Rajeev Jain – CEO of the company addressed the call:Highlights by Capital Mkt

Assets Under Management (AUM) surged 36% to Rs 37964 crore at end September 2015 from Rs 28004 crore at end September 2014. Deployments jumped 51% to Rs 9236 crore in Q2FY2016 from Rs 6115 crore in Q2FY2015.The company is targeting an AUM (loans) growth of 20-25% for FY2016, while expects the growth to be higher at 35%, if the festive loan demand turns out to be strong.New loans acquired galloped 42% to 13,93,309 in Q2FY2016 from 9,78,174 in Q2FY2015.Loan losses and provisions increased 71% to Rs 137 crore Q2FY2016 as against Rs 80 crore in Q2FY2015. The company made accelerated provisioning of Rs 31 crore in Q2FY16. Adjusted for this, loan losses and provisions growth is 33%.

Return on Assets and Return on Equity for Q2FY16 were 0.8% and 4.2% (not annualized) respectively. ROE is adjusted for capital raised by the company through QIP issue of Rs 1400 crore during Q1FY16.

Gross NPA and Net NPA as of 30 September 2015 stood at 1.67% and 0.46% respectively. The provisioning coverage ratio (PCR) stood at 73% as of 30 September 2015. Net NPA & provisioning coverage ratios have shown improvement from 0.48% and 67% respectively a year ago.Capital adequacy ratio (including Tier-II capital) stood at 20.49%. The tier I capital stood at 17.32%. The Company continues to be well capitalized to support its growth trajectory.

Two Wheeler financing business disbursed 139K accounts in the quarter (11% YoY). Three Wheeler financing business disbursed 8K accounts in the quarter (21% YoY). Consumer Durable business had a strong quarter disbursing 908 K accounts (36% YoY).Existing customer penetration continued to remain strong. The business launched its first co brand EMI Card proposition with Vijay Sales the second largest retailer in India.

Retailer finance business & extended warranty cross sell for consumer durable business remained strong, disbursing Rs 930 crore (83% YoY) and 45 crore. Extended warranty volume penetration crossed 16% in September 2015 from a low of 7.5% in the previous year.

Digital product finance business disbursed 126K accounts (102% YoY) during the quarter. Business crossed 50K accounts for the first time in the month of August 2015. Business is also exploring partnership opportunities with wireless carriers for financing packaged products.

Lifestyle finance business disbursed 38k accounts (92% YoY). The business continues to focus on identifying new categories like mattresses etc. New category additions should help the business accelerate growth in second half.

Salaried personal loans continued its strong run during the quarter and disbursed Rs 715 crore (88% YoY). The medium term strategy for the business is to grow direct business and deepen geographic penetration. Business added 15 new locations during the quarter to deepen its geographic footprint.Salaried home loans disbursed Rs 246 crore (119% YoY). The business launched Developer Finance product during the quarter. HFC license is expected further augment the delivery of its strategy.E-Commerce finance business launched in June 2015 with a ‘Seller Finance’ offering for sellers of Flipkart and Snapdeal disbursed Rs 49 crore across more than 140 sellers in Q2.

Rural lending business continued to be the fastest growing business in Q2 as well, disbursing Rs 361 crore (284% YoY). The business added 18 new branches across states of Madhya Pradesh, Karnataka, Maharashtra and Gujarat during the quarter. The business is now present in 272 towns and villages in less than 3 years of its launch. The diversified business model pursued has delivered rich dividends.Retail construction equipment finance business now has receivables of less than Rs 90 crore. This business had 1,100 crore of receivables at its peak. Due to timely exit from the business, the company has managed to come out with no capital loss over the 5 years of this business. Incremental provisions are expected to be non-material and the business is expected to fully wind down in the next 9 months time.

Loan against Share business had a good quarter with a net assets addition of Rs 159 crore (80% YoY) catalyzed by growth in its retail segment.

Structured Finance, Financial Institutions (FIG) lending business & Light Engineering Vendor Financing business are beginning to grow well and disbursed Rs 310 crore in Q2 (Rs 195 crore in Structured Finance, Rs 105 crore in FIG & Rs 10 crore in Light Engineering).

Relationship management (RM) strategy launched this year has started to deliver on growth momentum. RM business disbursed Rs 376 crore in Q2 (61% YoY).

Fixed deposit business garnered Rs 413 crore of new fixed deposits during the quarter taking the total deposit book to Rs 1467 crore (233% YoY). The average deposit amount stood at 3.3 lakh with a weighted tenor of greater than 24 months.

Interest cost for the company continues to remain significantly lower amongst its NBFC peers. Borrowing mix at the quarter end stood at 47:48:05 between banks, money markets and retail deposits respectively.

Posts tagged Value Pickr

Bajaj Finance Limited (30-10-2015)

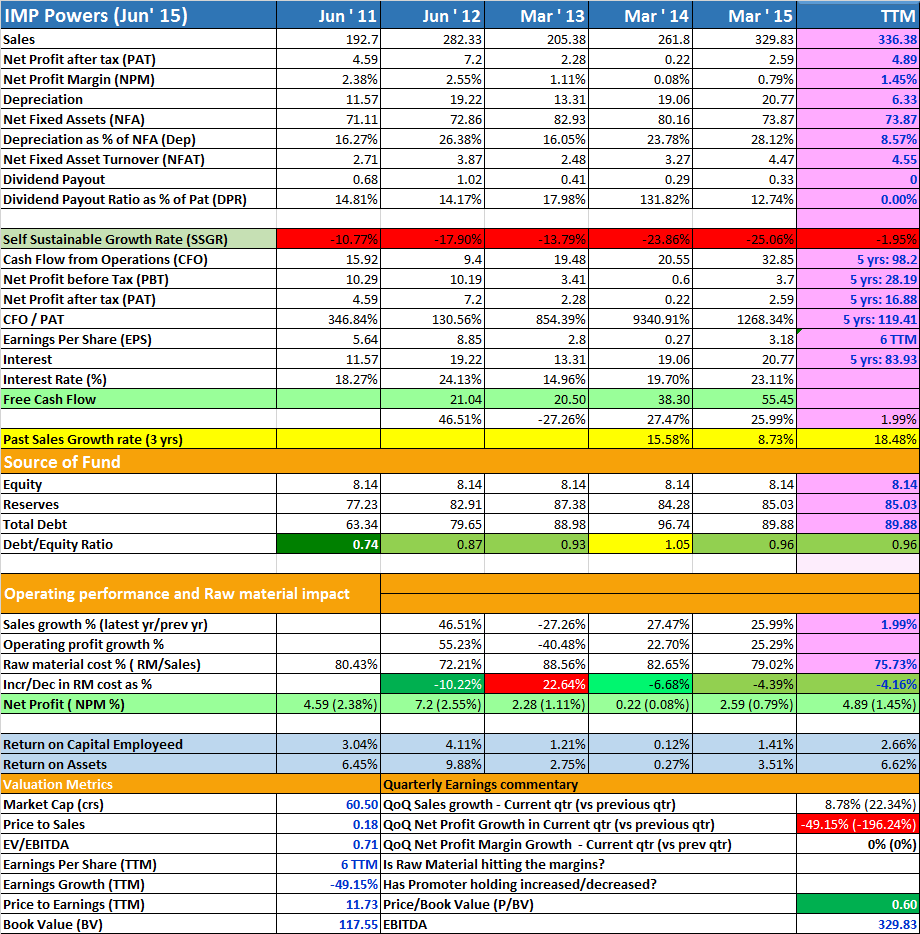

IMP Powers Ltd – Transforming through Transformers (30-10-2015)

There are improvement signs.

for e.g. the RM cost are reduced…need to see more in coming quarters

The SSGR is improving but still in red below 0.

For SSGR = Self Sustainable Growth Rate see http://www.drvijaymalik.com/2015/06/self-sustainable-growth-rate-measure-of.html

Debts are not big.

If you believe this is an good stock to add and hold then its at very good valuation given that recent growth it has shown and capex it has done.

INOX Wind (30-10-2015)

Call add by Deepak Asher,Director &Mr.Devansh Jain ED.Highlights Capital Mkt

Sales volume including equipment and turnkey supply, in Q2 FY’16 stood at 212 MW as compared to about 114 MW YoY. Commissioning however stood at 140 MW as compared to 30 MW for Q2 FY’15. There are about 160 MW of wind turbines yet to commissioned and will be commissioned during rest of FY’16.For 6 months ended Sep’15, the sales volume including equipment and turnkey supply stood at 332 MW, an increase of about 84% on YoY basis. For 6 months ended Sep’15, commissioning stood at 218 MW an increase of about 627% on YoY basis.Of the total revenue of Rs 1008.2 crore for Sep’15 quarter, about 92% of revenue came from sale of products and rest from sale of services, as compared to the entire revenue of Q1 FY’15 of about Rs 304.37 crore from sale of products.

During Sep’15 quarter, about Rs 194 MW of orders were added as compared to about 212 MW of orders being executed. About 71% of total order book of 1202 MW is from Turnkey and rest from Equipment supply. About 39.1% of order book is from MP, about 38.3% from Rajasthan, 21.8% from Gujarat and rest from Andhra Pradesh. The order book has an execution time frame of about 12-15 months.The company has sufficient land bank of capacity more than 5000 MW as on Sep’15. The company is in process of increasing land bank in existing States as well as new States like Tamil Nadu. As per the management lot of action is seen from States like MP, AP, and Gujarat in terms of signing the PPA’s from wind power while Rajasthan has slowed down. More States are expected to participate.

Orders are from clienteles such as Tata Power, Sembcorp Green infra, Bhilwara energy, CESC, Renew Wind Energy, Ostro Energy, Continuum Wind and PSUs such as GMDC, NHPC, RITES, GACL etc.The Blade plant at MP got commissioned in Sep’15 quarter. The Tower plant in MP is on track and will get commission in H2 of FY’16. The new 100 meter Rotors have higher efficiency and higher energy yields which will result in higher margins for the company. 113 meter turbines which will be launched in H2 FY’16 will also result in higher margins for the company.Ebidta margin for Sep’15 quarter stood at 13.6% as compared to 16% for Sep’14 quarter. Excluding forex fluctuations on like to like basis, Ebidta margins stood at 14.1% as against 15.3% for Sep’14. Lower margins were on account of higher employee costs and site related activities for future upcoming facilities. As per the management, margins are set to improve only from here on.Net working capital days fell to about 148 days as compared to 169 days as on June’15. Lower inventory levels and receivable days together with steady order intake, helped in improvement in working capital days.Government’s thrust on Renewable energy continues to remain. RBI notified Renewable energy lending under Priority sector in end of FY’15. Government aims to add about 10 GW of power capacity every year through wind sector.Overall management continues to remain optimistic for rest of FY’16.

Enil (30-10-2015)

Call was addressed by Prashant Panday MD and CEO.Highlights by Capital Mkt

Sep’15 quarter earnings include costs that are built in for Phase 3 auction. On like to like basis, Ebidta would have grown by 20% and PAT by 26% for Sep’15 quarter on YoY basis.The entire revenue growth of 11.6% for Sep’15 quarter was led by price increase and better product mix. There was a price increase of about 7.5% in Sep’15 quarter and volume de-growth of about 3%.Volumes in major metros were higher on YoY basis, while in other market were lower on YoY basis.The company operated at 97.5% capacity utilization led by Metros. The entire focus in Sep’15 quarter was on pricing and company let go some of the volumes. Also the company increased its distribution of frequency in late night stations. Distribution of delivery was planned very well during the quarter.

Metros have done stronger due to E-commerce sector. E-commerce contributed about 11% of total revenue as compared to 4.7% YoY. Other sectors that positively contributed include Government, Auto and Automobile sector, BFSI sector. Some sluggishness was seen in sectors like Retail, Durables, Telecom and Media and Entertainment etc.The company bid very rationally in Phase 3 auction and there was no overbid. Entire migration of 36 stations was done at almost same license price. The company now holds license for next 15 years.

The company added new cities like Kochi, Chandigarh, Calicut, Gawahati, Jammu, Srinagar and 4 stations were acquired from TV today. With this, the company has now presence in more than 40 cities in the country.The company also acquired 2nd frequency and 2nd brand in the 12 out of total top 13 markets in the country. These 13 markets contribute about 70% of total revenues. This 2nd frequency will generate higher Ebidta as most of the programming and other costs are more or less the same. The company plans to do more with the product and will launch gradually.In all, the company spent about Rs 340 crore in Auctions of Phase 3 and on Migration led costs.Overall, management expects the Radio industry should grow around 12% in FY’16.

Kitex Garments Limited (30-10-2015)

Are we not over analyzing stuffs ? just asking

Cera SanitaryWare Ltd (30-10-2015)

Mr. Bharat Mody, strategic advisor addr the call.Highlights by Capital Mkt

Bathroom products maker Cera Sanitaryware has achieved 13% rise in top line to Rs 225.30 crore and a 14% increase in net profit to Rs 17.88 crore in the second quarter of the current fiscal ended on September 2015.The company witnessed growth in all segment in Q2, with highest growth witnessed in Faucetware, meanwhile modest growth observed in Sanitaryware and Tiles segment. The company registered growth of 44% in Faucetware, 16% in tiles, and 8% in sanitaryware in Q2FY16.The Company received 63% business from sanitaryware, 21% business from faucetware,13% from tiles, and balanced 3% from allied products. The Company expects sanitaryware business will reduce to 58% from present 63% in mid-term (3-5 years), but faucetware, tiles, and bathroom ware business will increase during the period.The company hasutilized 90% ofincreased faucetware capacity of 7,000-8000 units a day in Q2 FY 2016 and plans to achieve a 95% of capacity utilization by end of FY 2016.The company has maintained rolling capex of around Rs 180 crore for next 3 years which will mostly funds from internal accrual.The company plans expansion of sanitaryware capacity to around 32-33 lakh units from present capacity of 30 lakh units.The Company has entered into a joint venture agreement with Anjani Tiles for setting up a plant to manufacture high-quality ceramic vertified tiles, in Andhra Pradesh. The Company envisages building initial capacity of around 10000 sq meter per day with initial project cost of around Rs 68 crore. The commercial production is expected to start by end of FY 2016.

The Company also decided to open offices in Dubai and/or Sharjah in order to increase exports to West Asian countries.The company has taken price hike of around 3-7% across the products effective from 1st December 2015 to maintain healthy margin.

The Company maintains marketing expenditure of 4.5% as a percentage of sales. It includes media budgets, also includes marketing.The Company has lowered its revenue guidance to 18-20% for FY 2015 from previous forecast of 20-22% due to lack of demand for the products amid low replacement demand from consumers and sluggish growth in real estate sector. Also, the company guides to maintain EBITDA margin at around 15%.

Anyone looked at Somany Ceramics (30-10-2015)

Mr. Abhishek Somany, Jt MD, addr the call.Highlights by Capital Mkt

The Company has delivered decent set of numbers maintaining positive trajectory on Volume growth and market share gain despite seasonally lower Q2 and first half and challenging demand environment. The Company strong Brand has helped to maintain Business momentum.Loss in volumes due to truck strike in late September and an exceptional loss of Rs 3.8 crore pertaining to last year impacted the second quarter earnings. The Company lost out of about Rs 22-23 crore of sale partly on the 29th and on the 30th on non-availability of trucks. The Company has paid Rs 3.83 crore to GAIL India towards one time settlement of ‘Pay for If Not Taken Obligation’ for CY14.Net sales of the Company grew 8.4% YoY to Rs 403.33 crore in Q2FY 2016 and rose 13.2% to Rs. 794.79 crore in H1FY 2016. Q2FY 2016 PBT before Exceptional Item grew by 24% to Rs. 20.28 crore, a margin of 5%. In H1FY 2016, PBT before Exceptional Item grew by 27.3% to Rs. 36.36 crore, a margin of 4.6%.Q2FY 2016 PAT grew marginally to Rs. 10.65 crore and 13.8% to Rs. 21.14 crore for H1FY 2016

The Company gross revenue grew 8% YoY to Rs 419.48 crore in Q2FY16. The revenue mix was Rs 147.54 crore from own manufacturing, Rs 170.73 crore from JVs, and Rs 101.21 crore from outsourcings. For H1FY 2016, gross revenue grew 13% YoY to Rs 827.48 crore, with revenue mix was Rs 294.81 crore from own manufacturing, Rs 337.66 crore from JVs, and Rs 195.01 crore from outsourcings.

Sales mix in Q2FY 2016 was Own manufacturing (35%), JV (41%) and Others (24%) while for H1FY 2016 sales mix was Own manufacturing (36%), JV (41%) and Others (23%)

As on September 30, 2015, the Company total debt stood at Rs 199.60 crore as against Rs 187.76 crore at end of March 2015. Working capital days increased to 43 days for H1FY 2016 from 39 days in FY 2015. Also, leverage ratio stood at 0.73 in H1FY 2016 as against 0.74 in FY 2015.

Operational Performance – The Company tiles business sales volumegrew 5.7% YoY to10.78million square meters (msm) in Q2FY 2016, while it rose 9.7% to 21.49 msm in H1FY 2016. For Q2FY 2016, sales volume mix was 4.6 msm from own manufacturing, 3.88 msm from JVs and 2.30 msm from others. For H1Fy 2016, sales volume mix was 9.13 msm from own manufacturing, 7.82 msm from JVs and 4.54 msm from others.

Capacity Expansion- 1) The Company plans to increase capacity to ~60 msm p.a. by end of Q1FY 2017 from current capacity of ~56 msm p.a.2) Somany Fine Vitrified Private, a subsidiary company expected to commence production of 4.3 msm p.a. of polished vitrified tiles in October 2015. 3)The Company brown field expansion at Kassar plant, Haryana, to produce 4 msm of glazed vitrified tiles is expected to be commissioned in Q1FY17.The Company remainsoptimistic about its future growth prospects in general and building and construction material industry in particular especially in the backdrop of various initiatives being taken by the incumbent government which would fructify in near future.The company remains confident over demand growth for H2FY 2016 on hopes that (i) Pay commission and One Rank One Pension (OROP) are likely to boost demand, (ii) CSR activities of Corporate India will pick up further steam than in the previous year helping overall industry growth, (iii) Exports continue to offer growth opportunities, and (iv) The recent cut in mortgage rates is likely to spur demand for Real Estate benefiting Buildings Material industry immensely.The Company guides tiles industry would benefit in coming quarter after initiation of anti-dumping duty on vitrified tiles by the Ministry of Commerce. Also, Government machinery is moving at a healthy clipping and will improve sentiments and demand prospects for the Buildings Material Industry.

The Company guidesGovernment plans for smart cities, dedicated freight corridor, Swachh Bharat Abhiyan, and housing for all will also bode well for Buildings Material Industry.80 Lakh Toilets built under the Swachh Bharat Abhiyan. Huge sums allocated by Corporate India under CSR. Framework laid for Smart Cities & Make in India programs; to lead to enormous investments and improve the quality of living in India. Relative Strength in Economy has allowed for cut in Interest rates leading to lower Home loan rates in nearly 4 years.

The company guides capex of Rs 100 crore for next 2-years. Of the total capex, the company guides a routine capex of Rs 30 crore and Rs 70 crore for brownfield expansion for FY16 and FY17.The Company trims topline growth of around 15-16% for FY 2016 from earlier guidance of 18-19%.The Company plans to take price hike between second half of December 2015 – January 2016.

Canfin homes ltd (30-10-2015)

Another HFC, which is even faster growing than can fin plans for an IPO

ie PNB housing finanace, it is growing really gud, with low NPA, better brand name etc.

Even we have their numbers discussed in past in this thread.

So, how will this impact can fin during listing time ?

dpnds they come with which valuations ?

can this lead to some rerating again ? wishful thinking

rgds

Elecon Engineering Limited (30-10-2015)

Call addr by Mr. Prayasvin Patel CMD & Mr. Rajat Jain CFO.Highlights-Capital Mkt

Co bagged orders worth Rs 112 crore in Sep’15 quarter in Gears division domestically as compared to Rs 107 crore of orders in Sep’14 quarter, and total order book position as on Sep’15 stood at Rs 258 crore as compared to Rs 275 crore in Sep’14.The company continues to remain cautious on order intake and was very selective. Given the order backlog, outlook remains robust for execution in coming quarters.Management continues to remain optimistic for orders and its execution in H2 FY’16. As per the management, the open cast mining would see more inflow of orders in next 9 months time frame. Upsurge will happen in order inflow in H2 FY’16.Defense, sugar and fertilizer sector are showing good traction and good orders are expected in H2 FY’16.Ebdita margins at consolidated level was around 13% in Sep’15 quarter largely due to improvement in international gear business and domestic gear business and increase in sales of spare parts together with tight costs control initiatives.

Elecon EPC or the MHE business sales stood at around Rs 101 crore in Sep’15 quarter with a loss of about Rs 12 crore and international gear business reported sales of Rs 74 crore for Sep’15 quarter with PAT of Rs 1 crore.Elecon EPC business has an order book of around Rs 1000 crore and international gear business has orders of around Rs 60 crore as on Sep’15.

Overseas entity Ebidta is expected to remain around 7% going forward for rest of FY’16.

Overall, management expects around 10% growth in consolidated net sales and Ebidta margins of around 12-13% for FY’16.Debt at consolidated level as on Sep’16 stood at around Rs 632 crore.The company is operating at 45% of capacity for gear business and there are not much capex planned for next 12 months.As per the management, so far not much benefit of lower steel prices was visible to the company as the company always booked the raw material on back to back basis.Around Rs 275 crore is the retention money lying with customers for more than 1 year now. Management expects Rs 60 crore of recovery before Mar’16.

Shirram City Union – Bet on MSME Financing (30-10-2015)

GS Sundararajan, MD &Subhasri Sriram, ED addr the call:Highlights by Capital Mkt

The company continues to exhibit steady growth across all segments in Q2FY2016, while well penetrating in to all geographies. The company expects second half of FY2016 to be better in terms of growth.Assets under Management (AUM) growth of the company accelerated to 17% at Rs 18165 crore at end September 2015 against a growth of 16% a quarter ago and 3% a year ago.The disbursements increased 9% to Rs 4527 crore in Q2FY2016 over Q2FY2015. Segment wise disbursement stood at Rs 1995 crore – small enterprise finance, Rs 800 crore – two wheelers, auto loans – Rs 200 crore, personal loans Rs 250 crore and Rs 1291 crore – gold in Q2FY2016.Off-balance sheet AUM of the company stood at Rs 500 crore, which is less 3% of AUM. The company has not conducted any securitization deals in H1FY2016, while expects to conduct securitization deals only in Q4FY2016.Overall Gross NPA ratio rose to 3.3% at end September 2015 from 3.17% at end June 2015. However, the Net NPA ratio was maintained at 0.65% with strong provision coverage ratio of 80.2% at end September 2015.Write-offs stood at Rs 71.23 crore, GNPA ratio including write-offs, stood at 3.69% at end September 2015.

Gross NPA increased by 50 crore in Q2FY2016 to Rs 582 crore at end September 2015, mainly contributed by small enterprise finance and gold loan book.Gold Loan Book GNPA stood at 2.55%, while non-gold GNPA was at 3.51% at end September 2015.

The company plans to shift NPA recognition norms from existing 180 days to 150 days over dues basis on 31 March 2016.As per the company, the GNPA would double to Rs 1000 crore from present level of Rs 582 crore, after shifting to 150 days over dues NPA recognition norms from present 150 days.Based on the current balance sheet position, the company estimates GNPA to be at Rs 1300 crore on 120 days and Rs 1700 crore on 90 days over dues basis.

With the huge customer base and small ticket size, the company and its collections teams are educating customers to adapt to the new NPA recognition norms.

Shriram Housing Finance:Shriram Housing Finance has crossed the AUM level of Rs 1000 crore at end September 2015. The AUM comprises mainly 90% of retail loans and 10% builder finance.The branch network of the company stood at 77 branches at end September 2015.

During the quarter, Shriram Housing Finance has tightened its NPA coverage and provisioning norms, which had a impact of Rs 1.2 crore on profitability. Accordingly, the provision coverage ratio was raised to 24% from 18%.