Greenply is the pioneer of MDF in India. Century is just starting off. The product is a commodity so both will do well. And I think both these companies will follow the ceramics industry model of partnering / buying out smaller players once GST rolls out and they (the smaller players) become nonviable.

Posts tagged Value Pickr

POKARNA LTD ( Stock opportunities ) (30-10-2015)

Results are little bit disappointing but not bad. Their overall EBITDA is about 33% this quarter in spite of Rs 3.2 crores loss from Apparel business. Yes Granite degrew, I have a feeling, going forward, their Granite segment will not grow much or will grow slower(I mean exports, but domestic granite business could still grow). Good thing Quartz grew, its their rising star, but I expected it to hit Rs 60 crores revenue this quarter considering their claim of Quartz plant running at 80%., either I overestimated, or they misrepresented the capacity utilization, will have to find out. I think Quartz EBITDA for this quarter are about 40%. Which is very impressive. Its encouraging to see how their Quartz segment margins are expanding. Compare the margins for last few quarters of quartz, you will notice. There is 2 months data on stoneupdate.com for this quarter, for July and August it shows 490k (july 175K and August 315K) square footage of quartz imports from India, for now , lets assume September did another 350k square feet (giving some monthly increment ) that makes it 840K square feet for the quarter from India. Give it a realization of $10 per square feet and and Rs60/USD exchange, that makes it little over Rs 50 crores in Rupee terms. That brings us to believe Pokarna is the only exporter of Quartz from India…would like to know if I am getting it wrong.

But most disappointing thing is their apparel business, Rs 1.5 cr revenue and Rs 3.2 crore loss?? Really??

I haven’t had a chance to look at the other Balance sheet details yet. Will spend some time over the weekend.

Any PSU bank worth investment? (30-10-2015)

In my opinion the larger PSU banks, the likes of SBI, BoB, PNB, Union Bank may be good options to keep a watch on. The smaller ones will have a tough time both from a financial capitalization and competitive landscape perspective with more private banks, NBFCs and payment banks.

P. I. Industries Ltd. – A Unique Business Model can make it a Great Play on Agri & CSM Space (29-10-2015)

@reacher, I would still respect @hitesh2710 views as it’s better to be a bit conservative on the estimates and work as if the EPS is around 22-23. Once FY16 completes, of course, the more EPS the better and market will re-rate then if the EPS is above the estimates.

I think the corporate tax rate is applicable from FY 17 onwards (April 2016?) though not sure on it.

I won’t factor in FY 17 yet personally, will do only in April 2016, that’s my personal view, though with secular growth companies market tend to price in much of the future ahead itself.

Bajaj Investment Holding Co (29-10-2015)

I am trying to understand holding companies, can someone suggest a good write up. I am looking at understanding how to evaluate their fair value and advantages.

I have Bajaj holding for 2 years now and it has given steady return.

Any help in this regard will be appreciated.

Thanks

Sukhbinder

What am I missing in Insecticides India? (29-10-2015)

there was a QIP done last quarter, hence the promoter holding has come down and DII/FII holding has went up.

P. I. Industries Ltd. – A Unique Business Model can make it a Great Play on Agri & CSM Space (29-10-2015)

richdreamz

my workings as per the concall : 15% blended sales jump – total sales 2230 crs – 995 = 1235 Crs . He said (if i heard him right ) jump of minimum 100-150 bsp in margins but to be conservative i have taken net margins @ 15% (only 50 bsp taken) – 15% of 1235 crs=185.25 Crs – Eps for full year = 13.6+10.6=24.2

This is w/o considering 5% reduction in corporate tax rate . So your earlier no of 25 eps is v much logical i think .Also perhaps its about time may be by Nov/Dec when eps for the next fy might get discussed and factored ?

Chemicals and Speciality Chem space in India (29-10-2015)

Executive Summary of report attached here

Will the investor community continue to ignore the Indian specialty chemicals sector, with a

market size of about US$ 25bn? This industry has already delivered healthy 13% CAGR (next

only to China and Korea) over the last decade. India has emerged as the fastest-growing

specialty chemicals market fuelled by sturdy domestic demand with strong economic growth,

a large population, and rise in per-capita income. A simultaneous reduction in input costs, due

to the sharp correction in crude prices, enhanced the earning efficiency of the industry, which

relies on imported inputs. Moreover, softening of Chinese chemical exports, with environmental

issues leading to a shut down and relocation of 1000+ chemical plants, adds zing to India’s

specialty chemicals exports potential for the next couple of years. Additionally, the Indian

government’s ‘Make-in-India’ initiatives in addressing the old hurdles of the industry, with

enhanced focus on R&D and the rapid flow of FDI into the sector indicates value growth in the

domestic specialty-chemicals industry. This issue takes an in-depth look into the rising tide that

will float all speciality-chemicals boats.

By Phillip Capital

chemicals.pdf (2.1 MB)

POKARNA LTD ( Stock opportunities ) (29-10-2015)

The stock hardly reacted to stellar set of nos. Seems everyone is buying or selling with one eye on index. On company’s part they have fallen short somewhat in deleveraging the balance. This is largely due to earnings have gone into building working capital or reducing some other liabilities. On longer term folks need to worry about rising rates and impact on housing.

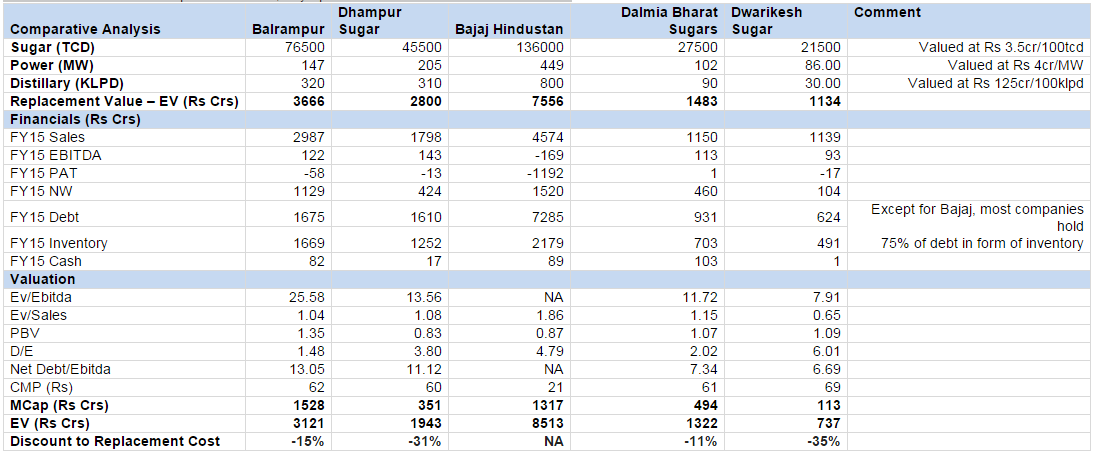

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (29-10-2015)

I have Reworked SOTP of key sugar companies post recent rally – Balrampur and Dalmia Sugar discount has come down significantly but Dwarikesh and Dhampur still provides some headroom there. Just to highlight, Replacement cost might also go up as market will start paying premium to earlier price given the attractiveness of the sector. I have not revised replacement cost, any upside revision will increase the discount.

But few days back i was checking 10 year seasonality chart of global sugar prices which suggests that any 3-4 month of rally in sugar price is followed by prolonged correction…will try to update that chart…so i feel the recent rally in sugar price will wane off in 1-2 months time…once that correction starts reflecting in sugar prices then we will see some correction in these stocks which ran up too fast too soon…i might be wrong but such a rally in short span is irrational….