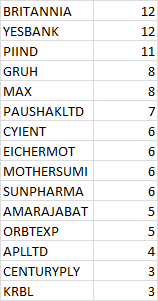

Done with the modifications with my portfolio. Finally reduced to 15 stocks from 50+. Here is the list. Comments are most welcome.

Posts tagged Value Pickr

My Portfolio – Dhina (21-10-2015)

Canfin homes ltd (21-10-2015)

Hiteshbhai good question . please elaborate more on ways that can be achieved( enhanced return ratios ) .

My opinion is that they have very few levers(they are already using CP funding ) and it will be very difficult to change the culture of company. they can (should ?) not go into non salaried class where yield is higher but you need better risk management & customer creditworthiness check are difficult.

so now stock price growth may be some re-rating (if any left) + annual business growth (which is not bad )

your view will be awaited ..

V-Mart Retail Ltd (21-10-2015)

Disruption due to barrage of online retailers would be a huge headwind for vmart and other similar players.

Even if actual impact may not be there, there will always be that perceived threat in the mind of most investors and I feel that should limit any kind of PE expansion.

disc: not invested.

SKS Microfinance (21-10-2015)

but why is price crashing post results?Satin creditcare the 2nd listed MFI is on 20% UC for last 2 days on the other hand

Canfin homes ltd (21-10-2015)

Till date since many quarters canfin has beaten all other HFC gruh and repco included in terms of growth and asset quality.

Can it get another bout of re rating to get closer to gruh is a question that needs to be answered. For that it will need some bump up in return ratios first.

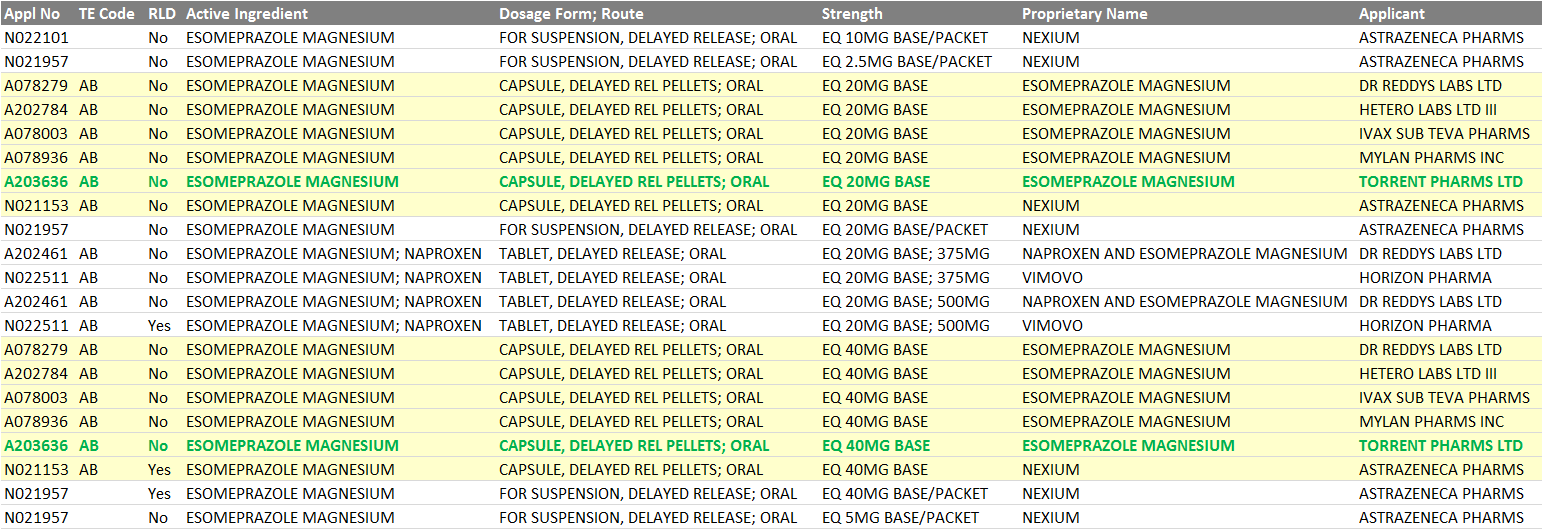

Torrent Pharma Ltd (21-10-2015)

Before the entry of generics, the size of nexium was 6 billion USD. Now torrent gets approval and it is the fifth company to get approval for the molecule according to their NSE announcement.

The questions that need to be answered are:

What kind of price erosion has happened/will happen?

What % of market share will torrent be able to garner since it is fifth co to launch the drug?

Overall looking at the size of the molecule and limited competition, it augurs well for torrent if they can capitalise on this approval.

Chemicals and Speciality Chem space in India (21-10-2015)

oriental carbon and chemicals – which is one of the three players in the world making insoluble sulphur used in tyres

Syngene International IPO – Views invited (21-10-2015)

Mahesh whats the expected EPS ,ROCE & CAGR for Syngene for next 2-3 years? will opp size also keep on increasing?

Torrent Pharma Ltd (21-10-2015)

Thanks @rajpanda – much awaited good news. Limited competition as of this date. Hope this late entrant can cover decent ground.

STL Global Ltd. (532730) (21-10-2015)

Hi Jigar,

If you can fix a meeting with the mgt., I ‘ll be happy to come from Mumbai for the same, but I suspect the mgt. may not oblige. Mgt. credibility is amongst the negatives in my view.

How much of the debt amount is finally settled for is not known. The earlier CDR failed to materialize as the revenues from the IT project did not come through. The mgt. & the developers may well be hand in glove. I won’t be surprised if the mgt. goes for a share buy back when they feel that they are in a position to settle with the banks. I feel confident that there is enough juice in the project because the mgt. willingly paid 50 crores to the banks towards debt repayment a couple of years ago.

The key here is to follow the development of the real estate project. The gains will come from there.