I raised this issue on MMB too, got attacked by other boarders. Looks a bit like Indian Terrain, but different industries.

Invested in Control Print since Rs 200 level, will probably get out around 500-550.

I raised this issue on MMB too, got attacked by other boarders. Looks a bit like Indian Terrain, but different industries.

Invested in Control Print since Rs 200 level, will probably get out around 500-550.

Hiteshbhai,

Excellent narration of the Jagran story. Few questions I have

1) Company’s operating margins in last 5 years have been fluctuating between 19-29% and hence the bottom line growth seems relatively slower compared to its peer (DB Corp – CAGR 12%; HMVL – 28%). What is the normalized margin trajectory for Jagran post turn around of Nai Duniya & Mid day and consolidation of radio business?

2) There is hardly any top line growth in Other publications (Mid day, Nai Duniya), Dainik Jagran has been growing at 10% odd CAGR while radio business has been growing at faster clip but with much smaller base. In this context, what will drive the topline growth going forward?

To me, two critical catalyst in the Jagaran’s case

My only concern remains about large inventory holding and probable obsolescence of the same

in future.

Hey Everyone,

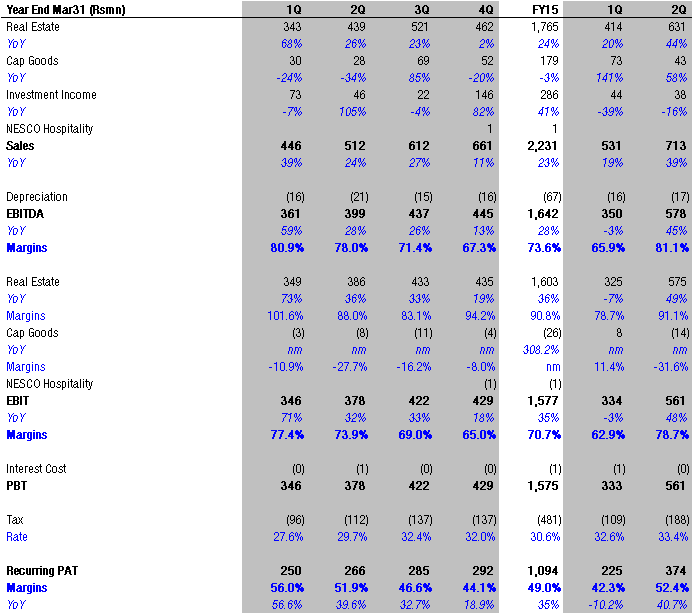

Please note down the following points in connection with Q2 (2015) Conference Call:

Overall:

1) Q2 financials : 45 cr (2015), 36 cr (2014)

25% growth YOY EBITDA 10 cr (2015), 7 cr (2014) EBITDA margin 22%2) Lease Model

Contribution of Lease Hotel is 39%

Average room rent INR 2950

Room occupancy rate 51%

Total Rooms 623Currently Byke has 697 Rooms and is targeting 1200 Rooms by 2018. Focused to grow via leased and chartering business.

3) Room Chartering Model

Contribution of Room Chartering is 61%

Average room rent Q2-2015: INR 2400,

Occupancy rate : 91%

Inventory sold 1 Lakh

240+ AgentsA) Question:

In connection with OYO as competitor –

Answer:

Yes, Byke understands the trend of mobile penetrating and also updated the following:

1) Assured that currently focussing on Agents

2) Looking to burn less cash when compare to OYO as they love making money than burning

3) OYO is in different business;

4) The pie is very big;

5) 1% of total market available.

We buys inventory only for the season time and OYO guarantee’s for the whole year.

B) Question

With regards to Higher Occupancy Rate when compared to competitors?

Answer:

1) We buy inventory only in season time.

2) Advance of around 3-4 months given to hotels.

3) Using network 50+ cities.

C) Question:

In connection with websites working on selling hotel rooms?

Answer:

1) They just guarantee hotel, no inventory is booked.

2) No booking of room by them.

Conviction is getting stronger and stronger after listening to this call.

Regards,

Gaurav

Skipper is showing improvement and results are quiet impressive from last year onwards…

The self sustainable growth is very visible.

for SSGR see Dr Vijay Malik’s explaination: http://www.drvijaymalik.com/2015/06/self-sustainable-growth-rate-measure-of.html

Today facebook showed me this adv. about a dealer selling Royal Enfield close to Taipei (I live in Taipei)

Makes me think, that the brand is travelling to places where company hasn’t even started selling officially. This is very promising development. Helps to seed the idea/culture and fan club around it.

It’s selling for almost 4x of India price, but Taiwan is known to have atrocious tax rates for bike imports so that could be contributing to it.

Taiwan has a huge leisure bike riders market. Mostly dominated by BMW’s, Harley,Triumph’s of the world.

This is really setting the stage for something very interesting.

Make me very happy !!

vardha ji

increase in authorized share capital is the first sign of raising funds to fund working capital ? (eg : through debt) or any other plan they have for rise in auth capital.

even eros has ballooning receivables, as we knew recently news on eros.

Rohit, Hitesh,

One of the reason for higher valuation to DB Corp is their ability to enter any given market and start as No.1 or 2 newspaper from day 1 of circulation, which no newspapers in the world are able to achieve. This reduces their gestation period.

Director Ravi kumar is taking pay of only 30Lakh Rs which is very modest for 20Year experience and he owns 8 lakh shares.

Ashok Atuluri took 1.4Cr salary in 2012 when they were in profits. 2013, 2014 he took only 30Lakh

Management looks to be honest and incentives are tightly coupled with performance.