Valuable post. Gr8 work.

What are the growth triggers available in future to maintain a 20+ CAGR apart from the one mentioned by you – Acquiring market share from sensient .

Valuable post. Gr8 work.

What are the growth triggers available in future to maintain a 20+ CAGR apart from the one mentioned by you – Acquiring market share from sensient .

Has someone met management recently? can someone update on the notes from AGM?

I am still little skeptical about 8K Miles, because other larger companies must be also seen the opportunity in the cloud computing business.

So other large IT companies like HCL,WIPRO,TCS and INFOSYS must be also in the cloud computing business, also persistent computers.

Then what is so unique about this company.

Please need some help to understand.

Regards

I think the golden period for the pharma business has just now started with the most of the block buster drugs going off patent in FY16 to FY20. So there huge opportunity for all the companies to get a pie of it.

More MNC companies need minimum 4 -5 blockbuster drugs to maintain there current growth rates which is very difficult. So we will see more companies will consolidate for more takeovers in the future because they cannot match the skills and cost of Indian pharma business.

So I think we can still get 20 – 25% growth in the pharma business for atleast another minimum 5 years.

It’s a win win situation for the foreign countries where they free healthcare services, they want cheaper drugs for healthcare.

@varadharajanr who is this competitor? what’s the name of this company? thx

As long as underlying business/management is good then worrying about bubble is mostly futile. For fresh buys definitely the valuations are stretched for most good pharma companies. but time to time there are good opportunities to buy them like in recent fall there were some good companies at attractive valuations.

How far it can go? – Honestly no one knows that answer.

Yes, Abhijit. You should put appropriate and meaningful disclosure to comply with forum guidelines.

Hi Dhwanil

Glad it was useful!

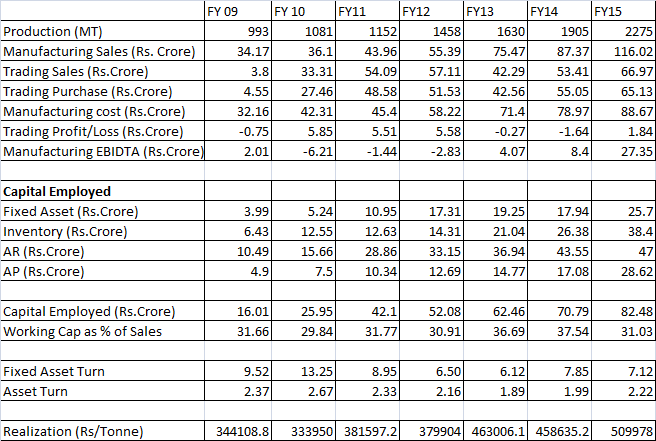

Another interesting observation from the AR is that despite the major break down due to fire of a critical equipment (which affected 30% of the production), they were able to grow at a steady pace.

I feel discontinuing the trading biz is a very wise move and must result in superior ROCEs.

Also as I’m new here, Is it compulsory to put Discl. at the end?

Hi Abhijit,

Thanks for the management meet updates. It is very useful. Especially, the answer to Sensient buying out VDSL was very interesting!!

If the management’s vision plays out, it looks like a very interesting bet. However, there is one big “If”. We, as an investor, must assess the odds of management’s vision turning into reality. I did some number crunching and few inferences base on the same

After looking at competitors like ROHA and Sensient, I too come to same conclusion that it is a industry dominated by few large players and business is growing for companies like Roha and Vidhi as companies like Sensient are forced to look at natural colors due to their existing clients demanding the same. At the same time, I also got an impression that there exist a slow but sure shift from synthetic color to natural colors (even though, as management rightly pointed out, there is no evidence of synthetic color being harmful). Thus, it will be prudent to start developing products for natural colors market.

On whole, it remains interesting idea worth tracking to me

Disclosure: Hold small position @ Average price of 48.

Hi Hitesh,

With pharma doing so well in recent years, do you foresee a bubble forming? or are we already in a bubble? All pharma cos valuations are stretched. How far can it go?