Yes FDC seems to be approaching fair valuation now.

Posts tagged Value Pickr

MPS Ltd (06-10-2015)

True….if the acquisitions doesn’t materialise in coming few months, the acquisitions done after that will need to be right and perfectly right otherwise a very bad example will be set by the management for the investor community which will be very detrimental for company’s long term fund raising prospects…..if management is comfortable of its company’s valuations, then no rationale management with zero debt will dilute equity without concrete proposals and no concrete proposals can take more than six months to seal……In today’s dynamic world, time lost is opportunity lost and so a slight right decision taken late could be as good as wrong when you have already slipped to 10th position from 5th position….I am sure Mr. Arora is aware of this fact and so if he is taking more time then we might see a very good game changer acquisition….let’s keep our fingers crossed.

Rgds.

Satin Creditcare Network Ltd – Reaching out! (06-10-2015)

The company has grown the loan book very, very aggressively from 50,000 Rs to 2150 Crore Rs, over past 25 years, roughly CAGR of 60%.

Importantly, past the 2011 M.F.I. hump, company has returned to same growth!

In North India the competition is relatively benign in Mirco Finance sector.

The key risks I.M.H.O are political. This may be a good trading bet.

Tasty Bites: A proxy play to India’s QSR industry (06-10-2015)

a) 5 years of 25% CAGR.

b) Last year US (RTE) Business grew by +25%, domestic business grew by only 8% (FSSAI issue).

c) Aggressive growth in both segments this year. Do not give explicit growth targets,

d) Market reach in US doubled from 8000 to 16000 (out of 36000) outlets in one year.

e) FSSAI issues impacted India launches (Rockr was rejected). New launches this year Rockr Burger (KFC), Chilli Paneer Pockets (McDonalds). FSSAI no longer required to approve products as per supreme court order.

f) Started operation in UK this year. UK RTE market largest in world for Indian foods.

g) RTE market share for Indian food bigger than all other players (Haldiram, MTR, ITC etc.) combined.

h) Limited impact of food price fluctuation.

i) Working with local chains like FAASO’s.

j) Working on complete organic foods and will launch them in two years. Sourcing everything organic is very difficult. Working with farmers to grow organic rice etc.

k) Entered into a tie-up with Wendy’s UAE (15 stores) for QSR supplies.

l) Capacity utilization of various divisions: RTE (80%), Patties (60%), Sauces (50%).

m) New capacity to be added this year in RTE business. Capex plan 5.5 cr for one additional line (existing two lines).

Kagome Impact:

a) Largest manufacturer of Tomato Ketchup worldwide with far superior quality.Looking to develop tomatoes with Kagome help.

b) Will be using Kagome’s research in agricultural technologies.

c) Use each other’s distribution network.

d) Kagome’s name gives an easy entry in quality QSR, example cited was Wendy’s UAE.

Conclusion: Came out highly impressed with management.Entry into UK market +ve for RTE. Newer products with McDonalds, KFC, FAASOS shows traction in QSR. I liked their response on dividends where they said as long as we are able to deploy capital generating significantly higher returns than cost of capital the dividend payouts will be limited. Post that period they will increase significantly.

Discl: Holding from lower levels.

Satin Creditcare Network Ltd – Reaching out! (06-10-2015)

An Informative report on MFI sector as well as detailed research report on Satin CreditCare Network.

http://research.religarecm.com/INDIA/India%20Microfinance%20-%20Sector%20Report%2019Aug15.pdf

Skipper Ltd., distributing Power and Water, Is it a moat in making? (06-10-2015)

Latest Board Meeting held on 5th October in which the Board has provided following two in-principle approvals:

1) ESOPs;

2) To purchase PVC manufacturing Plant and Machineries from Skipper Polypipes Private Limited which seems to be a group Company.

While 1st item gives positive outlook of the Company, can’t comment much on 2nd item it could be have some tax angle to it. Please find below link of the said in-principle approvals.

http://www.moneycontrol.com/stocks/reports/skipper-limited-1924681.html

Hitesh portfolio (06-10-2015)

Hi Hitesh.. If my memory serve, you had FDC in your portfolio… fdc is already a 4 bagger for me.. not sure if market is stretching its valuation.. What is your view on fdc now

GRUH Finance – mini HDFC (06-10-2015)

Hi Hitesh,

I am afraid this is like putting the cart in front of the horse.

The question to ask is whether Gruh can raise fresh equity at CMP. The hypothetical situation of whether Gruh will be overvalued / undervalued after raising fresh equity, arises only after Gruh is able to successfully raise fresh equity at CMP.

It is the same question facing Flipkart types today. Question is whether they can go for an IPO and raise fresh equity at $15 billion – $20 billion valuation today… The hypothetical question of whether they will be overvalued / undervalued after raising equity in the IPO is a moot question.

Anyways, can you show a calculation of how the valuation would look like, if Gruh is able to raise fresh 30% equity at CMP…. Requesting this as I think the calculation by @richdreamz to illustrate this was probably not what you meant (that calculation is completely misleading, I am afraid)… If I think I understood you – you are trying to say that P/BV will be between 8 – 9 on a 1 year forward basis…. Why is that leading to a conclusion that Gruh is undervalued / fairly valued….

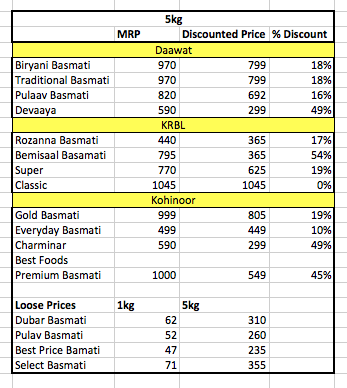

KRBL- The King of Basmati rice (06-10-2015)

Did some more scuttlebutt on 5kg pricing a while ago.

Below is the table:

1kg and 5kg India Gate Classic brand was either absent or had very poor shelf space in Hypercity, Spar and More stores. If somebody can check two biggies – Big Bazaar and D-Mart that would complete the picture.

I don’t see domestic sales of KRBL picking up and Export remains the saviour for coming quarters. Even there, I think similar story will play out. These are testing times for India Gate as a brand.

Further drop in paddy prices means that KRBL has to manage high price paddy procured 18-24 months ago.

I think when paddy price cycle turns – then KRBL might be an attractive play for 1-2 years after that.

Disc: Sold partially yesterday. Looking to sell half holdings on rallies.

Want to learn about commodity market (06-10-2015)

I think you have come to a wrong place. This is an equity forum and you may not get info about the commodity market from here.