Crane is sure a household name in AP & TG.

Durga Ghee, Heard of it but not sure, at least I have not seen it occupuying a shelf space of dairy at any super stores.

When I was small I don’t know what betel is, we just know crane pouch packs are used along with betel leaves.

Promoters are looking to be in a hurry to add more verticals non relative businesses which is not good.

Are they talking of unlocking the real estate value they sit on ?

Anyhow it is a common misunderstanding that Guntur is gonna be capital. to be precise the area selected for capital falls in Guntur and is near to Vijayawada city than Guntur.

Do not generalise the place Guntur, it is too big a geographical area. Chirala, Bapatla, Tenali, Sattenapalli, Macharla, Dachepalli, Narasaraopet, Vinukonda, Mangalagiri all are in Guntur and real estate value differs by leaps. One end a acer may not cost more than 2 lac and one end u might not get one fot 50 lac, I am talking of pure agri lands.

Anyhow are the management looking at unlocking land bank value ?

Posts tagged Value Pickr

Virat Crane Industries Limited (VCIL) – sure shot multibagger (14-10-2015)

My Portfolio – Dhina (14-10-2015)

I am trying to do a basic check on all the stocks I own. Please correct me if I have missed any basic parameters.

Company: Cyient

Pros:

Zero Debt

5 Yr sales growth: 23.48%

Profit growth: 15.56%

ROE: 17.83%

Current price < Intrinsic value

Net cash flow: 192.52

Consistent dividends. Last year: 25.43%

Cons:

Low promoter holding.

Being a Mid cap, ROE is comparatively less(10 year ROE for TCS: 44%.If compared, TCS has given far better returns. I am not able to find any advantage in Cyinet over TCS apart from better sales. Can someone please help to find if there are any?)

Decision: HOLD

Virat Crane Industries Limited (VCIL) – sure shot multibagger (14-10-2015)

(post withdrawn by author, will be automatically deleted in 24 hours unless flagged)

Cafe Coffee Day – Will you Date? (14-10-2015)

Sorry I am a bit lost here with your calculations whilst evaluating the company.

You say

1) market cap of Sical is 900 cr so 50% is 450 cr. 1/6 of 450 is indeed 75 cr (as you suggest) so the value of the holding should be 5/6 (discount = less by 1/6) which is 375 cr.

2) Similarly for the Mindtree valuation. 16.6% of 10,500 cr is 1743 cr of which 5/6 is 1452.

Both together contribute 375 + 1452 = 1828 approx. Add cash of 197 = 2025 so you get the other parts of the company for 6756 – 1828 = 4732 cr. Then add 2100 cr for debt EV = 6832cr (as opposed to your calculation of 7900 cr).

The difference in calculations is that you discount the value of the holdings of Sical and Mindtree to 1/6 whereas I discount by 1/6.

Maybe I am doing something wrong. Please advise.

Nevertheless, the story does not look good to me with the political angle and capital allocation.

BTW, apart from Rakesh Jhunjhunwala I believe his mentor Radha Kishen Damani is also an investor through his Derive investments. But why go by them. RJ also invested in A2Z maintenance and Bilcare.

Regards

Kumar

Shaily Engineering Plastic (14-10-2015)

The ZAHORANSKY Customer Magazine

Shaily Plastics Engineering from India is Capturing the Brush Market with support from ZAHORANSKY

“In our cover story, our Indian customer Shaily Engineering Plastics

describes how all-round support from ZAHORANSKY – from product development

through to start of production and the implementation of a new technology

– works in practice. This story and other current highlights about the company

are waiting for you in the new issue of CONTACT”.

http://zahoransky.com/files/PDF/Contact_Digital_01-2015_EN.pdf

Intellect Design Arena PICK for 2015 (14-10-2015)

Transaction banking is ofcourse going to be more critical because in developed countries the core banking segment is pretty stagnant because of stable population base.

All of these transaction banking , core banking , risk management are individual components with a plug and play feature. This is the basis of what in IT is called as component based architecture.

No bank will go for the entire suite as the risks would be too high. So you plug in areas with maximum demand. E.g. IDFC has chosen IDA for its transaction banking component only while its core banking suite will be something else.

Another info Rakesh Jhunjhunwala has further upped his stake in IDA as per the latest shareholding pattern. That is the reason for the current upswing.

KAPIL Portfolio (14-10-2015)

Bought some LLoyd Electric today at 218 roughly 2% of Portfolio.

Their debt has been on an increasing trend but it seems that because they are currently in growth and expansion mode.

Also value of their Other Assets have been increasing.

Can any Senior Guide what all comes under Other Assets.

Is it possible that they are using this debt to buy offices/outlets or setting up franchises for pushing their

Consumer goods.

Was Just Comparing its Market Cap and Profit figures with that of Blue Star and found that it reports more operating profit than Blue STAR.

However could not understand that it is a consumer Goods company reporting regular profits how come

its operating Cashflow is negative. (If any senior can provide insight into this).

Have Checked online Sites as Diwali Time is approaching and Saw their ACs and Washing Machines on Amazon and Flipkart

Will keep track of their numbers if in one or two quaters indication of debt reduction or improving cashflows are seen than will add more else will get Out

Seniors and Fellow Mwmbers Views are invited.

Regards,

Kapil

Arvind infrastructure: Godrej Properties in the making? (14-10-2015)

Few doubts

The company doesn’t seem to be having any land holding. As per BS Mar 2015, Tangible assets of about 2 cr and i can’t find any freehold land.

As per their presentation, some of the projects , it is mentioned DA-Arvind land. I assume the land belongs to either Arvind ltd or another group company. But i don’t understand then why the percentage ownership is 100%.

The long term and short term advances are very high.

Understand that the company intends to develop 14 m sq ft of space. And it is expected that the cost of construction will come from sales proceeds ( advance from customers ) but as of 31 mar 15 advance from customers is mentioned as only 2.75 cr ( 4 cr in mar 2014) which seems pretty low.

In order to execute the projects the company needs to sell heavily in advance and same should reflect in Balance sheet.

Also need to monitor inventories. Mar 15 it stands at abt 76 cr.

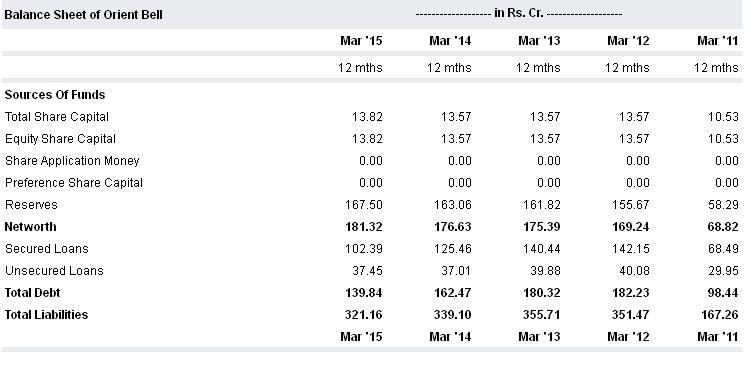

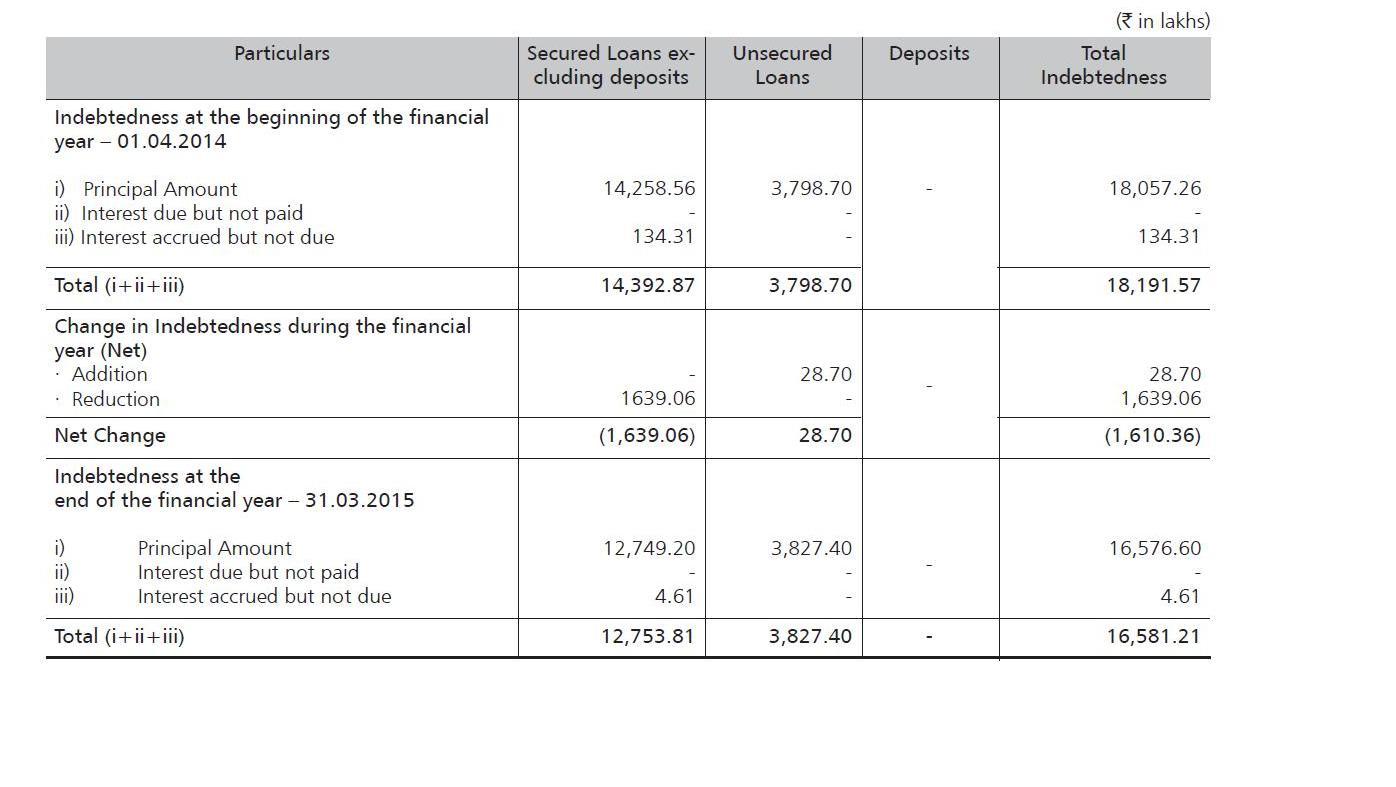

Orient Bell Limited (14-10-2015)

akshay my point is that 50 cr. of operating profit will not go in to debt repayment. u have interest of 20 cr. that u have to pay . and income tax on PBT and u have maintenance capex . i am being very liberal here because i am not even talking about depreciation here.

Moneycontrol figures of debt is misleading as it does not take into account current maturity of debt . here actual debt is 165 cr. not 139 cr.

actual debt figure from AR 2015

again sales growth is not 20% even after acquisition sales rose from 546 cr (fy12 ) to 693 cr.(fy15) it is at best a 10% growth and anyone will agree that last 3-5 years environment was much better that current one.

Finally it is difference of opinions that make market . i am holding shares and want them to move up  but i like to have reality check of business which i own so i can sell them at right time.

but i like to have reality check of business which i own so i can sell them at right time.