Co was repr by Laurent Demortier, CEO & MD.Highlights of call by Capital Mkt

Consolidated order backlog as end of Sep 2015 was Rs 8428 crore with order intake for the quarter being Rs 2886 crore.

Order intake in Q2FY16

India Non India CG global

Power Systems 714 1636 2350

Industrial 452 84 536

Total 1166 1720 2886

Order Backlog as end of Sep 2015

India Non India CG global

Power Systems 3145 4607 7752

Industrial 553 123 676

Total 3698 4730 8428

Figures in Rs Crore

The company is in the process of monetizing its investment in non strategic business as well as assets. In this regard on Oct 8, 2015, the BoD have approved divestment of its entire 50% stake (investment of 600000 equity shares of RS 10 each) in medium voltage business i.e. CG Lucy Switchgear (CG-Lucy)to W Lucy & Co of UK for a consideration of Euro 5.50 million. Similarly the company with effect from Aug 12, 2015, has terminated the Distribution Franchisee Agreement (DFA) with MSEDCL for Jalgaon Circle Area.

On Oct 16, 2015, the BoD have also approved entering into definitive agreement for the sale of a portion of its land in Kanjurmarg, Mumbai admeasuring approx 53000 sft for an aggregate sum of Rs 496.48 crore.

International power systems (IPS) business continues to be impacted by ongoing divestment process. The buyer has completed due diligence of of all plants and expects definite offer by end of Dec 2015.

Automation orders backlog as end of Sep 2015 was Rs 831 crore with order intake in Q2FY16 being Rs 441 crore. Revenue from Automation in Q2FY16 was Rs 197 crore, which is flat compared to corresponding previous period.

Proceeds from monetization of non core business/assets will be used to reduce debt at international operations.

Lower EBIT for consumer business in Q2FY16 is largely due to the company accounting an amount of Rs 15 crore towards certain cost heads which was hitherto accounted under unallocated under consumer biz.

Exports revenue in Q2FY16 was Rs 329 crore which is higher compared to Rs 317 crore in Q2FY15 and Rs 133 crore in Q1FY16. Exports order backlog is Rs 883 crore.

Kanjurmarg – Out of 34 acres the company initially sold 8 acres and now has sold another 13 acres. Nothing more will be sold in the next 12-18 months.

Two quarters from now the high rating transformer orders will start contributing to topline and that will improve the India power system margins from FY17 onwards.

Posts tagged Value Pickr

Crompton Greaves- Looks like a turnaround story (31-10-2015)

Vinati Organics (31-10-2015)

Vinati organics reported its quarterly result today…..

Overall, flat quarter on Q-o-Q basis and muted growth I believe.

Disclosure: Invested

Screener.in: The destination for Intelligent Screening & Reporting in India (31-10-2015)

I know but in this case one has to delete and re load the ratios. The click and move method made things easy. I was just hoping.

Thanks

Kumar

Screener.in: The destination for Intelligent Screening & Reporting in India (31-10-2015)

Hello ayush, has the export to excel option gone ?

Also would it be possible to compare companies in screener ?

Economic Value added (31-10-2015)

Hello friends, In try to anslyse stocks , I often come across a metric called EVA( Economic Value added) . I have also seen the same in Pidilite’s anural report. Could some provide a writeup on it ? Is that worth exploring ?

KDDL (Ethos Watches) – Scalable business model at an inflection point? (31-10-2015)

Promoter shareholding is down in Sept quarter . 52.83% in June end quarter to 47.62% in Sept end quarter. Not a good sign for KDDL.

Torrent Pharma Ltd (31-10-2015)

Crestor is a quite a big molecule for fy17. it is $6b and a growing molecule, They seem confident of doing well here.

They also mentioned in next 2 years there will be about 20 launches of which 5-6 will are very lucrative launches with limited competition.

Besides that, they are hiring a lot of R&D people of around 1000, and increasing the filings. The increased filings will start from q1fy17.

So from fy17, we will see increased filings with increasing complexity of ANDA filed (like cream and ointments and some would that would require clinical trials too) . Oncology green field plant is another positive.

They would also be launching many first timers in india with innovative dosage and combinations ( I think this is ajanta like strategy) and then replicate this india model in brazil.

Tax rate was 36% in 1H and will from fy16 point of view, it will be 25%. so, H2 there will be reduced tax rate.

KDDL (Ethos Watches) – Scalable business model at an inflection point? (31-10-2015)

Hi all ,

Has anyone done any scattlebutt research by visting an Ethos store ? I am from Chennai and I am planning to visit the store in Vijaya mall soon. Any specific things you guys think I should watch out for ?

More Introduction to Financial Accounting @Coursera [Helps to be an Equity Investor] (31-10-2015)

More Introduction to Financial Accounting

By Professor Brian J Bushee, Wharton School of the University of Pennsylvania.

Continuing the discussion from Introduction to Financial Accounting in Coursera:

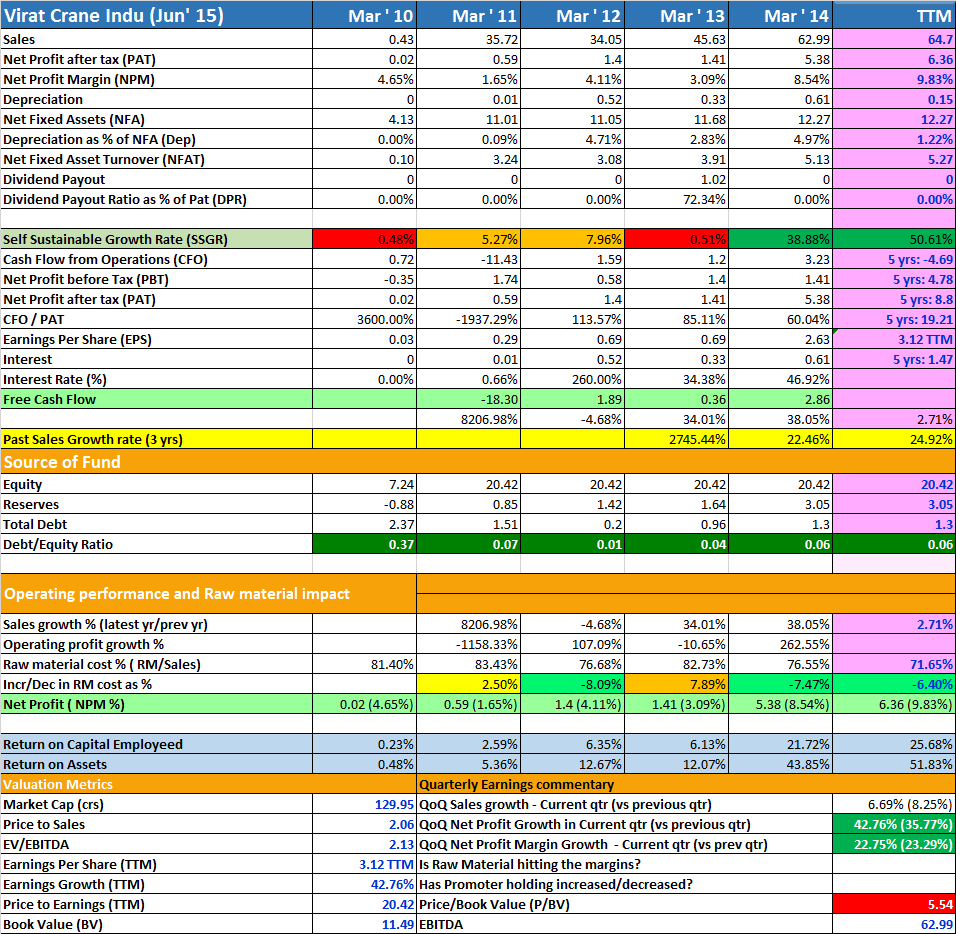

Virat Crane Industries Limited (VCIL) – sure shot multibagger (31-10-2015)

Not only RoCE, RoA and Asset turn over showing growth. The Self sustainable growth rate is also showing good growth. http://www.drvijaymalik.com/2015/06/self-sustainable-growth-rate-measure-of.html

This SSGR growth is important for company like Virat as it needs to fuel its growth with cash it generate.

Disclosure: Holding small qty and hoping to add more on decline.