganic growth. Not able to understand clearly the sources of organic growth 3) Exit PE multiple not more than 20x over 3-5 years 4) future pay offs to shareholders depend on outcome of acquisition lead growth strategy.

Let me set the context right. I have no views either positive or negative. Just trying to throw some different angle for further analysis by playing a devil’s advocate:

What’s factored in price: Assuming that MPS will pay only 1x sales [could be materially higher] to acquire total addition to revenue over next three years would be 150crs. Assuming organic growth of 15%, MPS organic sales will grow to 350crs. Overall sales of 500crs. Now what sort of margins are possible. Even assuming organic EBITBA margins remain flat at 40%, giving generous margins of 15% on acquisitions [I assume they will acquire break-even or loss making entities], EBITA would come to 150crs. So a healthy 25% Revenue and EBITA CAGR. We can expect 7-10% CAGR for salary inflation over next 3-5 years. I am assuming that this will be absorbed by productivity and scale advantages and INR depreciation. Yes, am not factoring any appreciation of INR J. I think one should compare and contrast MPS with other similar size IT companies. In my understanding MPS is more an IT service provider than part of printing and publishing industry. If we see the margins of IT service providers, Average EBITA margins of last five years is around 27% [which is substantially higher than 24% during 2004-08]. I am guessing higher level of margins in latter period is due to steep INR depreciation. Why should MPS margins continue to remain at 36% [excluding FX gains & interest income] .I am not suggesting margins will decline. For a customer why he should not be comparing this outsourcing with what it does to IT firms. EBITA margins of bigger players are in the range of 10-20%. We need to dig deeper into why there margins are lower.

ON a TTM basis most of IT companies are trading at 15-25x PE. MPS is trading at 21X PE exl cash. So I guess it’s already trading at its top end of PE range. [Though I guess organic revenue growth could be higher in IT industry in general compared to publishing Industry].. Ofcourse we can pay premium for better capital allocation, high mgt quality and high dividend.

From reading of VP thread and MDA what comes out clearly is that customers are sticky. Then customers will be sticky to their existing vendors too. What makes us believe that existing customers won’t leave MPS but MPS will be able to convince others to shift vendors?

Vendor consolidation: I understand one of the main motive in vendor consolidation is pricing advantage from bigger players. Top three players EBITDA margins is in the range of 10-20%. Taking the example of Infosys I would argue that either one can maintain top line growth or margins. It would be difficult to control both. Not arguing margins will crash to 20% would in our 3-5 years estimates we should factor in lower margins.

Acquisitions: All the top three players are backed by big institutions. So I guess there won’t be scarcity of money for them. All of them will be chasing the same players and seller will have lot of options. So can be count on getting acquisitions at reasonable price.

So if one wants to play inorganic growth story and good capital allocator, One should also compare and contrast other bets like Piramal enterprises and leaving the question of valuation aside Thomas cook too. Businesses like Shriram transport, Shiram city union, Contract research and their own quasi NBFC which is lending to real estate and infrastructure can easily grow at organic growth rate of 15%. DRG which is their data analytic business is an exception where organic growth rate will be only 5-7% [DRG contributes 15% to EV] and key acquisition are more or less are done except for one or two more. So if one wants to play inorganic growth story and good capital allocator purely on valuation basis, One should also compare and contrast other bets like Piramal enterprises and leaving the question of valuation aside Thomas cook too

.Lastly end market [publishing market] at best is growing at 4-5%, unless it is the case that we are standing at the beginning of the outsourcing trend. Technology is going to be key differentiator for publishing entities who are fighting for their survival in their fight with companies like Amazon. So how much they will be willing to outsourced should also be questioned. So regarding the potential to some extent there is some similarity with Kaveri seeds where the market size was/is growing at single digit and main bet was on increasing market share. But unlike Kaveri, MPS is only a marginal player in the industry and not a market leader.

Arman Financial Services Ltd (07-11-2015)

Arman came up with good set of numbers for Q2FY16 with interest income growing by 40% while profit after tax growing by 38% on a consolidated basis (MFI plus two wheeler). The press release for the quarterly result which should be out in a few days and concall would give us more details about the growth in AUMs of MFI and two wheeler segment as well as the development on the expansion in MP for MFI business.

Disclosure: Invested at an average price of 49. Forms more than 10% of my pf.

This is not an investment recommendation. Pls do your own due diligence before taking any action. Have been following the stock since more than a year and have been single handedly posting about it but not a post to promote the stock.