I had to close thrice and restart.. Pl try the full cycle and check

Posts tagged Value Pickr

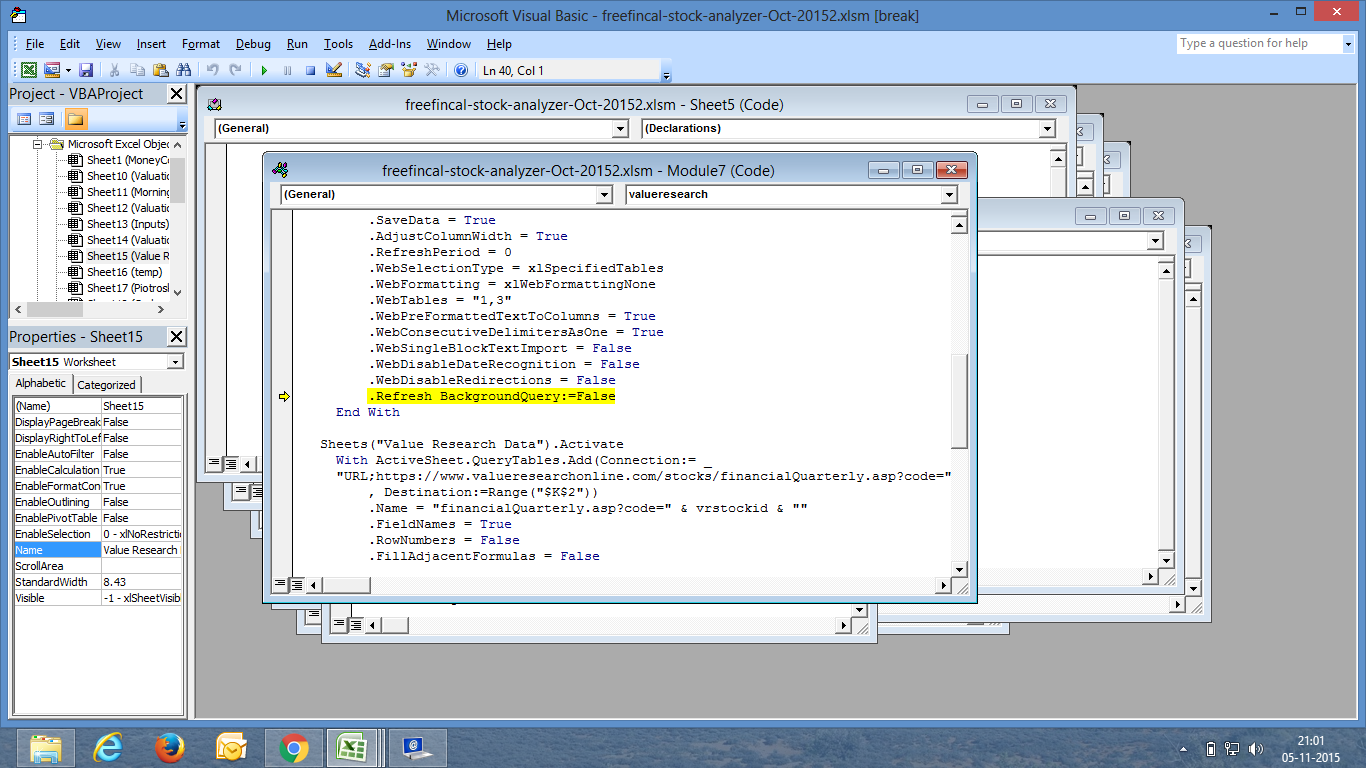

Automated Stock Analyzer (05-11-2015)

Works fine for me. Not a problem with Excel. Could be a firewall issue if done from work.

Abbott India: MNC pharma play on increased consumer spending (05-11-2015)

Positives

Look at the stock price of Abbott USA, shows a consistent rising trend with some slowdown in the last year. This indicates that they’re doing something right over there. Related link: http://www.bloomberg.com/news/articles/2015-11-05/meet-the-world-s-most-confident-consumers-flush-with-credit

Look at the products that they’ve launched. Ask a person who uses Pediasure… They’ll tell you that they buy it irrespective of the price.

Government spending in preventive healthcare has increased a lot in the past 2-3 years

A doctor who knows about Preventive & Social medicine says that major posts in rural government missions are being filled by PSM doctors

Connecting the dots backward indicate that they’re a consumer focused company

Nutritional product buyers love the brand they buy and are willing to pay the price

Promoters hold a major stake indicating they want control over how they invest going forward

Concerns

Privately held subsidiaries of the parent company operating in India

Sarla Performance Fibres – Another Interesting Textile Story in Making? (05-11-2015)

I am using the Nylon 66 thread now and let me tell you, there is no one who cam make ropes like the ones made by Sarla Flex in the US. There are top quality and as their usage in human life goes up, so shall the stock price, they have just started the US thing and at 59 I took a sizeable position. I am expecting that after these umbers posted in Nov 15, the company can do wonders over the next few quarters till 2020 if it goes to 100% capacity in US too.

Prashanth Jain and Kenneth Andrade have a positive view on this too, just a matter of time before they get in.

Lincoln Pharma … the next mid-cap pharma in the making …? (05-11-2015)

@ansii77 heyy….stake doesn’t matter. My question is on the operation of the subsidiary where PAT margin is too low to be believed. Chances of cash being taken out is high in this scenario.

While I noted ur point on the stake.

MPS Ltd (05-11-2015)

@Mahesh Mahesh

Just want to acknowledge your early work in MPS.

The competitive data that you had put up brought a lot of perspective for the early investors into MPS. You were he one who pointed to different margins at play among the bigger players, and other such data painstakingly put together.

Guys, if you give importance to this type of work at VP, please go back in this thread, and provide big-thumbs up (add your Likes) to that specific post that really stands out even today when you go back and browse the thread, among others

My perspective is that MPS is well known as a brilliant turn-around story in the last 2-3 years. What is interesting is that it could well be in the “Global Sweet Spot” that Management paints in 2015 AR (we should ignore the sleekly hyped up parts by Kolkata based AR expert, but not IGNORE the facts either)

Having said that, let me re-iterate for the benefit of newbies at VP

Do not start salivating at Mahesh’s well-meaning comments either, no matter how much you respect anyone’s work/contribution  . Don’t think the Verdict is out in the open. I wouldn’t venture such adjectives as NO-BRAINER or mouth-watering prospects with some fixed multiples like EV/EBITDA or Acquisition track record, just yet. Can’t be as simple as that, can it. As Hitesh has astutely observed A lot depends on how the Management walks the Talk in the next 2-3 years; how it executes, especially on acquisition front – that can make or break it – Ticket sizes are much bigger 10x last times – one can’t help overemphasise.

. Don’t think the Verdict is out in the open. I wouldn’t venture such adjectives as NO-BRAINER or mouth-watering prospects with some fixed multiples like EV/EBITDA or Acquisition track record, just yet. Can’t be as simple as that, can it. As Hitesh has astutely observed A lot depends on how the Management walks the Talk in the next 2-3 years; how it executes, especially on acquisition front – that can make or break it – Ticket sizes are much bigger 10x last times – one can’t help overemphasise.

The endeavour from here should be to dissect – Is it really in a Global Sweet Spot? Really? Why or Why not? Lets focus on that.

Let’s ask tough questions on Business Quality. Sustainability of Competitive advantage for a Long Time, Can someone dislodge it from its perch? What all can go wrong?? Predictability of the Revenues/Profitability, Can it be a consistent performer over 3-5-10 years, why or why not? A lot lies on the answers to the above questions – Valuations will reflect that.

Disc: I am invested, as disclosed in the Management Q&A post. Very small allocation 2 years back. Having set the contours of the business that MPS operates in, I now find it has very little operational challenge, or disruptive competition, or Customer pressure. Everything works to its advantage, unlike many other quality businesses, It’s quite free to keep executing. Much of my confidence is an ACT of FAITH …The story can play out differently, if execution falters

Everyone – As influencers in this discussion/debate don’t forget to add your disclaimers. Its a MUST. Also Like to remind we need similar disclosures if & when you exit, within reasonable timeframes.

Automated Stock Analyzer (05-11-2015)

@Doonsrini, error corrected and file reuploaded. Thanks.

Sarla Performance Fibres – Another Interesting Textile Story in Making? (05-11-2015)

Minutes of concall (note – had to be in/out of concall due to some work)

- Volume grew marginally by 4% y-o-y

- USA plant has broken-even

- Company is enjoying gross margin expansion due to crude price fall. Gross margins for H1 FY2016 have been 62%. However, historically gross margins have been ~52%, which is also very appreciable

- Nylon 66 plant commenced operations. Full year sales from Nylon 66 is expected to be ~INR 15 cr. hence, contribution to H2 FY2016 is INR 7.5 cr. 2 shipments already made till date

- RM/sales ratio is USA ops is 30% implying gross margin from USA plant of 70%!! RM/sales ratio from India ops has been ~50% over last decade!

- For H1 FY2016, India capacity utilized = 4700 TPA and USA capacity utilized = 1900 TPA

- Training manpower in USA ops is creating delay in USA plant’s ramping up

- Guidance for FY2016 sales of INR 350 cr. and PAT of ~INR 46 cr.