Just a query, how long do you think it would take PI to become a 5 bagger from current levels? I think PE is already at its peak so only growth in EPS would take the price higher.

Posts tagged Value Pickr

Vidhi Dyestuff Management Meet (06-10-2015)

The importance of colors to attract the buyers is very well known to the industries. As such, the market of color pigments is growing at a very fast pace. A wide range of pigments are used in textile industry and they are increasingly substituting dyes. Other than textiles, pigments are used extensively in the sectors like cosmetics, paper, building material, ceramics, and glass. (Even pharma)

Vidhi Dyestuff Management Meet (06-10-2015)

What constitutes of pigment market?

Disc: Have a tracking position.

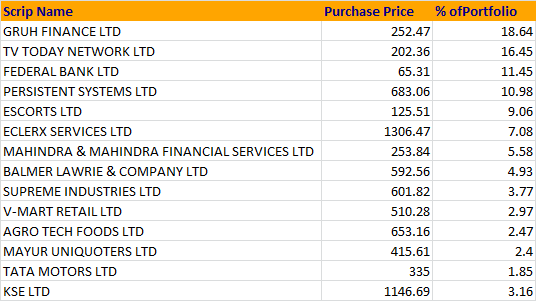

Value and Growth Portfolio (06-10-2015)

Have exited out of IPCA, Polymedicure and VA Tech Wabag with some partial gains

Any suggestions on portfolio composition or allocation would be helpful.

Value and Growth Portfolio (06-10-2015)

Scrip Name Purchase Price % ofPortfolio

GRUH FINANCE LTD 252.47 18.64

TV TODAY NETWORK LTD 202.36 16.45

FEDERAL BANK LTD 65.31 11.45

PERSISTENT SYSTEMS LTD 683.06 10.98

ESCORTS LTD 125.51 9.06

ECLERX SERVICES LTD 1306.47 7.08

MAHINDRA & MAHINDRA FINANCIAL SERVICES LTD 253.84 5.58

BALMER LAWRIE & COMPANY LTD 592.56 4.93

SUPREME INDUSTRIES LTD 601.82 3.77

V-MART RETAIL LTD 510.28 2.97

AGRO TECH FOODS LTD 653.16 2.47

MAYUR UNIQUOTERS LTD 415.61 2.4

TATA MOTORS LTD 335 1.85

KSE LTD 1146.69 3.16

Torrent Pharma Ltd (06-10-2015)

Torrent gets tentative approval from USFDA for g benicar which is an anti hypertensive olmesartan Medoxomil

Here its pertinent to note that the final approval is the important milestone.

Vidhi Dyestuff Management Meet (06-10-2015)

Hi Vaibhav

- Increase in margins was due to capacity expansion and higher utilization and several efficiency revamps.

- With the current capacity of 4200 MTPA they will do around 250 Cr of sales by FY17 and the incremental expansion will double the capacity and thus double the topline by FY20.

My richdreamz portfolio – visit my portfolio to learn together! (06-10-2015)

hmm, actually not very sure, but the answer to your question may not be company specific but investment process specific. My approach is,

it really does not matter, we will never have clarity on all issues in all businesses and by the time the clarity emerges, the stock price would have gone up. Companies where there is clarity, like Page few years back, are rare to find and when we get such opportunities many will be found sucking the thumb.

In PI case, there are two options, govt. will interfere and govt. will not. By the time we are sure that govt. will interfere, price would have gone up 5 times and then since govt. is interfering the price would fall by 40% but even then you would have made 3 times the original. Now, if the govt. does not interfere, you are left with 5 bagger and still to go…

The above is how I’m thinking…

Vidhi Dyestuff Management Meet (06-10-2015)

Hey

Thanks buddy

Apart from discontinuing trading business, capturing market share of the american giant and capacity expansion, other triggers are as follows:

- Gradual foray into Natural food colour market (Huge opportunity there)

- Pigments market also can be captured which is another opportunity altogether.

Vidhi Dyestuff Management Meet (06-10-2015)

Hi @desaidhwanil and @abhijitchokshi

Thank you for the mgmt meet update. i hav just couple of queries:

1. what has led to increase in ebitda margins of manufacturing in last 2 years. ebitdam in mfg has increased frm 5% in fy13 to more than 20% in fy15 . ny reasons for the same ?

2. also mfg sales were arnd 115 cr in fy15 nd they r going to discontinue trading. doesnt the company’s tgt of 500 cr in 2020 look aggressive ?